Assessing DICK'S Sporting Goods (DKS) Valuation After New Easton Drop Culture Retail Model Launch

Easton’s collaboration with DICK'S Sporting Goods (DKS) on sneaker-style “drop culture” baseball and softball launches has put the retailer’s stock in focus, as investors weigh what limited releases and experiential retail could mean for long term demand.

See our latest analysis for DICK'S Sporting Goods.

At a share price of US$192.13, DICK'S Sporting Goods has seen recent momentum soften, with a 30 day share price return of a 5.84% decline and a 1 year total shareholder return of a 6.87% decline, set against much stronger 3 and 5 year total shareholder returns of 47.73% and 175.02%.

If this kind of product driven buzz interests you, it could be worth broadening your view beyond retailers and checking out 20 top founder-led companies

With short term returns under pressure but multi year performance still strong, the real question is whether DICK'S Sporting Goods at about US$192 is being undervalued, or if the market is already pricing in future growth.

Most Popular Narrative: 19% Undervalued

With DICK'S Sporting Goods last closing at about $192 and the most followed narrative pointing to a fair value near $237, the gap comes down to how earnings power and cash flows are expected to develop over time under a 9.43% discount rate.

The acquisition of Foot Locker is set to expand DICK'S total addressable market, broaden its consumer base, strengthen vendor relationships, and offer synergies (targeting $100 to $125 million), all of which are likely to accelerate top-line growth and operating earnings post-integration.

Want to see what earnings path and margin profile justify that higher fair value, and how comp sales, mix and buybacks fit together in this story.

Result: Fair Value of $237.24 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on Foot Locker being integrated smoothly and on physical store investments paying off, since missteps in either could weigh on margins and earnings power.

Find out about the key risks to this DICK'S Sporting Goods narrative.

Another Angle On Value

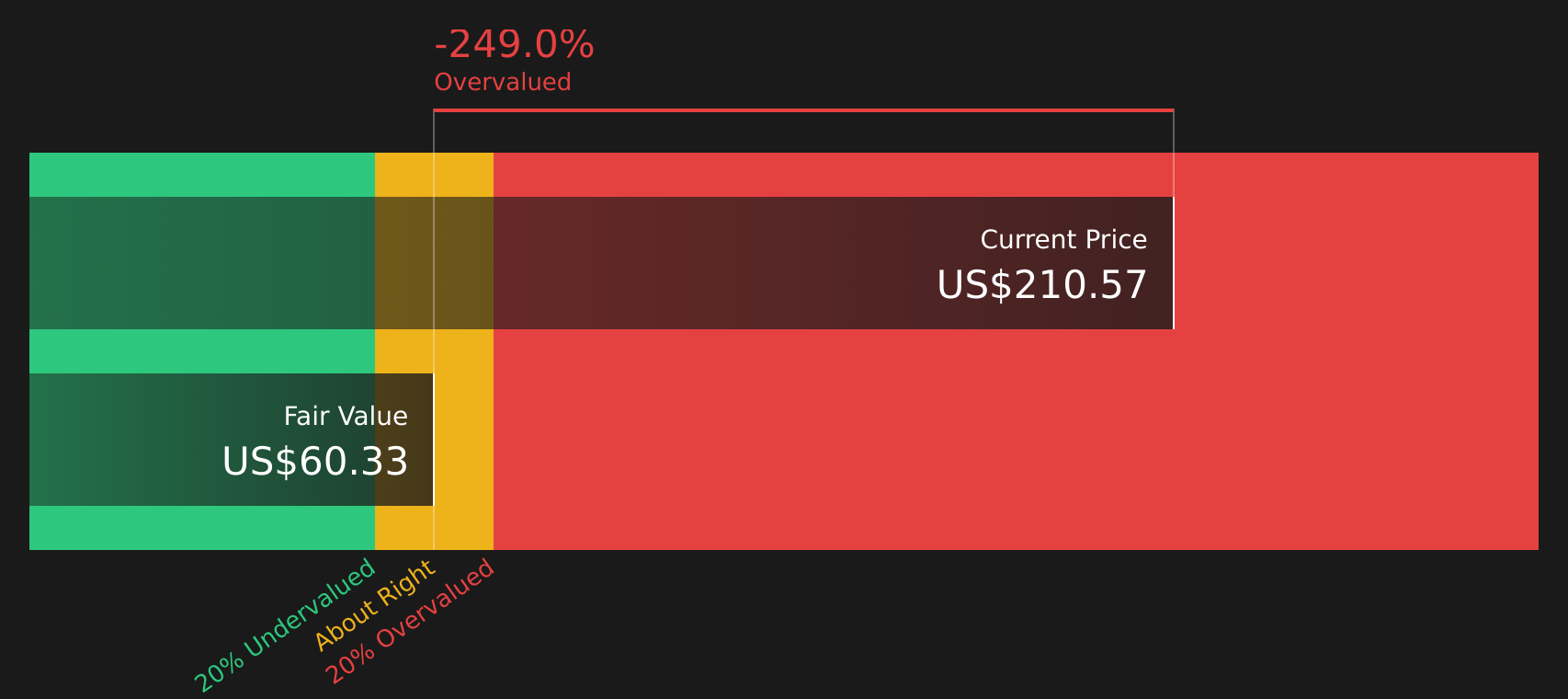

There is a sharp contrast between the narrative fair value of about $237 and the SWS DCF model, which puts DICK'S Sporting Goods at $60.57 per share. One view treats earnings power as more durable; the DCF view prices in much more conservative future cash flows. Which lens do you trust more for a long term call?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out DICK'S Sporting Goods for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 63 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed sentiment running through this story, it makes sense to check the underlying data yourself, move quickly if needed, and weigh both sides of the thesis with 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If you are still weighing what to do with DICK'S Sporting Goods, you can give yourself an edge by comparing it with other high quality ideas filtered by clear rules.

- Scan 63 high quality undervalued stocks to identify potential mispricings that combine strong fundamentals with prices that may not fully reflect their strengths.

- Review 12 dividend fortresses to find income-focused opportunities built around companies offering yields of 5% or more.

- Consider 65 resilient stocks with low risk scores to focus on ideas that pair financial resilience with lower risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English