Mobvista (SEHK:1860) Valuation Check As 2025 Earnings Guidance Flags Strong Profit Rebound

Mobvista (SEHK:1860) has drawn fresh attention after issuing 2025 earnings guidance that points to higher revenue and a sharp profit increase, largely tied to its Mintegral advertising platform and improved operating efficiency.

See our latest analysis for Mobvista.

The guidance has arrived at a time when Mobvista’s recent momentum has been mixed, with a 2.33% 1 day share price return and 6.89% 7 day share price return contrasting with weaker 90 day and year to date share price returns. At the same time, the 1 year total shareholder return of 156.97% and 3 year total shareholder return of about 3.1x suggest that longer term investors have still seen strong gains.

If this earnings update has you thinking more broadly about digital advertising and AI, it could be a good moment to look at 59 profitable AI stocks that aren't just burning cash as another way to spot potential opportunities backed by earnings rather than hype.

With 2025 guidance pointing to higher revenue and much stronger profit, yet recent 90-day and year-to-date returns weaker after a big one-year run, is Mobvista still offering value, or is the market already pricing in future growth?

Preferred Price-to-Sales of 1.3x: Is It Justified?

Mobvista is currently trading on a P/S of 1.3x, which sits slightly below its peer group average of 1.4x and above the Hong Kong Media industry average of 1.1x.

The P/S ratio compares Mobvista’s HK$12.72 share price to its HK$1,922.70m revenue and is often used for companies that are not yet profitable, as is the case here.

On one hand, the P/S of 1.3x lines up closely with peers, suggesting the market is treating Mobvista similarly to comparable companies. On the other hand, it is materially below an estimated fair P/S of 2.3x from our model, which is a level the market could move toward if revenue growth and the path to profitability unfold in line with expectations.

Compared with the broader Hong Kong Media industry average P/S of 1.1x, Mobvista trades at a premium, which points to investors already assigning a higher value to its revenue than the sector overall, while still sitting below that estimated fair P/S level implied by the SWS model.

Explore the SWS fair ratio for Mobvista

Result: Price-to-Sales of 1.3x (UNDERVALUED)

However, there are clear risks, including Mobvista’s recent negative 90 day and year to date returns, as well as its current net loss of $25.672m despite solid revenue.

Find out about the key risks to this Mobvista narrative.

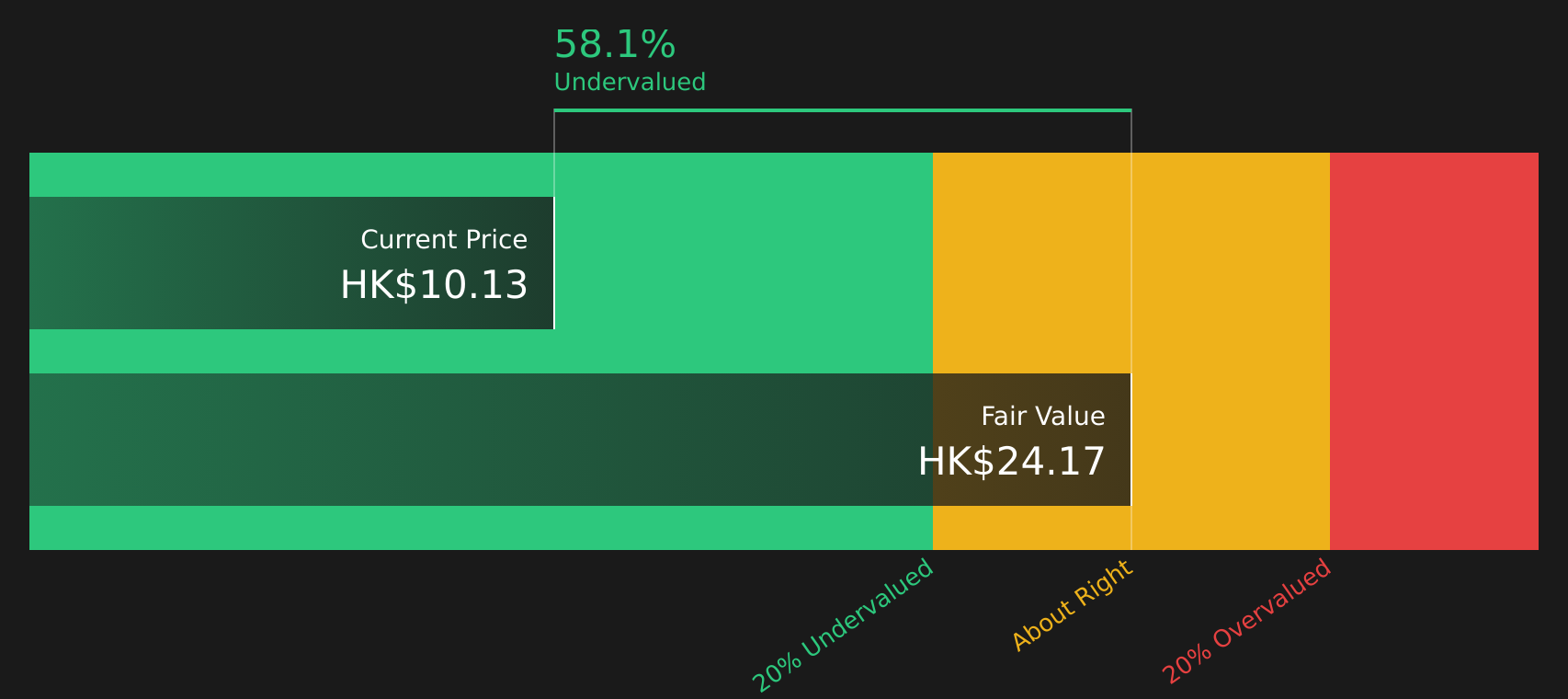

Another View: What Does The SWS DCF Model Say?

While the P/S of 1.3x suggests Mobvista is cheap relative to its fair ratio of 2.3x, our DCF model indicates an even stronger case. On this view, the current HK$12.72 price sits about 57.8% below an estimated fair value of HK$30.14.

That gap looks large on paper, but it also raises a practical question for you as an investor: how comfortable are you with relying on long term cash flow assumptions for a business that is still loss making today?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Mobvista for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 224 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the signals here feel mixed, this is exactly the moment to look at the underlying data yourself and move quickly to form your own view. A good place to start is 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Mobvista has sharpened your thinking, do not stop here. Widen your watchlist with a few focused stock ideas built from clear fundamentals and risk checks.

- Target value first and hunt for 224 high quality undervalued stocks where solid fundamentals meet prices that may not fully reflect the underlying business.

- Prioritise resilience and review 299 resilient stocks with low risk scores that score well on financial health and business risk, so sudden shocks are less likely to catch you off guard.

- Get ahead of the crowd by scanning our screener containing 576 high quality undiscovered gems and spot quality companies that many investors may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English