A Look At Waste Management (WM) Valuation As Renewable Gas Investments Draw Focus Before Earnings

Why Waste Management’s renewable gas push matters now

Waste Management (WM) is pouring billions into 20 renewable natural gas plants, a shift that puts regulatory trends, ESG mandates, and carbon credit markets in clearer focus as the upcoming earnings release approaches.

See our latest analysis for Waste Management.

Despite the upcoming earnings focus and the renewable gas build out, WM’s recent price action has been mixed, with a 4.6% 30 day share price decline but a 47.1% three year total shareholder return that points to longer term momentum.

If WM’s renewable push has you thinking more broadly about the energy transition, it could be worth scanning other grid focused names through our 26 power grid technology and infrastructure stocks

With WM trading around US$229.79, a 4.6% 30 day share price decline and a 47.1% three year total return already on the board, the key question is whether today’s valuation still leaves room for upside or if the market is already baking in future growth.

Most Popular Narrative: 9.2% Undervalued

At a last close of $229.79 versus a narrative fair value of $253.12, the current price sits below what the most followed model suggests WM could be worth, with that view anchored on detailed assumptions for revenue, margins, and future earnings power.

The company's strategic investments in sustainability, particularly in the areas of recycling and renewable energy, are showing strong, high return growth, which could drive future revenue increases. The integration and optimization of WM Healthcare Solutions are on track to deliver significant synergies, anticipated to reach $250 million annually by 2027, positively impacting earnings.

Want to see what is sitting behind that valuation gap? The narrative leans on steady top line expansion, thicker margins, and a richer earnings base. Curious which assumptions really move the fair value.

Result: Fair Value of $253.12 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh risks, such as potential tax credit changes and higher leverage from Stericycle, which could pressure margins and limit flexibility if integration stumbles.

Find out about the key risks to this Waste Management narrative.

Another View: What P/E Says About WM’s Price

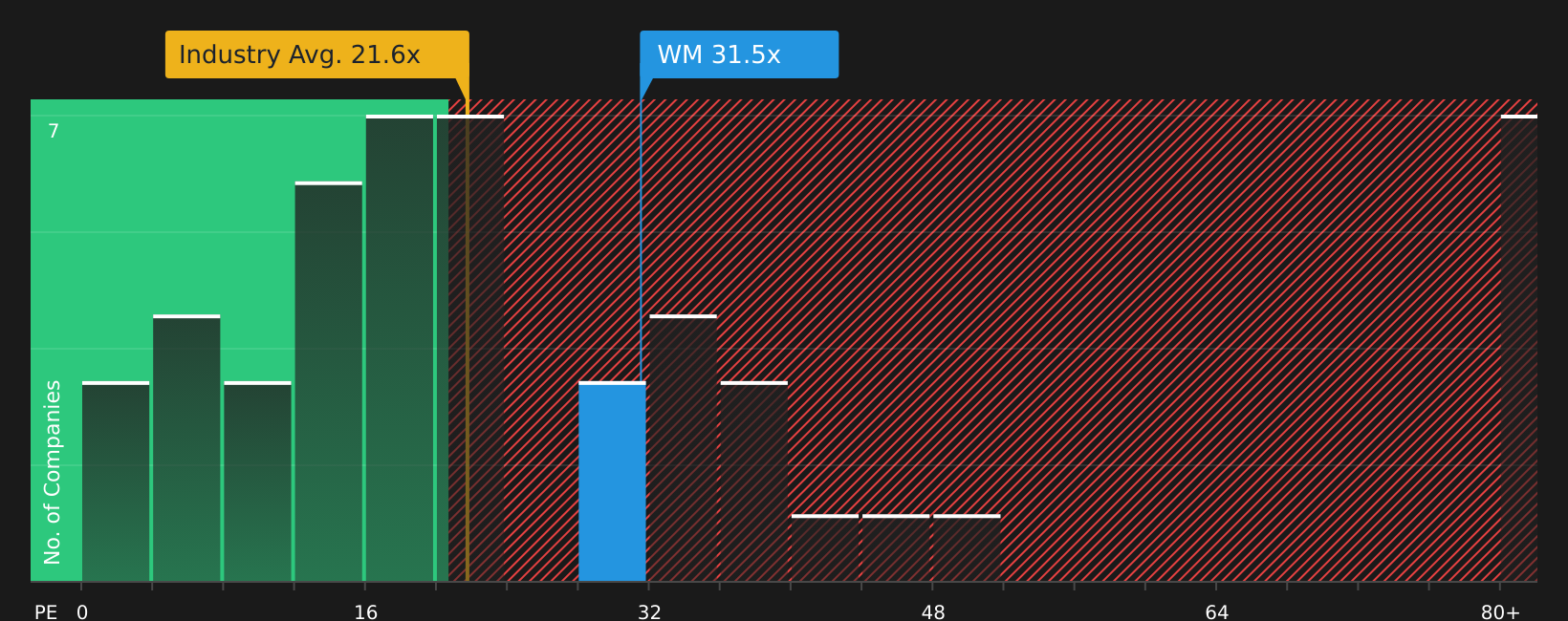

The narrative fair value suggests WM is 9.2% undervalued, but the earnings multiple tells a tighter story. WM trades on a P/E of 34.2x versus a fair ratio of 31.3x, above the US Commercial Services average of 22.2x and slightly below peers at 35.5x. This tilts risk toward the downside if sentiment cools.

For a closer look at how that earnings multiple stacks up and where the market could shift toward the fair ratio, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With both concern and optimism in the mix, it makes sense to move quickly and review the underlying drivers for yourself. You can start with the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If WM has sharpened your thinking, do not stop here. Use the Simply Wall St screener to quickly surface fresh stock ideas that fit your style.

- Target value focused opportunities by checking out companies highlighted in the 58 high quality undervalued stocks that combine quality fundamentals with room for potential re rating.

- Strengthen your core holdings by reviewing the solid balance sheet and fundamentals stocks screener (39 results) and spot businesses with financial foundations that may help them handle tougher conditions.

- Get ahead of the crowd by scanning the screener containing 25 high quality undiscovered gems where fundamentally strong names may still be flying under most investors' radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English