Talen Energy (TLN) Is Up 7.1% After Nuclear SMR LOI With X-energy - Has The Bull Case Changed?

- On 19 March 2026, X-energy Reactor Company and Talen Energy signed a Letter of Intent to assess deploying X-energy's Xe-100 small modular reactors in Pennsylvania and across the PJM market, including feasibility studies, site evaluations, and a potential transition of fossil-fired sites to nuclear.

- This early-stage collaboration highlights a possible path for Talen to expand clean baseload capacity while reusing existing transmission infrastructure and workforce at legacy fossil generation sites.

- Next, we'll examine how this potential use of Xe-100 reactors to repurpose fossil-fired sites could influence Talen Energy's investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Talen Energy Investment Narrative Recap

To own Talen, you need to believe its mix of nuclear, gas, and grid-adjacent assets can convert rising PJM power demand into durable cash flow, while its leverage and fossil exposure remain manageable. The new X-energy Letter of Intent potentially speaks directly to both the key near term catalyst, expanding reliable low carbon capacity, and the dominant risk, being too tied to fossil plants if decarbonization policies tighten.

Among recent announcements, the 1,920 megawatt carbon free nuclear contract with AWS through 2042 feels most relevant here. That long term, inflation linked revenue anchor already ties Talen’s nuclear capabilities to data center demand. The Xe 100 SMR exploration could, if it progresses, fit beside that AWS deal as another way to reuse existing sites for cleaner baseload capacity while supporting the same growth theme.

Yet, against this potential, investors should be aware that concentrated fossil assets, rising leverage, and policy shifts could still...

Read the full narrative on Talen Energy (it's free!)

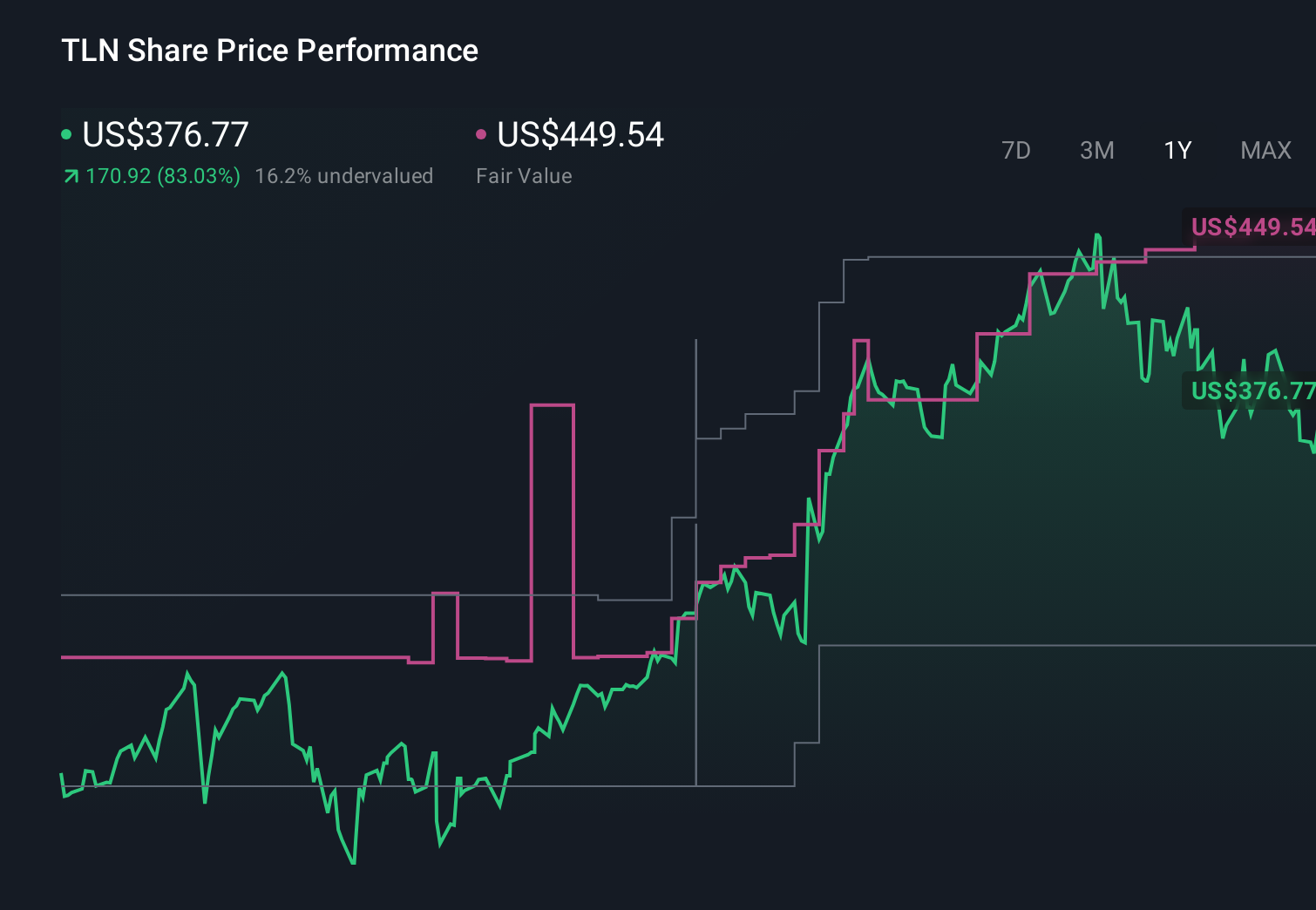

Talen Energy's narrative projects $4.2 billion revenue and $1.1 billion earnings by 2028. This requires 25.1% yearly revenue growth and about a $913.0 million earnings increase from $187.0 million today.

Uncover how Talen Energy's forecasts yield a $462.97 fair value, a 43% upside to its current price.

Exploring Other Perspectives

While consensus sees upside from SMRs and data centers, the most cautious analysts expected only about US$3.2 billion of revenue and US$1.1 billion of earnings by 2028, so this kind of news could push you to rethink which narrative you find more convincing.

Explore 7 other fair value estimates on Talen Energy - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Talen Energy research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Talen Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Talen Energy's overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English