Why VinFast Auto (VFS) Is Up 18.5% After EV Deliveries Jump Despite Deeper 2025 Losses

- VinFast Auto’s recently reported fourth-quarter 2025 results showed revenue rising to VND 39,411.71 billions, while quarterly net loss widened to VND 35,101.20 billions, and full-year 2025 revenue almost doubled to VND 90,427.61 billions alongside a larger annual loss of VND 97,041.89 billions.

- Despite these heavier losses, VinFast highlighted a very large quarter-over-quarter surge in electric vehicle deliveries, underpinned by expanding international offerings such as the VF 8 in Canada, which combines federal incentives eligibility with an extensive 10‑year vehicle and battery warranty.

- We’ll now examine how this combination of sharply higher EV deliveries and still‑sizeable losses could reshape VinFast Auto’s investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

VinFast Auto Investment Narrative Recap

To own VinFast Auto today, you have to believe that rapid growth in electric vehicle deliveries can eventually outrun heavy losses and funding pressures. The latest results show revenue scaling quickly but losses remaining very large, so the near term catalyst is still delivery growth and pricing power, while the biggest risk remains liquidity and potential dilution. This earnings release reinforces, rather than changes, that core trade off for shareholders.

Among recent developments, management’s reaffirmed 2026 target of 300,000 EV deliveries stands out next to the Q4 jump in volumes. That guidance leans heavily on continued traction in Asia and product expansion, including models like the VF 8 in Canada that qualify for federal incentives and come with a lengthy warranty. How efficiently VinFast converts those volume ambitions into better unit economics will likely shape how investors reassess the latest numbers.

Yet behind the impressive delivery targets, investors also need to be aware of the risk that persistent cash burn could force fresh capital raises and dilute existing shareholders...

Read the full narrative on VinFast Auto (it's free!)

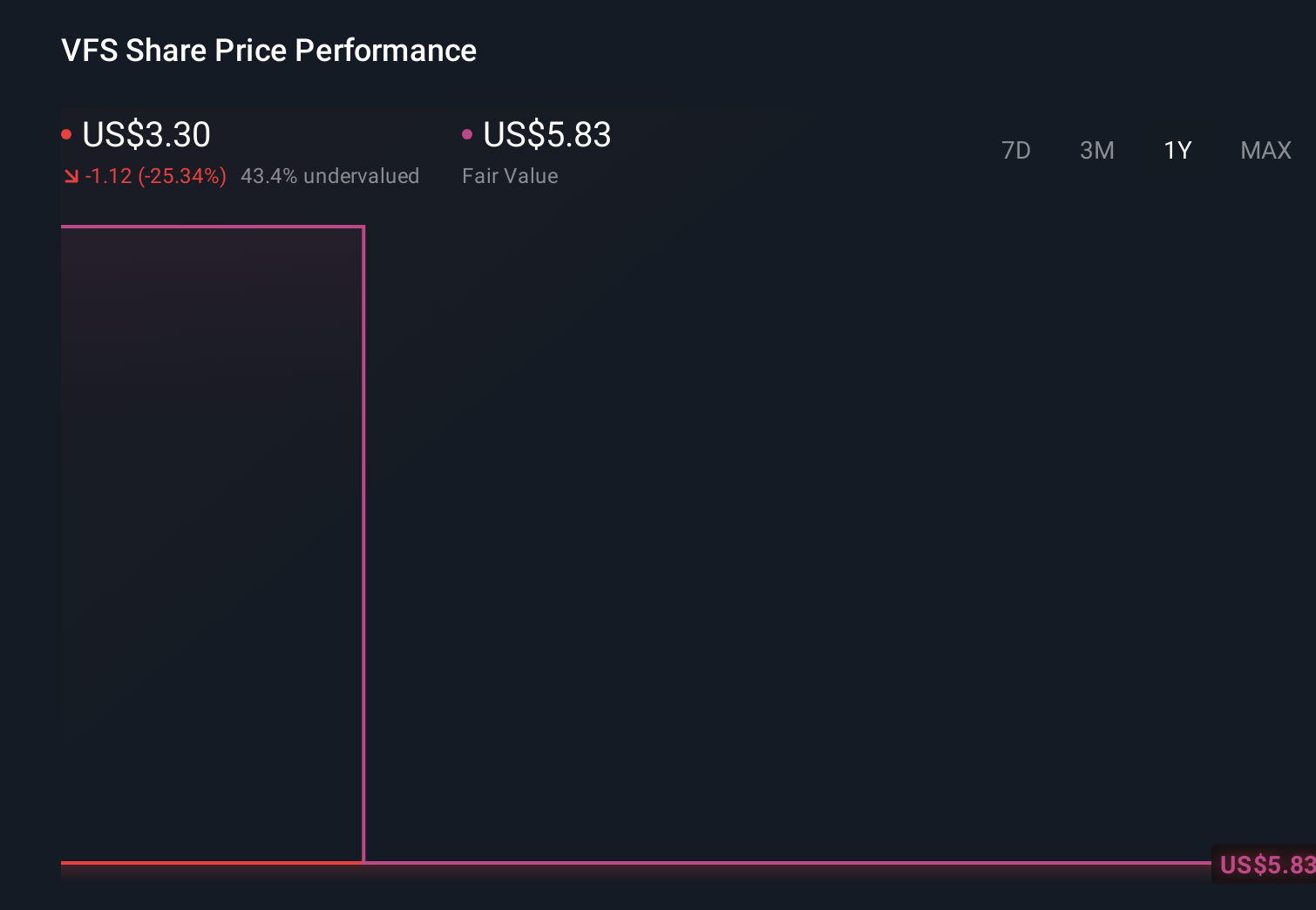

VinFast Auto's narrative projects ₫239006.9 billion revenue and ₫6414.4 billion earnings by 2029. This requires 38.3% yearly revenue growth and an earnings increase of about ₫1.01 trillion from -₫97041.9 billion today.

Uncover how VinFast Auto's forecasts yield a $6.38 fair value, a 88% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming roughly 41 percent annual revenue growth and almost ₫9,301.1 billion in earnings by 2028, which is far more upbeat than the consensus view and sits uneasily alongside fresh concerns about execution risk in overseas markets highlighted by these latest results.

Explore 5 other fair value estimates on VinFast Auto - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your VinFast Auto research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free VinFast Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate VinFast Auto's overall financial health at a glance.

No Opportunity In VinFast Auto?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 62 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English