Is Sunrun’s (RUN) Battery Storage Dominance Offsetting Concerns About Softer Near-Term Earnings?

- In recent days, Sunrun reported softer expectations for near-term earnings as analysts cut forecasts and voiced concern about slower solar origination and capacity deployment, even while revenue is still expected to grow.

- At the same time, Sunrun remains a major force in U.S. residential battery storage, controlling roughly half of 2025 installations and about 44% of national residential storage capacity, highlighting a tension between operational leadership and financial strain.

- Now we’ll examine how these reduced earnings expectations, alongside Sunrun’s battery storage leadership, may influence the company’s existing investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Sunrun Investment Narrative Recap

To own Sunrun, you need to believe that its leadership in residential solar plus storage and grid services can translate into durable, profitable growth despite policy, financing, and demand uncertainty. The latest cuts to earnings estimates highlight how fragile near term sentiment is, but they do not fundamentally alter the key near term catalyst: converting Sunrun’s dominant battery footprint into recurring, higher margin grid services revenue. The biggest immediate risk remains execution under financial strain, especially given leverage and financing needs.

The most relevant recent update here is analysts’ 44.67% cut to near term EPS forecasts while still expecting revenue to rise. That shift aligns with concerns about softer solar origination and capacity deployment, even as Sunrun’s 44% share of U.S. residential storage capacity underscores its operating scale. For investors focused on storage driven upside, this tension between earnings pressure and asset strength is central to how the catalyst, and the risk around it, might evolve.

But against this operational leadership, investors should be aware of how Sunrun’s high debt load and distress flagged by its Altman Z-Score could...

Read the full narrative on Sunrun (it's free!)

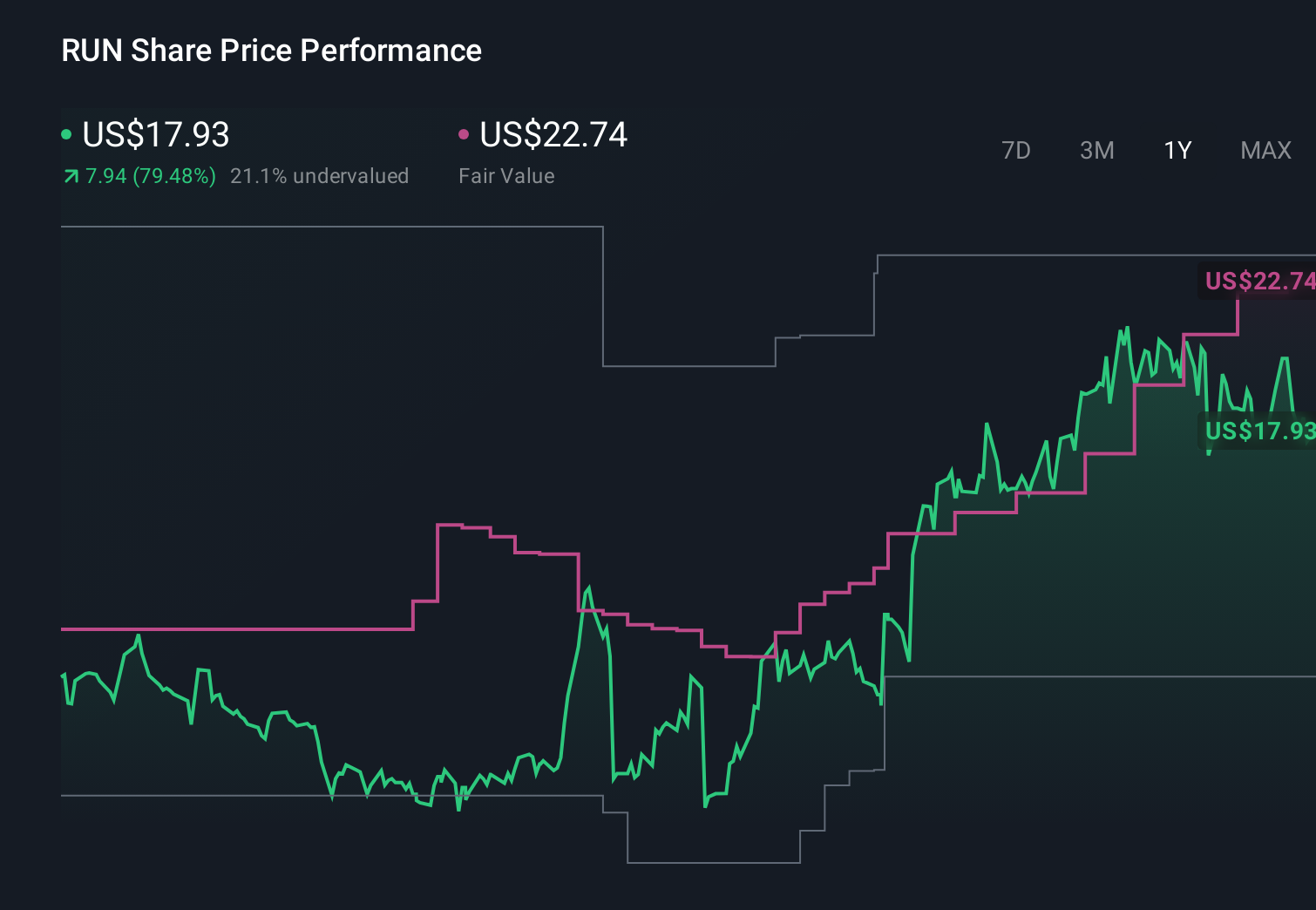

Sunrun’s narrative projects $2.9 billion revenue and $465.4 million earnings by 2028. This requires 10.4% yearly revenue growth and about a $3.1 billion earnings increase from -$2.6 billion today.

Uncover how Sunrun's forecasts yield a $22.20 fair value, a 83% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming flat revenue around US$2.1 billion and tight margins by 2028, so when you see new cuts to near term EPS, it shows just how differently people can view the same company and why it is worth comparing these more pessimistic scenarios with your own expectations before you decide what Sunrun’s recent earnings reset really means for you.

Explore 4 other fair value estimates on Sunrun - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Sunrun research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Sunrun research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sunrun's overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English