How Carnival’s Q1 Profit Return And New Buybacks At Carnival Corporation (CCL) Has Changed Its Investment Story

- Carnival Corporation & plc recently reported first-quarter 2026 results, with sales of US$2,142 million, revenue of US$6,165 million, and net income of US$258 million, and also announced a US$2.50 billion open-ended share repurchase program authorized by its Board of Directors on March 27, 2026.

- The shift from a net loss to positive earnings, alongside committing billions to buybacks, signals management’s confidence in the company’s financial position and future cash generation capacity.

- Next, we’ll examine how Carnival’s move to initiate a multi-billion-dollar share repurchase program could reshape its investment narrative and risk profile.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Carnival Corporation & Investment Narrative Recap

To own Carnival today, you have to believe that demand for cruising and high-margin private destinations can offset rising costs and geopolitical noise, while the company steadily chips away at its debt load. The latest quarter’s move back into positive earnings is helpful, but near term the key catalyst remains execution on pricing and bookings, while the biggest risk is still external cost pressure, particularly fuel, which this news does not fundamentally change.

The most relevant update here is the new US$2.50 billion open-ended share repurchase program. Coming alongside a return to quarterly profits, it sits on top of earlier balance sheet work and dividend reinstatement, and could meaningfully influence how much of Carnival’s future cash flow ends up in shareholders’ hands versus creditors, especially if earnings and free cash generation stay on track with its Propel and loyalty program initiatives.

But against that, investors should be aware that fuel cost volatility and geopolitical shocks could still materially affect...

Read the full narrative on Carnival Corporation & (it's free!)

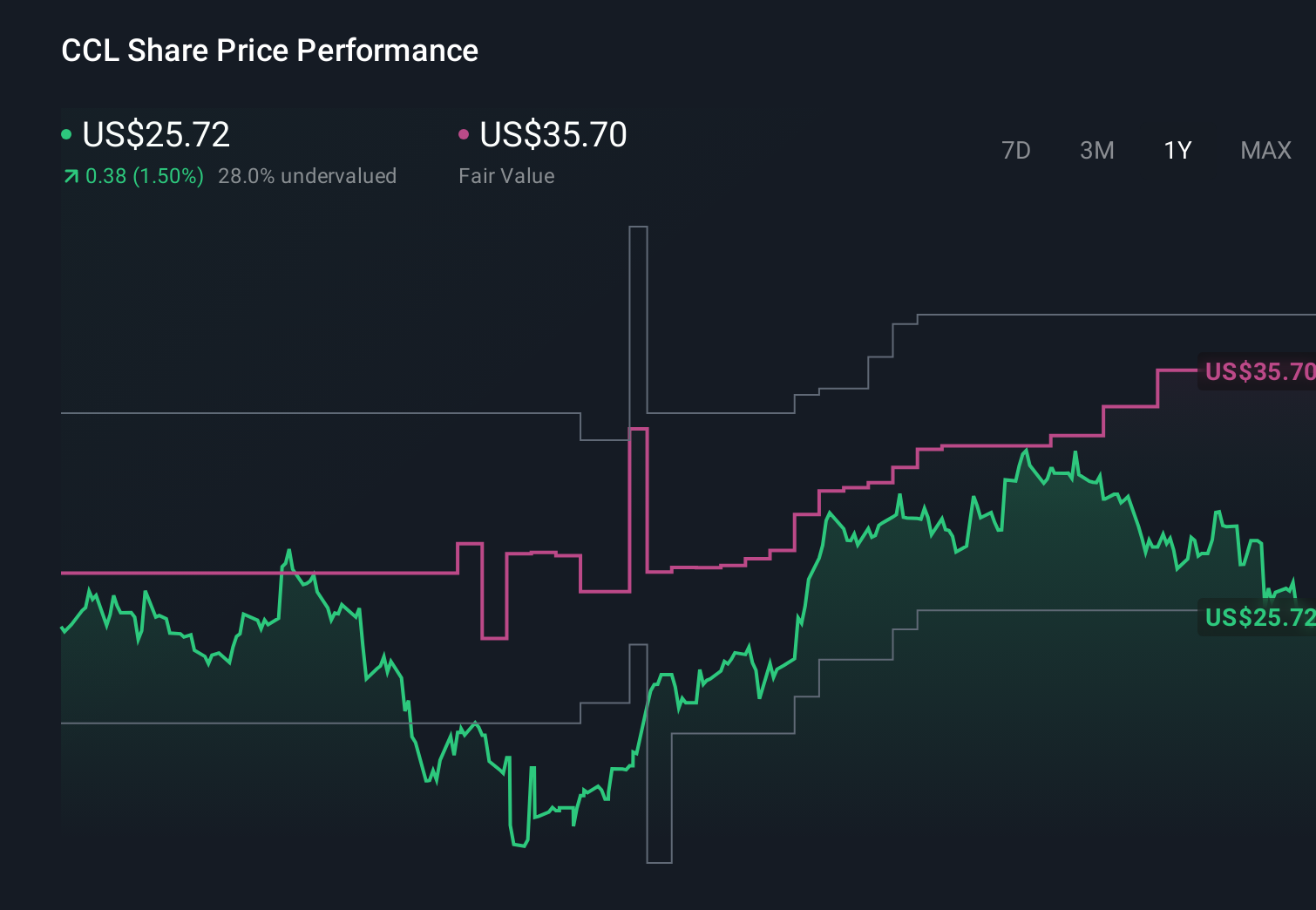

Carnival Corporation &'s narrative projects $29.0 billion revenue and $3.7 billion earnings by 2028. This requires 3.8% yearly revenue growth and a roughly $1.2 billion earnings increase from $2.5 billion today.

Uncover how Carnival Corporation &'s forecasts yield a $37.70 fair value, a 42% upside to its current price.

Exploring Other Perspectives

Some of the most pessimistic analysts, who were penciling in earnings of about US$3.6 billion on roughly US$28.3 billion of revenue by 2028, worry that aging ships and heavier climate regulation could eat into the kind of profitability implied by Carnival’s strong Q1 and fresh US$2.50 billion buyback, so it is worth weighing their caution alongside more optimistic views before deciding what you believe.

Explore 13 other fair value estimates on Carnival Corporation & - why the stock might be worth as much as 94% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Carnival Corporation & research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Carnival Corporation & research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carnival Corporation &'s overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 25 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Invest in the nuclear renaissance through our list of 94 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English