A Look At Harley-Davidson (HOG) Valuation After Workforce Cuts And Weaker Profitability

Harley-Davidson (HOG) has moved back into focus after announcing global workforce reductions and outlining plans to tackle weaker demand, higher tariff costs, and recent revenue and profit declines.

See our latest analysis for Harley-Davidson.

Harley-Davidson’s recent workforce cuts and weaker results have come alongside a 7-day share price return of 10.75%. However, the 1-year total shareholder return of 20.05% and 5-year total shareholder return of 45.95% show longer term momentum has faded.

If this kind of restructuring story has you reviewing your watchlist, it could be a good moment to broaden your search and check out 20 top founder-led companies

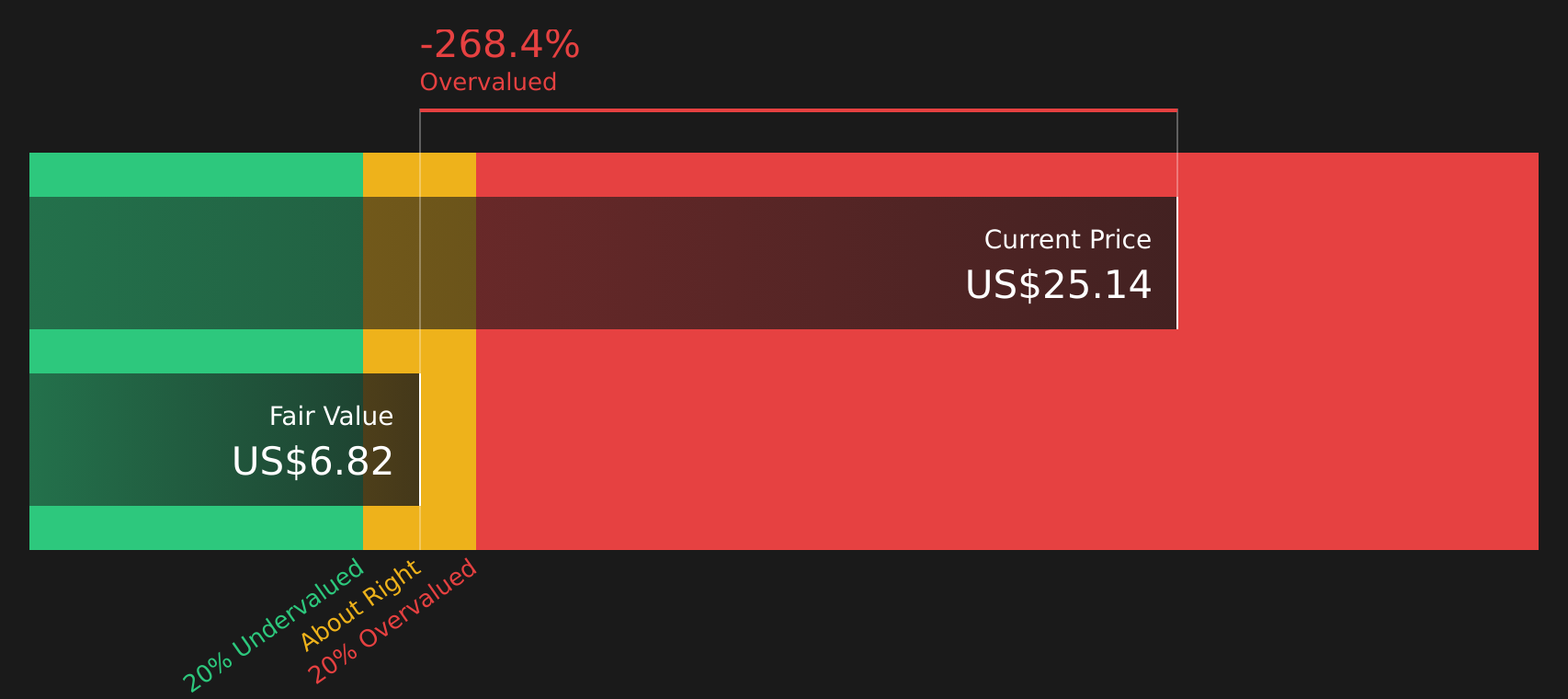

With revenue and profit under pressure, a recent share price rebound, and the stock trading below the latest analyst price target, you have to ask: Is Harley-Davidson undervalued, or is the market already pricing in any future recovery?

Most Popular Narrative: 11.5% Undervalued

Harley-Davidson's most followed narrative puts fair value at $22, compared with the last close of $19.47, and builds a case around financing flexibility and product repositioning.

The new partnership in HDFS unlocks significant cash ($1.25B) and reduces leverage, enabling accelerated share buybacks and freeing up $300M for growth investments, which can directly bolster EPS and future revenue streams through both financial engineering and new business initiatives.

Curious how a shrinking top line and thinner margins still produce that valuation? The narrative leans heavily on capital returns, product mix, and a richer future earnings multiple.

Result: Fair Value of $22 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh weak heavyweight motorcycle demand and dealer pressures, along with tariff costs that could squeeze margins and challenge that 11.5% upside case.

Find out about the key risks to this Harley-Davidson narrative.

Another View: DCF Points The Other Way

The popular narrative sees Harley-Davidson as 11.5% undervalued at $22 fair value, but the SWS DCF model lands closer to $16.15, which would imply the shares are priced above estimated future cash flows.

If earnings are forecast to shrink and cash flow points to a lower value, the key question is how much weight to give the cash flow math compared with the analyst multiple story.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Harley-Davidson for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 61 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed messages or just a complex story that needs a closer look? Use the full data set and sentiment breakdown to form your own view with 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If Harley-Davidson has sharpened your thinking, now is the time to widen your search and compare it with other focused stock ideas tailored to different goals.

- Target higher yield potential by scanning companies that pay robust income and have been grouped as 12 dividend fortresses

- Zero in on quality at a reasonable price by reviewing companies flagged as 61 high quality undervalued stocks

- Prioritize resilience by checking businesses identified through the 67 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English