Three Undiscovered Asian Gems To Enhance Your Portfolio

As geopolitical tensions and energy price volatility ripple through global markets, Asian equities are navigating a complex landscape with both challenges and opportunities. Amidst this backdrop, the S&P MidCap 400 and Russell 2000 indexes have shown resilience, highlighting the potential for small-cap stocks to thrive in uncertain times. In such an environment, identifying strong fundamentals and growth potential can be key to uncovering undiscovered gems that might enhance a diversified portfolio.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Asian Terminals | 25.82% | 12.05% | 17.00% | ★★★★★★ |

| Thai Steel Cable | NA | 2.06% | 15.66% | ★★★★★★ |

| Central Forest Group | NA | 5.20% | 23.67% | ★★★★★★ |

| Konishi | 0.11% | 1.95% | 8.48% | ★★★★★★ |

| System ResearchLtd | 9.14% | 11.35% | 15.88% | ★★★★★★ |

| Daoming Optics&ChemicalLtd | 14.14% | 3.49% | 9.95% | ★★★★★☆ |

| Sichuan Fulin Transportation Group | 21.07% | 6.25% | 17.69% | ★★★★★☆ |

| Kodama Chemical IndustryLtd | 55.59% | 25.52% | 90.12% | ★★★★★☆ |

| Fengyinhe Holdings | 9.39% | 53.36% | 74.10% | ★★★★☆☆ |

| K BankLtd | NA | 33.37% | 52.70% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

Bank of Gansu (SEHK:2139)

Simply Wall St Value Rating: ★★★★★★

Overview: Bank of Gansu Co., Ltd. operates as a provider of banking and financial services in the People's Republic of China, with a market capitalization of HK$5.12 billion.

Operations: Bank of Gansu generates revenue primarily through its banking and financial services in China. It focuses on interest income from loans and advances, as well as fee-based income from various financial services. The company's net profit margin has shown variability, reflecting changes in operational efficiency and market conditions.

