Did Plexus' (PLXS) Earnings Beat and Guidance Raise Just Shift Its Sector Mix Narrative?

- Plexus recently reported a strong quarter with revenues of US$1.07 billion, up 9.6% year on year and in line with analyst expectations, while also exceeding forecasts for earnings per share and issuing higher-than-expected revenue guidance for the next quarter.

- Management highlighted especially strong momentum in Healthcare/Life Sciences and Aerospace/Defense, underscoring how its investments in talent, technology, and advanced capabilities are reinforcing these higher-complexity, higher-value sectors within its overall business mix.

- We’ll now examine how Plexus’s earnings beat and growth in Healthcare/Life Sciences and Aerospace/Defense affect the company’s investment narrative and outlook.

The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Plexus Investment Narrative Recap

To own Plexus, you need to believe in its ability to win and scale complex, higher-value programs in Healthcare/Life Sciences and Aerospace/Defense, while managing cyclical swings in other end markets. The latest quarter’s earnings beat and higher revenue guidance support that thesis and appear to strengthen the near term catalyst around continued program ramps, but they do little to reduce the key risk from customer concentration and program timing that can still unsettle results.

The most relevant recent announcement here is Plexus’s Q2 fiscal 2026 revenue guidance of US$1.11 billion to US$1.15 billion, paired with GAAP diluted EPS of US$1.53 to US$1.68. This guidance sits alongside management’s commentary on strong Healthcare/Life Sciences and Aerospace/Defense demand, tying the near term outlook directly to the same sectors that are driving investor optimism, while also highlighting how dependent Plexus remains on sustained orders and smooth ramps in these complex programs.

Yet investors should also be aware that customer concentration and large program ramps can quickly become a headwind if...

Read the full narrative on Plexus (it's free!)

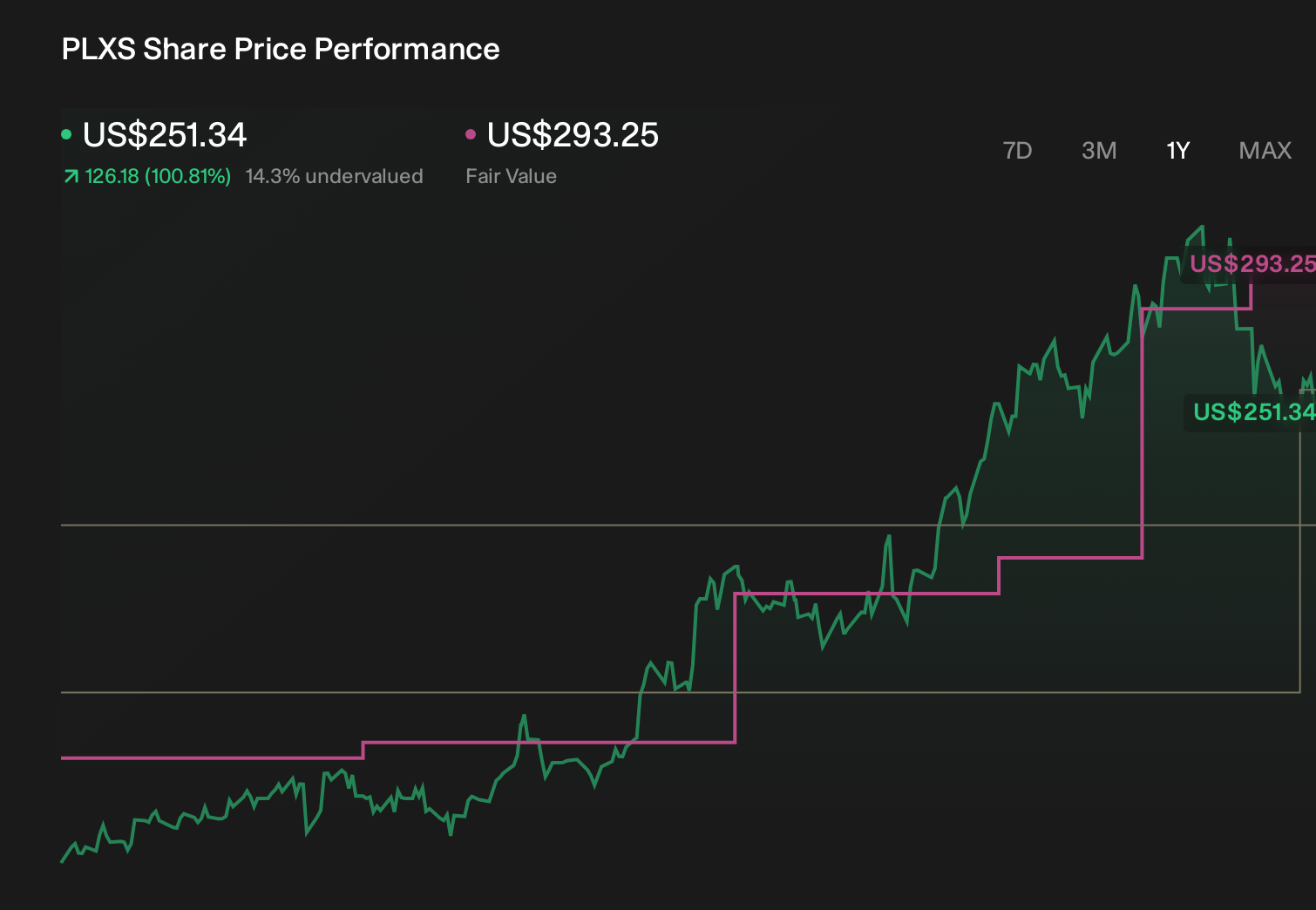

Plexus' narrative projects $4.8 billion revenue and $202.1 million earnings by 2028. This requires 6.1% yearly revenue growth and about a $39 million earnings increase from $162.7 million today.

Uncover how Plexus' forecasts yield a $200.80 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Before this earnings beat, the most optimistic analysts were already modeling revenue of about US$5.2 billion and earnings of roughly US$257.2 million by 2029, which is a far more upbeat view than the baseline narrative and leans heavily on ongoing Aerospace and Defense strength and the same long cycle program risks you have just read about.

Explore 3 other fair value estimates on Plexus - why the stock might be worth 40% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Plexus research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Plexus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Plexus' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English