A Look At Trinity Capital’s Valuation As Joint Venture And Insider Buying Follow Mixed Earnings

Why Trinity Capital’s new joint venture is drawing investor attention

Trinity Capital (TRIN) has moved into focus after forming a US$100 million joint venture with Capital Southwest Corporation to target senior secured debt, alongside a sizeable insider share purchase by Steven Brown.

See our latest analysis for Trinity Capital.

The joint venture and insider buying sit against a share price that closed at US$14.79, with a modest 7 day share price return of 1.09% but a stronger 1 year total shareholder return of 9.24%, hinting that longer term momentum has outpaced recent price moves.

If this kind of targeted credit exposure interests you, it could be a good moment to widen your search and check out 20 top founder-led companies

With Trinity trading at US$14.79 and flagged as having an intrinsic discount plus room to analysts’ price targets, the real question is whether investors are seeing a genuine value gap or whether the market already prices in future growth.

Preferred P/E of 9.1x: Is it justified?

On a P/E of 9.1x and a last close of $14.79, Trinity Capital screens as expensive against its direct peers but cheaper than the broader US Capital Markets group.

The P/E multiple shows what investors are currently willing to pay for each dollar of earnings, which matters a lot for a lender focused on cash generation and shareholder distributions. For Trinity, a 9.1x P/E sits above the peer average of 6.2x, which points to investors assigning a higher earnings valuation than similar names. At the same time, it sits below the estimated fair P/E of 11.3x, a level that the market could potentially move toward if current assumptions play out.

Against the wider US Capital Markets industry average of 33.1x, Trinity’s 9.1x P/E looks much lower, which shows how differently the market is pricing its earnings compared with the sector. The tension between a higher multiple than close peers and a lower multiple than the industry, as well as a discount to the fair P/E estimate, is what many investors are now weighing up.

Explore the SWS fair ratio for Trinity Capital

Result: Price-to-earnings of 9.1x (ABOUT RIGHT)

However, investors still need to watch for credit quality issues in Trinity’s growth stage portfolio and any shift in the assumptions behind its US$16.61 analyst price target.

Find out about the key risks to this Trinity Capital narrative.

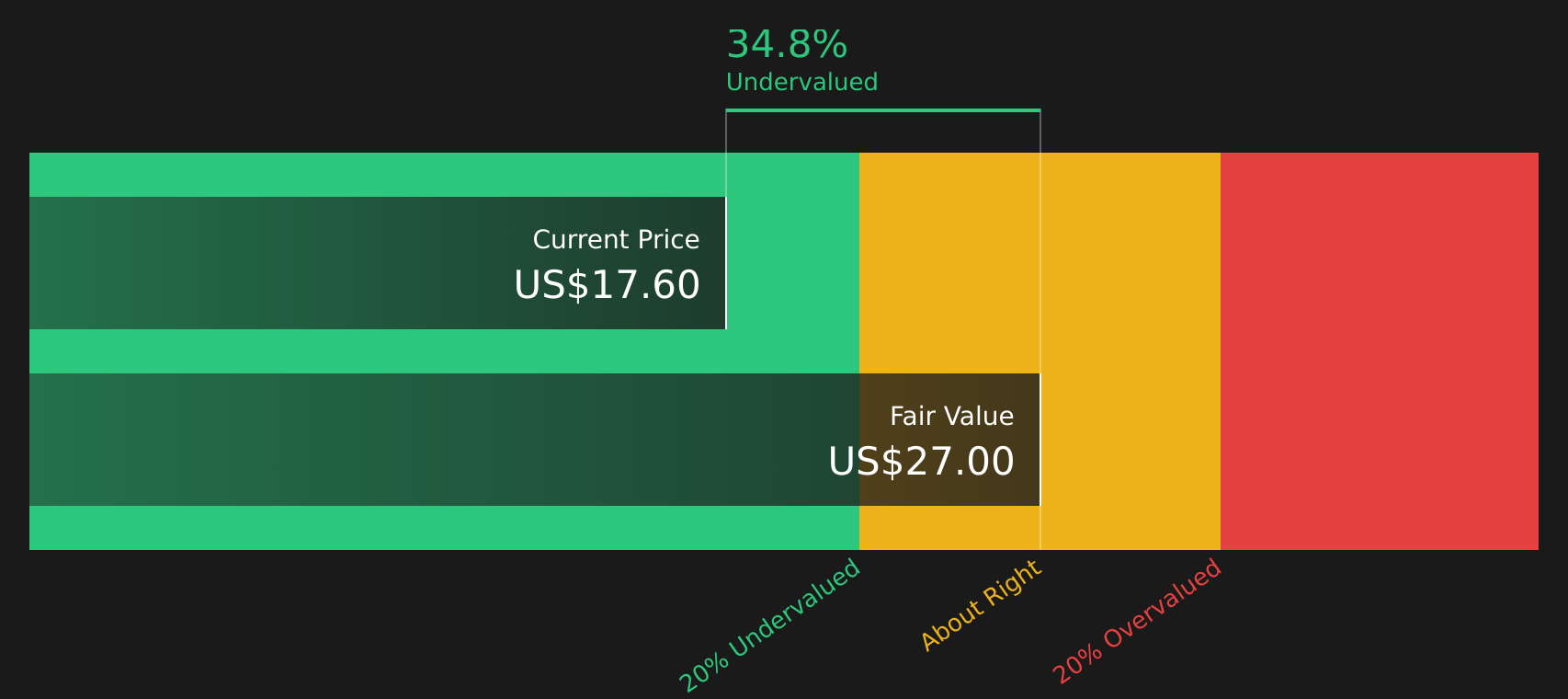

Another view: DCF points to a different story

While the 9.1x P/E suggests Trinity is roughly in line with where earnings ratios might settle, the SWS DCF model paints a different picture. With the share price at $14.79 versus an estimated future cash flow value of $19.22, the model flags the stock as undervalued. This raises a clear question: are current earnings multiples missing part of the cash flow story?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Trinity Capital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 63 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals from valuation and sentiment, the real edge comes from understanding the details for yourself and acting before the crowd fully reacts. To get a balanced view of both sides of the story, check out the 3 key rewards and 4 important warning signs

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one lender. Use focused stock lists to quickly pinpoint other opportunities that fit your style.

- Target potential mispricings by screening for companies that look fundamentally sound yet are priced for caution with the 63 high quality undervalued stocks.

- Strengthen your income stream by focusing on companies offering higher yields with the 12 dividend fortresses.

- Prioritise resilience and sleep easier at night by filtering for companies that score well on stability using the 65 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English