A Look At Olema Pharmaceuticals (OLMA) Valuation After Earnings And New Shelf Registration Filing

Why Olema’s latest earnings and shelf filing matter for investors

Olema Pharmaceuticals (OLMA) has drawn fresh attention after reporting fourth quarter and full year 2025 results, along with a new shelf registration of up to US$71.82 million in common stock.

The company posted a fourth quarter net loss of US$46.06 million and a full year 2025 net loss of US$162.45 million. It also registered 4,882,586 shares for an ESOP related offering that could affect future dilution and funding flexibility.

See our latest analysis for Olema Pharmaceuticals.

The earnings update and new shelf registration landed after a sharp 30 day share price return of around a 44% decline and a year to date share price return of around a 46% decline. However, the 1 year total shareholder return is very large and the 3 year total shareholder return is close to 3x. Together, these figures point to strong long term gains but fading recent momentum as investors reassess funding needs and execution risks.

If Olema’s recent swings have you thinking about diversification, this could be a good moment to scan for other healthcare names harnessing AI in their pipelines via our screener of 34 healthcare AI stocks.

With the stock down sharply in recent months, yet still showing very large 1 year and close to 3x 3 year total returns, and trading at a discount to analyst targets, is this a fresh opportunity or is future growth already priced in?

Preferred Price to Book of 2.5x: Is it justified?

On simple metrics, Olema looks attractively priced against peers but still carries a premium to the broader US biotech group, which gives mixed valuation signals at the last close of $13.67.

The preferred metric here is the price to book ratio, or P/B. At 2.5x, Olema trades below the peer average of 4x, which points to a cheaper entry price compared to similar companies assessed on this framework. At the same time, this valuation sits above the wider US biotech industry average P/B of 2.2x, so the shares are not at the very low end of the sector range.

This blend of a discount to peers and a premium to the sector suggests the market is assigning some value to Olema’s pipeline and forecast revenue growth, while still keeping the stock priced below closer comparables. If sentiment or fundamentals shift, that relative positioning could move closer to either the cheaper industry level or the higher peer group level.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price to book ratio of 2.5x (ABOUT RIGHT)

However, recent share price declines and ongoing net losses of US$162.45 million mean that any funding setbacks or clinical disappointments could quickly flip sentiment on Olema.

Find out about the key risks to this Olema Pharmaceuticals narrative.

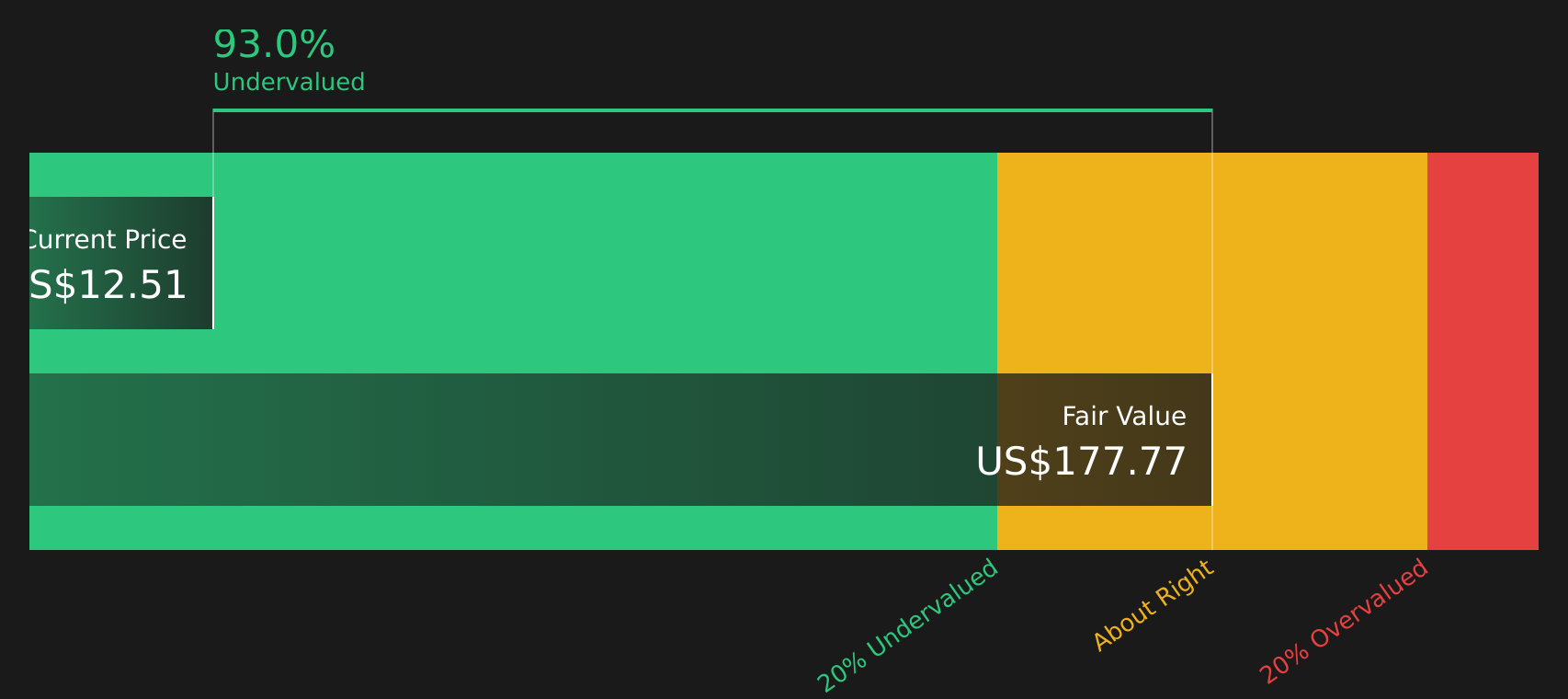

Another view using the SWS DCF model

The earlier lens using a 2.5x P/B ratio suggested Olema sits between peer cheap and sector average. The SWS DCF model points in the same direction, with an estimated fair value of $18.83 versus a current price of $13.67, implying the shares trade at about a 27% discount.

That gap highlights a tension you need to weigh: whether the discount reflects genuine mispricing or simply the reality of an unprofitable, volatile biotech that is forecast to remain loss making for at least three years.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Olema Pharmaceuticals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 62 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals or early opportunity: either way, you do not want to rely only on headlines when the data is this split. Take a closer look at the 2 key rewards and 5 important warning signs.

Looking for more investment ideas?

If Olema has sparked your interest, do not stop here. Broaden your watchlist with focused stock ideas that fit different roles in your portfolio.

- Target potential mispricing by scanning 62 high quality undervalued stocks that combine quality traits with prices that may not fully reflect their fundamentals.

- Strengthen your core holdings by reviewing solid balance sheet and fundamentals stocks screener (39 results) that aim to keep financial risk in check.

- Get ahead of the crowd by uncovering a screener containing 25 high quality undiscovered gems before attention and liquidity catch up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English