Assessing Antero Midstream (AM) Valuation After Recent Share Price Pullback And Conflicting Fair Value Signals

Why Antero Midstream is on investors’ radar today

Antero Midstream (AM) has been drawing fresh attention after recent share price moves, with the stock showing a 1.1% decline over the last day and a 4.4% pullback over the past week.

At a last close of US$22.55 and a market value of about US$10.8b, the midstream operator’s recent performance sits between a 1.6% decline over the past month and a 26.8% gain over the past 3 months.

See our latest analysis for Antero Midstream.

Even with the recent pullback, the 25.7% year to date share price return and 28.6% one year total shareholder return suggest momentum has been positive. However, shorter term sentiment has cooled as investors reassess growth prospects and risks.

If you are weighing Antero Midstream against other opportunities in energy infrastructure, it can be useful to scan similar themes in power and grid-related names using our 27 power grid technology and infrastructure stocks

With Antero Midstream trading near US$22.55, a price target close to US$21.86 and an intrinsic value estimate that implies a large discount, the key question is whether the market is already baking in future growth or leaving a genuine entry point on the table.

Most Popular Narrative: 4.5% Overvalued

With Antero Midstream last closing at $22.55 and the most followed fair value estimate at $21.57, the narrative frames the current price as slightly ahead of fundamentals while still leaning on a cash flow and buyback story.

Accelerated debt reduction and opportunistic share buybacks, fueled by strong free cash flow and reduced interest expenses, are improving the company's financial flexibility and are likely to drive earnings per share and equity value higher over the long term.

Curious what kind of revenue path, margin profile, and earnings multiple are baked into that fair value line? The key assumptions behind it are far from conservative.

Result: Fair Value of $21.57 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that fair value story can quickly change if Antero Resources scales back activity in Appalachia, or if tighter environmental rules push up compliance and project costs.

Find out about the key risks to this Antero Midstream narrative.

Another View: Cash Flows Paint a Different Picture

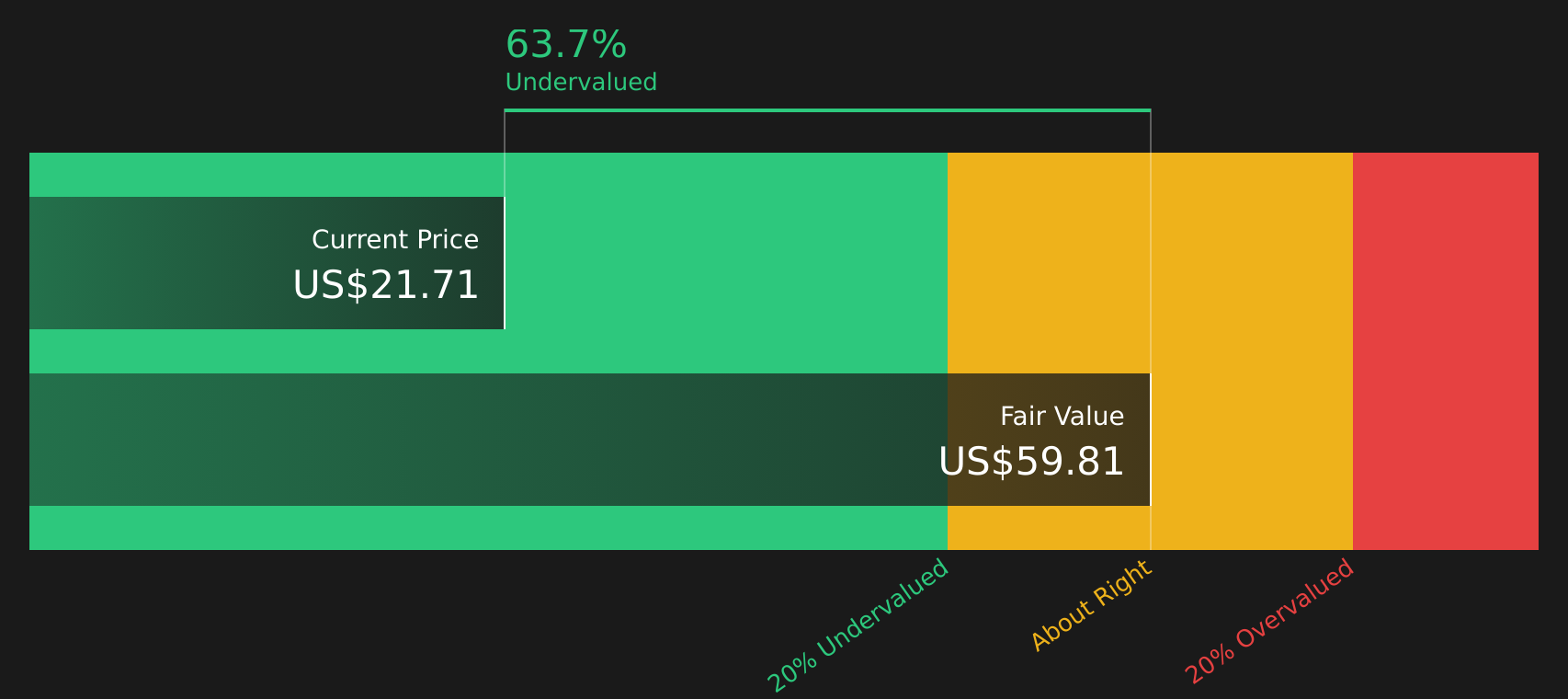

The analyst narrative frames Antero Midstream as about 4.5% overvalued at a fair value of $21.57, based on future earnings and multiples. Our DCF model, using future cash flows instead of earnings multiples, points to a value of $59.05, which is a large gap for you to reconcile.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Antero Midstream for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 63 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value, risk, and reward, does the story so far really tell you enough? Take a closer look at the underlying data, consider the trade off between potential upside and the concerns highlighted, and see the full picture with 3 key rewards and 2 important warning signs

Ready to uncover more ideas?

If Antero Midstream has you thinking harder about where to put fresh capital, do not stop here. Broaden your watchlist with focused sets of stocks that match clear, practical themes.

- Target quality at a discount by scanning companies filtered as 63 high quality undervalued stocks, so you are not relying on hunches when comparing price against fundamentals.

- Prioritize staying power with the solid balance sheet and fundamentals stocks screener (39 results), and focus on businesses that pair financial resilience with straightforward, transparent balance sheets.

- Get ahead of the crowd by hunting through the screener containing 25 high quality undiscovered gems, where smaller names with strong fundamentals may not yet be widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English