How Wayfair’s Exit From the S&P Homebuilders Index (W) Has Changed Its Investment Story

- In March 2026, Wayfair Inc. was removed from the S&P Homebuilders Select Industry Index, reflecting a reclassification of its role within the broader home-related sector.

- This index exit can matter for investors because it may alter institutional and index-fund ownership patterns, potentially changing how the market assesses Wayfair’s profile.

- Next, we will examine how Wayfair’s removal from the S&P Homebuilders Select Industry Index might reshape its existing investment narrative.

This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

Wayfair Investment Narrative Recap

To own Wayfair, you need to believe it can turn a large, still-unprofitable home goods platform into a more efficient and higher margin business, helped by logistics, tech, and retail investments. Its removal from the S&P Homebuilders Select Industry Index is more about classification than fundamentals and does not materially change the key near term catalyst of efficiency gains, or the biggest risk, which remains a pressured home and big-ticket furniture market.

The index exit lands just as Wayfair is leaning into physical stores, with a second large format location opening in Atlanta at the end of March 2026. For investors focused on catalysts, these stores, alongside initiatives like CastleGate and Wayfair Verified, sit at the heart of the thesis that better service and omnichannel reach can support higher conversion, even while macro and housing related headwinds remain a concern.

Yet behind the optimism, investors should also be aware that persistently high customer acquisition costs could...

Read the full narrative on Wayfair (it's free!)

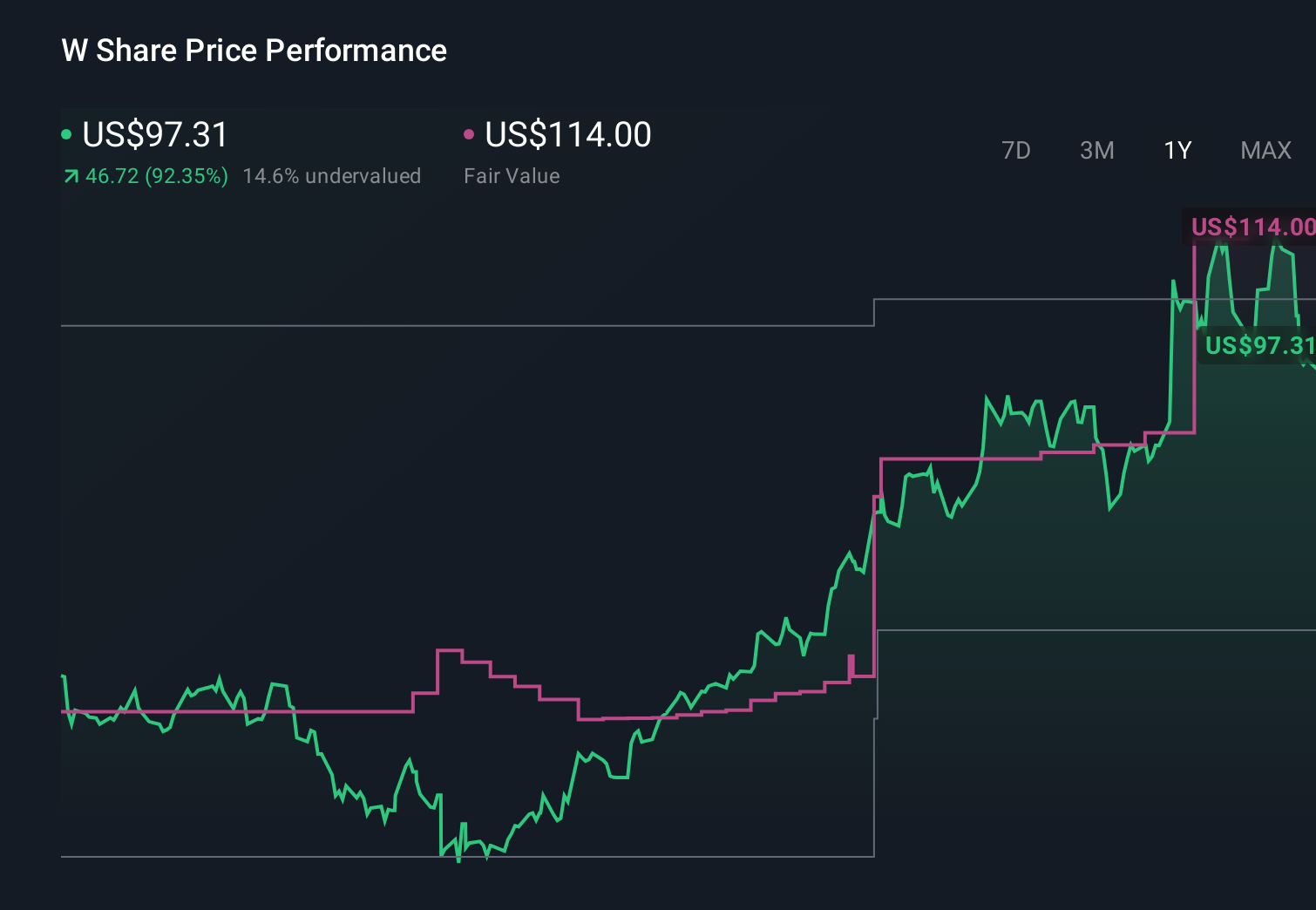

Wayfair’s narrative projects $13.9 billion revenue and $124.7 million earnings by 2028.

Uncover how Wayfair's forecasts yield a $113.64 fair value, a 42% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts paint a much tougher picture, assuming roughly 3.4 percent annual revenue growth and no profitability by 2028, which contrasts sharply with more optimistic views and invites you to weigh how this index removal might shift already cautious expectations.

Explore 4 other fair value estimates on Wayfair - why the stock might be worth 44% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Wayfair research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wayfair research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wayfair's overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Find 55 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English