Southern Copper (SCCO) Is Up 7.6% After Unveiling US$19.9 Billion Decade-Long Copper Expansion Plan

- Recently, Southern Copper outlined a long-term plan to invest nearly US$19.90 billion over the next decade to lift copper production toward about 1.6 million tons annually by 2035, even as it anticipates near-term output pressure from weaker ore grades at its Peruvian mines.

- This commitment highlights how one of the industry’s largest reserve holders is positioning itself to be a major future supplier of copper-intensive, energy-transition materials.

- We’ll now examine how Southern Copper’s US$19.90 billion decade-long investment plan could reshape its existing investment narrative.

Rare earth metals are the new gold rush. Find out which 26 stocks are leading the charge.

Southern Copper Investment Narrative Recap

To own Southern Copper, you need to believe its large reserve base and multi-country footprint can support consistent copper production and disciplined capital allocation over time. The US$19.90 billion decade-long plan reinforces the long-term growth story, but it does not materially change the key near-term catalyst, which is how effectively the company manages weaker Peruvian ore grades. It also sharpens the biggest current risk around execution and cost control on such a large capex program.

Against that backdrop, the recent string of dividend increases, including the US$1.00 per share quarterly cash dividend announced in January 2026 alongside solid 2025 results, matters. It ties the long-term growth plan to a track record of returning cash to shareholders, while also raising questions about how future payouts might evolve as capex rises and free cash flow comes under more pressure.

Yet behind the growth plan, investors should also be aware of the mounting capital commitments and what they could mean for...

Read the full narrative on Southern Copper (it's free!)

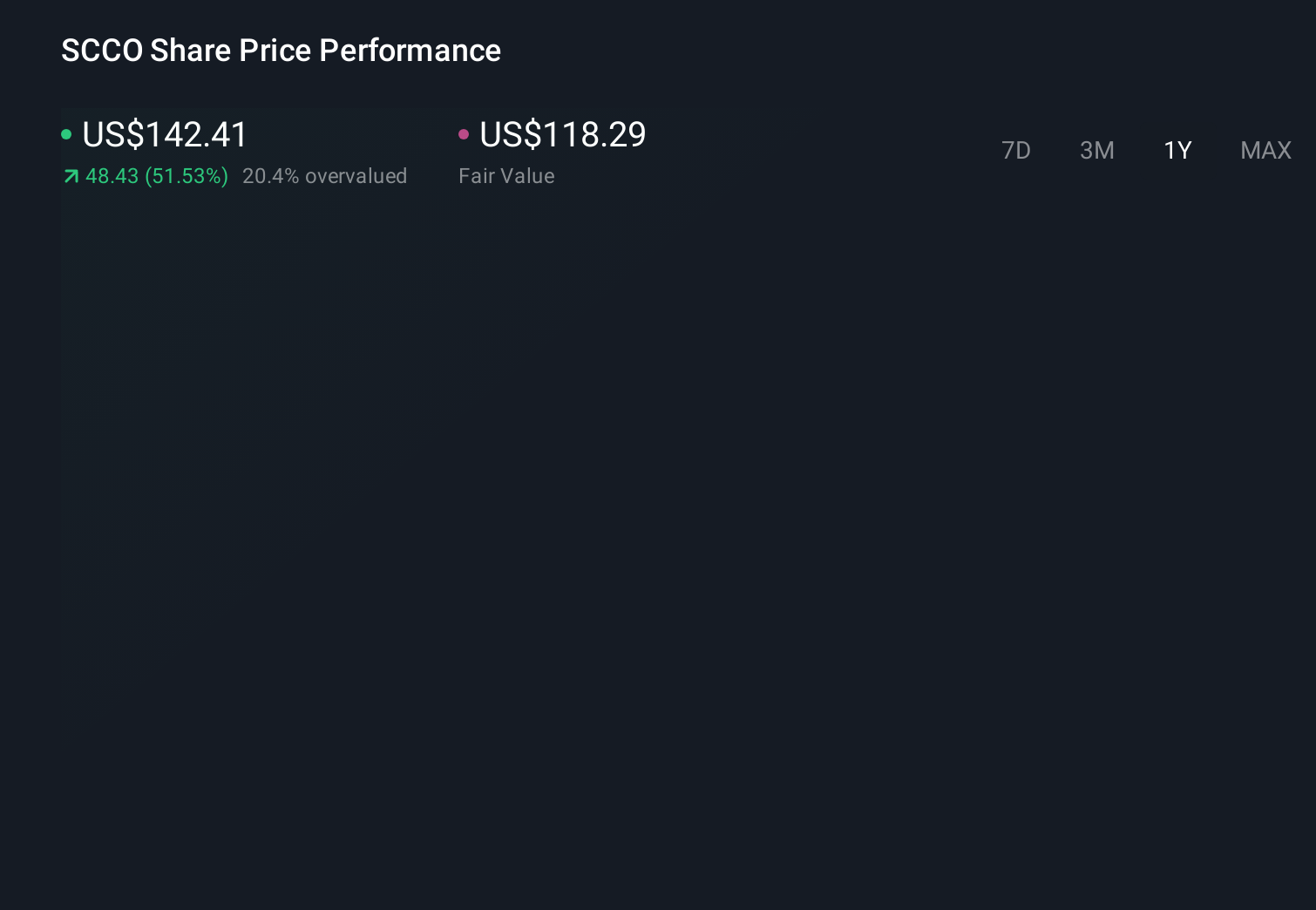

Southern Copper's narrative projects $13.0 billion revenue and $4.3 billion earnings by 2028.

Uncover how Southern Copper's forecasts yield a $149.54 fair value, a 13% downside to its current price.

Exploring Other Perspectives

The most optimistic analysts were already expecting revenue near US$13.7 billion and earnings around US$4.9 billion by 2028, so this new US$19.90 billion plan could either reinforce that upbeat view or expose how sensitive those forecasts are to project delays and higher capital costs.

Explore 5 other fair value estimates on Southern Copper - why the stock might be worth as much as 35% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Southern Copper research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Southern Copper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southern Copper's overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Invest in the nuclear renaissance through our list of 92 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English