Evaluating NOV (NOV) After Mixed Short Term Moves And Contrasting Valuation Signals

Why NOV (NOV) is on investors’ radar today

NOV (NOV) has drawn fresh attention after recent share performance showed a 1 day gain of 0.48%, a 0.36% move over the past week, and a 6.55% decline over the past month.

See our latest analysis for NOV.

Against this backdrop, NOV’s recent pullback over the past month comes after a stronger 90 day share price return of 19.21% and a 1 year total shareholder return of 32.58%. Together, these figures point to momentum that has cooled in the very near term but remains positive over a longer window.

If you are reassessing your energy exposure after NOV’s move, it can be useful to see what else is driving the sector, including infrastructure tied to power grids and transmission, by scanning 27 power grid technology and infrastructure stocks

With NOV trading at US$18.68, below both an analyst price target of US$19.90 and an estimated intrinsic value gap of roughly 35%, the key question is whether this indicates a potential opportunity or a market that is already incorporating expectations of future growth into the price.

Most Popular Narrative: 11% Overvalued

On the widely followed narrative, NOV’s fair value sits at $16.88 compared with the latest close at $18.68, so the story assumes a premium to that estimate.

Sustained investment in energy infrastructure, including LNG and gas processing driven by global energy security needs and rising energy demand in developing markets, supports long-term growth in NOV's composite pipe, process systems, and related offerings, enhancing recurring and project-based revenues. (Revenue)

Want to see what kind of revenue profile and profit margins sit behind that fair value and premium pricing? The core assumptions mix slow top line growth, firmer margins and a future earnings multiple that undercuts many peers.

Result: Fair Value of $16.88 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still the risk that weaker North American drilling and more aggressive customer pricing could pressure NOV’s revenues and squeeze margins if conditions soften further.

Find out about the key risks to this NOV narrative.

Another View: Cash Flows Point a Different Way

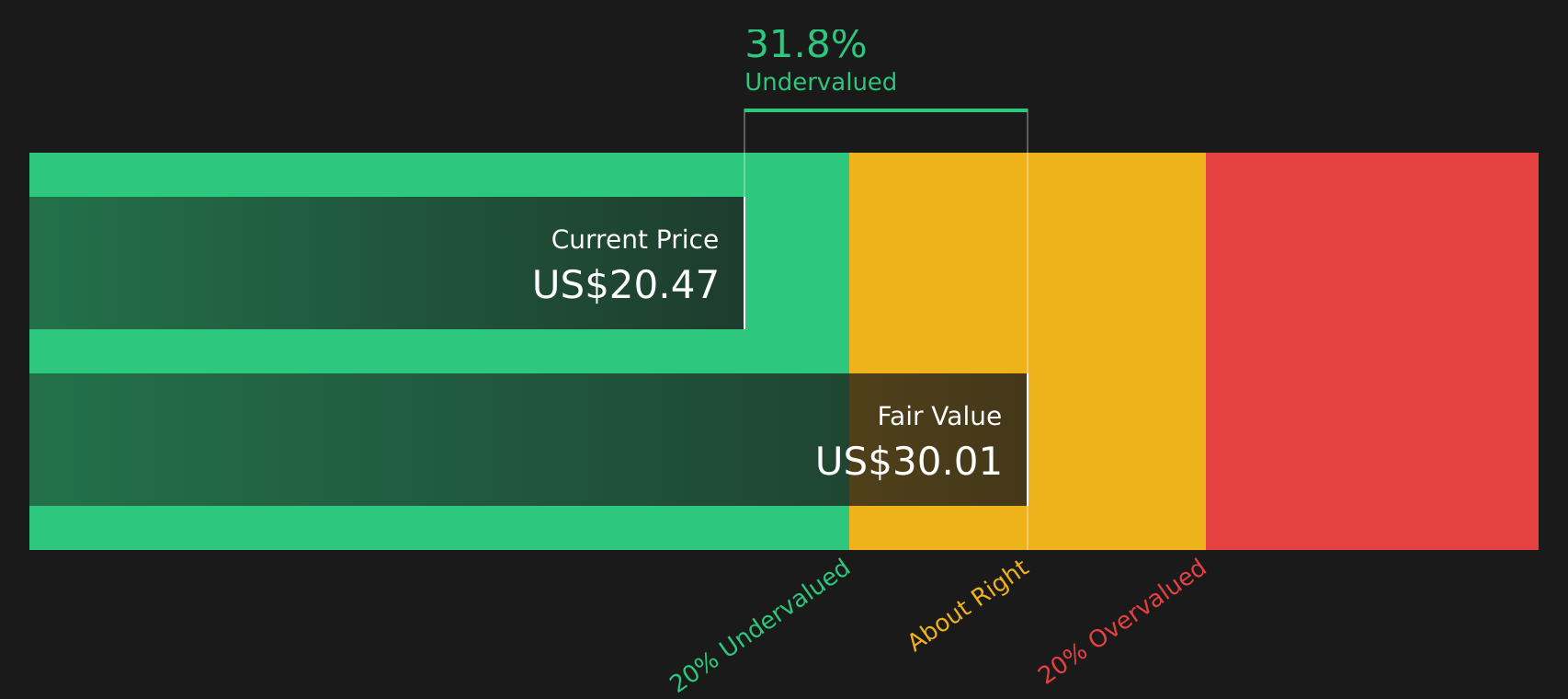

While the popular narrative frames NOV as about 11% overvalued at a fair value of $16.88 versus the current $18.68, the SWS DCF model points the other way. On that approach, NOV’s estimate of future cash flow value sits at $28.56, suggesting the shares trade at a sizable discount.

When two methods disagree this sharply, it raises a simple question for you as an investor: are earnings multiples or long term cash flows the yardstick you trust more for NOV?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NOV for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and expectations, it helps to look past the headline and into the details yourself. Then act while the data is fresh by weighing NOV’s 2 key rewards and 4 important warning signs

Looking for more investment ideas?

If NOV has you thinking about what else might belong on your radar, now is a good time to line up a few more names to research carefully.

- Target long term compounding potential by scanning 52 high quality undervalued stocks that pair quality fundamentals with what may be attractive entry prices.

- Strengthen your income game by reviewing 13 dividend fortresses that focus on higher yields backed by balance sheet support.

- Put resilience first by checking 68 resilient stocks with low risk scores that screen for lower risk profiles so you are not relying on just one story.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English