A Look At NOV (NYSE:NOV) Valuation As It Commits US$200 Million To Subsea Capacity Expansion

NOV (NOV) plans to invest US$200 million over three years to roughly double capacity at its subsea flexible pipe facility in Açu, Brazil, addressing a backlog extending into 2028 and supporting deepwater projects.

See our latest analysis for NOV.

The Açu expansion news comes after a period of stronger share price momentum, with a 90 day share price return of 27.27% and a 1 year total shareholder return of 37.81% from a US$19.88 starting point. Over longer periods, the 3 year total shareholder return of 15.03% and 5 year total shareholder return of 52.63% point to more mixed outcomes.

If this subsea expansion has you thinking about where else capital intensive energy infrastructure could matter, it may be worth checking out 26 power grid technology and infrastructure stocks

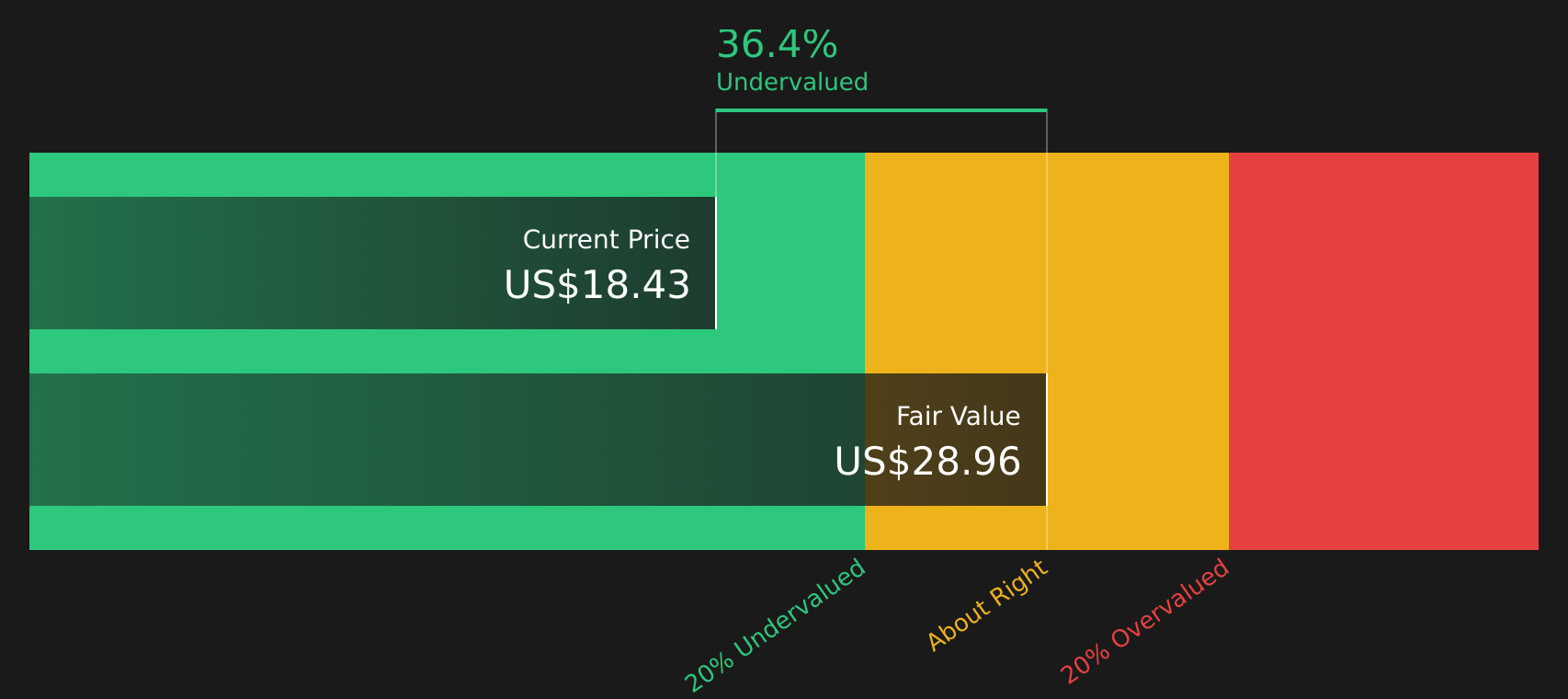

With NOV trading near its US$19.90 analyst price target but showing a roughly 31% intrinsic discount estimate, the key question is whether today’s valuation leaves room for upside or if the market already reflects expectations for future growth.

Most Popular Narrative: 17.8% Overvalued

With NOV closing at $19.88 against a narrative fair value of $16.88, the widely followed view is that the current price sits ahead of those assumptions, with that gap framed using a 7.63% discount rate.

Fair Value: nudged higher from US$16.33 to US$16.88, representing a small uplift in the implied estimate per share.

Discount Rate: trimmed slightly from 7.75% to 7.63%, which modestly increases the present value of projected cash flows.

Interested in why a modest tweak to growth, margins and the future P/E still points to an overvaluation gap at today’s price? The full narrative shows how long term earnings and cash flow assumptions, paired with that lower discount rate, are doing the heavy lifting behind the $16.88 fair value.

Result: Fair Value of $16.88 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this narrative still depends on offshore and international activity picking up, while tariffs, inflation, and irregular project orders could easily challenge those assumptions.

Find out about the key risks to this NOV narrative.

Another Angle On Value

Analyst models and narrative fair values currently suggest NOV is 17.8% overvalued at $19.88, yet the Simply Wall St DCF model points to a fair value of $28.76, implying the shares trade at about a 31% discount. Which set of assumptions do you find more convincing for the long term?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NOV for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 61 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly mixed between risks and rewards, it makes sense to review the numbers yourself and decide how comfortable you are with the trade off before relying on the 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If NOV has you thinking more broadly about where to put your money to work, do not stop here, you could miss opportunities that fit you better.

- Target higher quality at sensible prices by scanning 61 high quality undervalued stocks that combine fundamentals with more grounded valuations.

- Strengthen income potential by reviewing 12 dividend fortresses that focus on 5%+ yields with an eye on durability.

- Dial down risk by comparing 67 resilient stocks with low risk scores that score well on resilience before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English