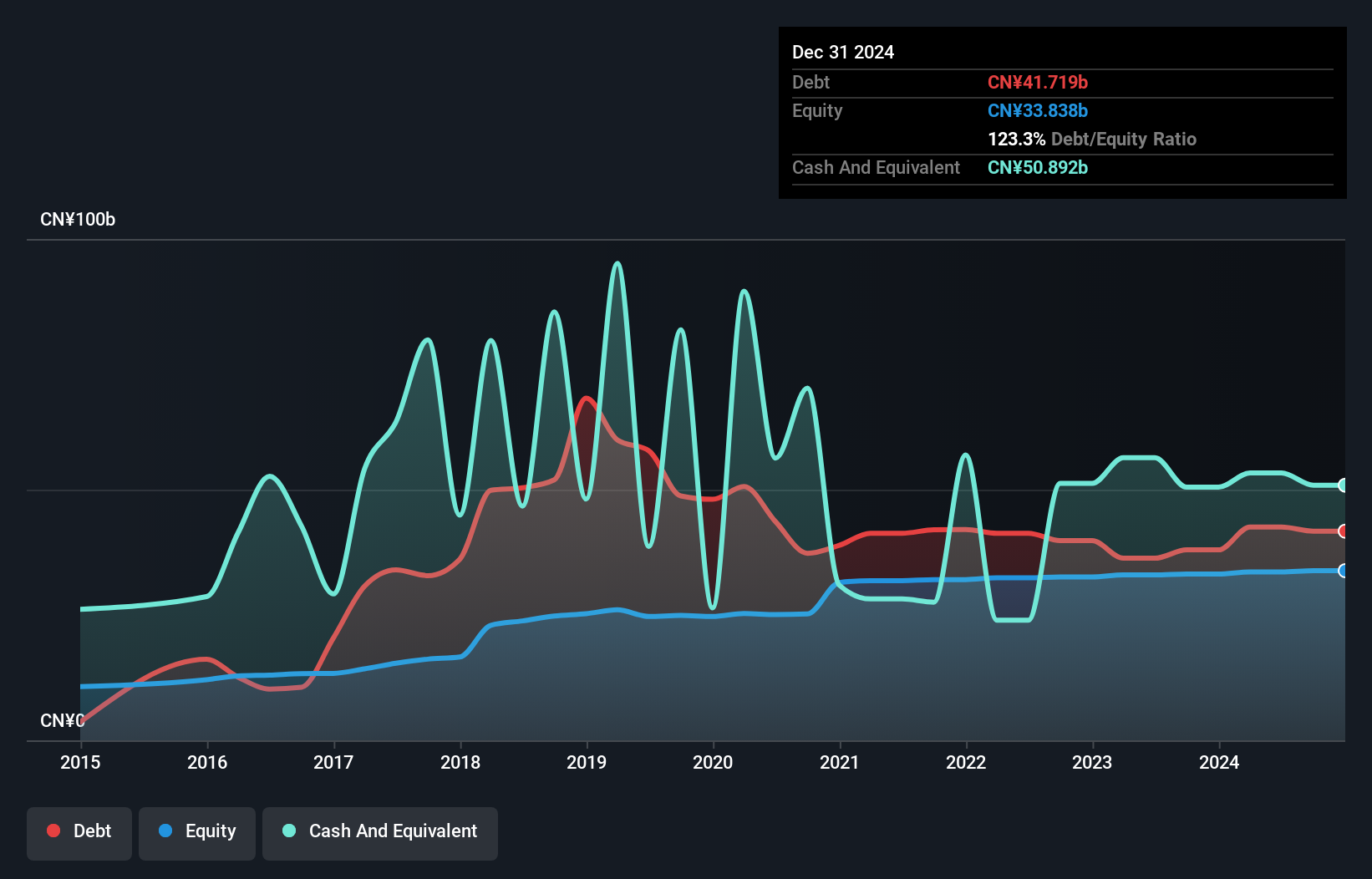

With total assets of CN¥435.9 billion and equity at CN¥34.4 billion, Bank of Gansu presents a compelling profile with its robust deposit base of CN¥335.9 billion and loans totaling CN¥217.9 billion. The bank's price-to-earnings ratio stands attractively at 7.6x, below the Hong Kong market average of 11.9x, suggesting potential value for investors seeking opportunities in smaller financial institutions. Despite earnings growth lagging behind the industry at 1% compared to 4.9%, it boasts a sufficient allowance for bad loans at 137% and maintains an appropriate non-performing loan level of just 1.8%.

- Click here to discover the nuances of Bank of Gansu with our detailed analytical health report.

Gain insights into Bank of Gansu's historical performance by reviewing our past performance report.

Fujian Haixi Pharmaceuticals (SEHK:2637)

Simply Wall St Value Rating: ★★★★★☆

Overview: Fujian Haixi Pharmaceuticals Co., Ltd. is a Chinese company that manufactures and sells pharmaceutical drugs, with a market cap of HK$14.18 billion.

Operations: Fujian Haixi Pharmaceuticals generates revenue primarily through the sale of pharmaceutical drugs in China. The company's financial performance can be analyzed through its gross profit margin, which reflects its efficiency in managing production costs relative to sales.

Fujian Haixi Pharmaceuticals, a nimble player in the pharma sector, reported sales of CNY 582.36 million for 2025, up from CNY 466.68 million the prior year, with net income reaching CNY 177.03 million compared to CNY 136.08 million previously. Earnings growth at 30% outpaced the industry's -6%, highlighting robust performance and high-quality earnings. Their innovative drug platform MultiSel-Opt is advancing HXP056 for retinal diseases into Phase II trials after promising Phase I results showed safety and efficacy in wAMD patients. Despite these strides, regulatory hurdles remain before commercialization can begin in China’s complex market landscape.

Yong Jie New MaterialLtd (SHSE:603271)

Simply Wall St Value Rating: ★★★★★★

Overview: Yong Jie New Material Co., Ltd. specializes in the R&D, manufacturing, and sale of aluminum alloy products globally, with a market cap of CN¥9.38 billion.

Operations: The company generates revenue primarily from the sale of aluminum alloy products. It focuses on research and development to enhance its product offerings. The net profit margin shows significant variation, reflecting fluctuations in production costs and market conditions.

