Share Buyback And Risk Pivot Could Be A Game Changer For First Advantage (FA)

- At the March 12, 2026 BofA Securities Information & Business Services Conference, First Advantage Corporation highlighted 17% fourth-quarter revenue growth, a transition toward capital risk management solutions, and board approval of a US$100,000,000 share repurchase program.

- The company’s emphasis on expanding beyond background screening into a broader capital risk management platform, supported by about 97% client retention, underlines management’s confidence in scaling the business model.

- We’ll explore how First Advantage’s US$100,000,000 share repurchase authorization may influence its existing investment narrative around growth, margins, and capital allocation.

Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

First Advantage Investment Narrative Recap

To own First Advantage, you need to believe it can evolve from a background screening vendor into a broader capital risk management platform while improving profitability. The latest conference update, with 17% fourth quarter revenue growth and a US$100,000,000 buyback authorization, supports that ambition but does not remove the near term risk that hiring softness or competitive pricing pressure could weigh on revenue and margins.

The new US$100,000,000 share repurchase program is the announcement most directly tied to this update, because it intersects with the core debate around growth, margin improvement, and how management prioritizes capital between buybacks and further investment in technology, international expansion, and integrating Sterling. How effectively the company balances these uses of cash will shape whether investors see the stock as primarily a growth story, a margin recovery story, or a capital return story.

Yet beneath the company’s confidence, investors should still be aware of how hiring weakness and intense price competition could...

Read the full narrative on First Advantage (it's free!)

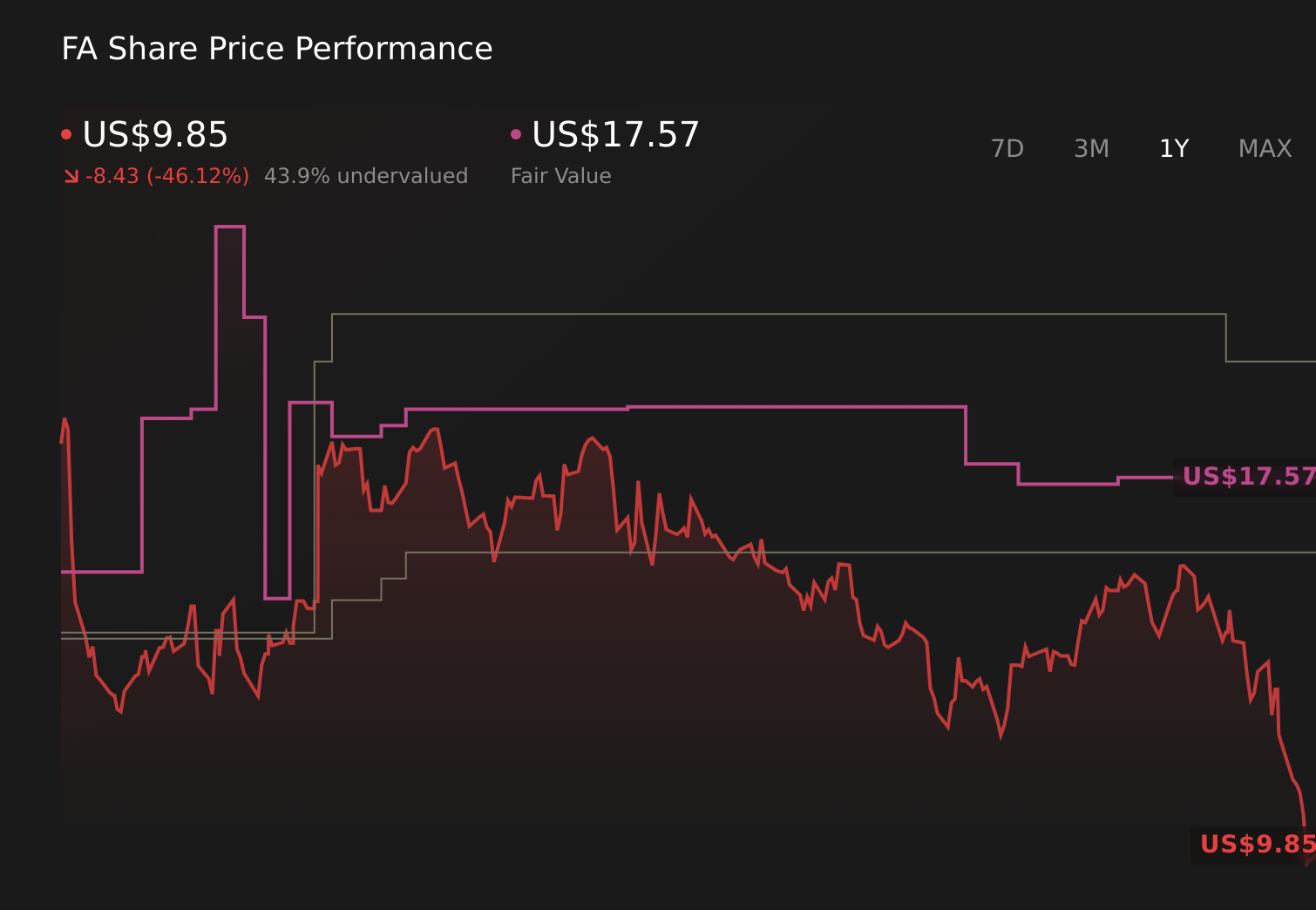

First Advantage's narrative projects $1.9 billion revenue and $168.3 million earnings by 2029. This requires 7.1% yearly revenue growth and a $203.1 million earnings increase from -$34.8 million today.

Uncover how First Advantage's forecasts yield a $15.00 fair value, a 35% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$1,700,000,000 and earnings about US$95,000,000 by 2028, which is a much more upbeat view than consensus. If you compare that optimism with concerns about rising privacy regulation and data access costs, and then layer in First Advantage’s push toward a capital risk platform and fresh buyback news, it is a good moment to consider how your own expectations might differ from both narratives.

Explore another fair value estimate on First Advantage - why the stock might be worth as much as 35% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your First Advantage research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free First Advantage research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate First Advantage's overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 25 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 62 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English