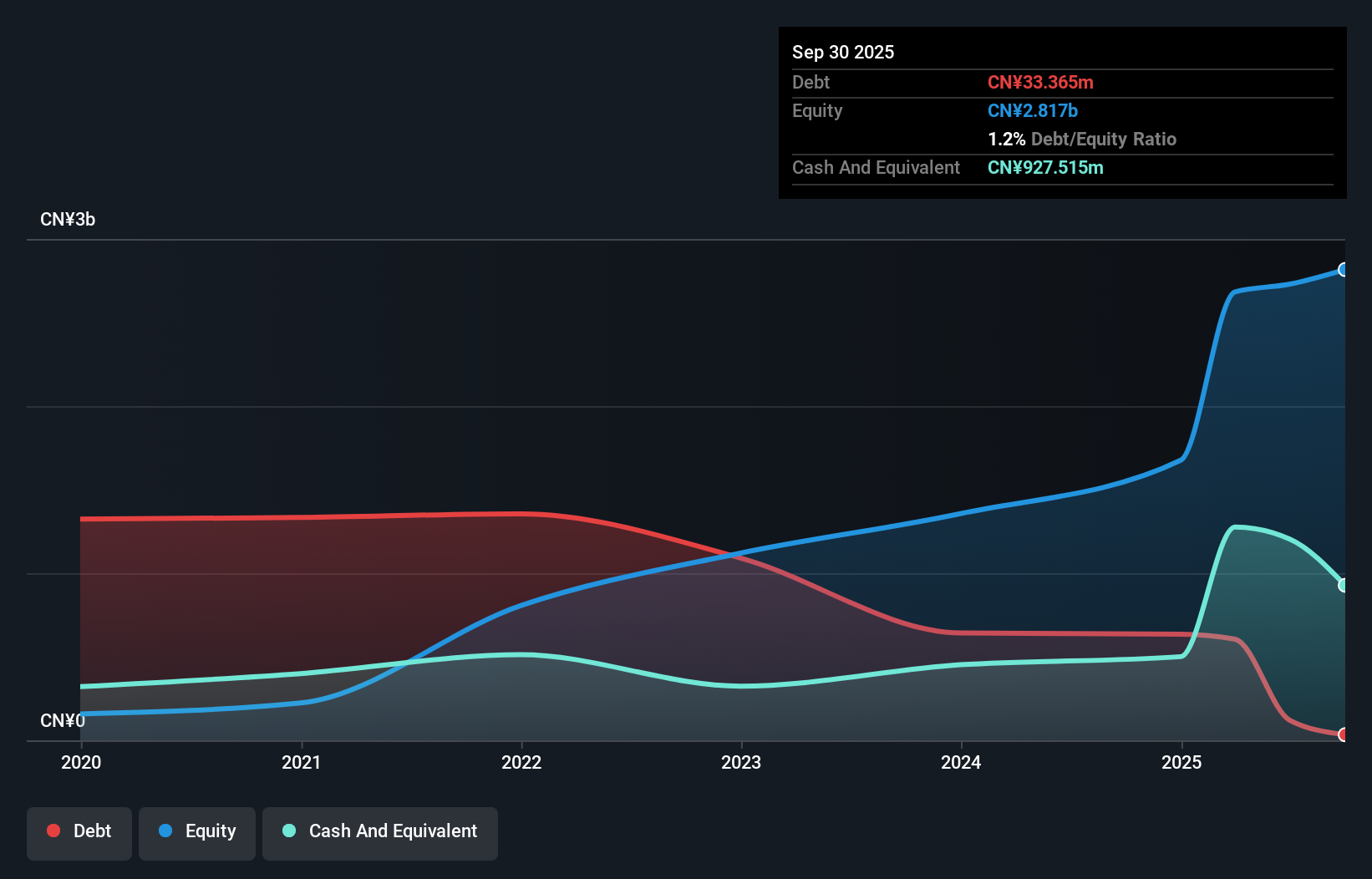

Yong Jie New Material, a nimble player in the metals industry, showcases solid financial footing with a debt-to-equity ratio dropping from 597% to just 1% over five years. The company boasts high-quality earnings and strong interest coverage at 236 times EBIT. Recent performance highlights include sales of CNY 9.64 billion and net income of CNY 415 million for the year ending December 2025, up from CNY 8.11 billion and CNY 319 million respectively a year prior. With basic earnings per share rising slightly to CNY 2.25, Yong Jie seems poised for continued growth amidst industry challenges.

- Click to explore a detailed breakdown of our findings in Yong Jie New MaterialLtd's health report.

Gain insights into Yong Jie New MaterialLtd's past trends and performance with our Past report.

Taking Advantage

- Gain an insight into the universe of 2529 Asian Undiscovered Gems With Strong Fundamentals by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English