Should Board Exit And Middle East Tensions Reshaping Tanker Markets Require Action From Frontline (FRO) Investors?

- Frontline plc recently confirmed that Director Richard C. Prince resigned from the board, as the company also released its audited 2025 annual report outlining performance and governance developments.

- At the same time, heightened tensions in the Middle East are disrupting key oil shipping lanes, tightening tanker supply and lifting charter rates for operators of Very Large Crude Carriers such as Frontline.

- We’ll now examine how tighter tanker availability amid Middle East tensions could reshape Frontline’s investment narrative and earnings risk-reward profile.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

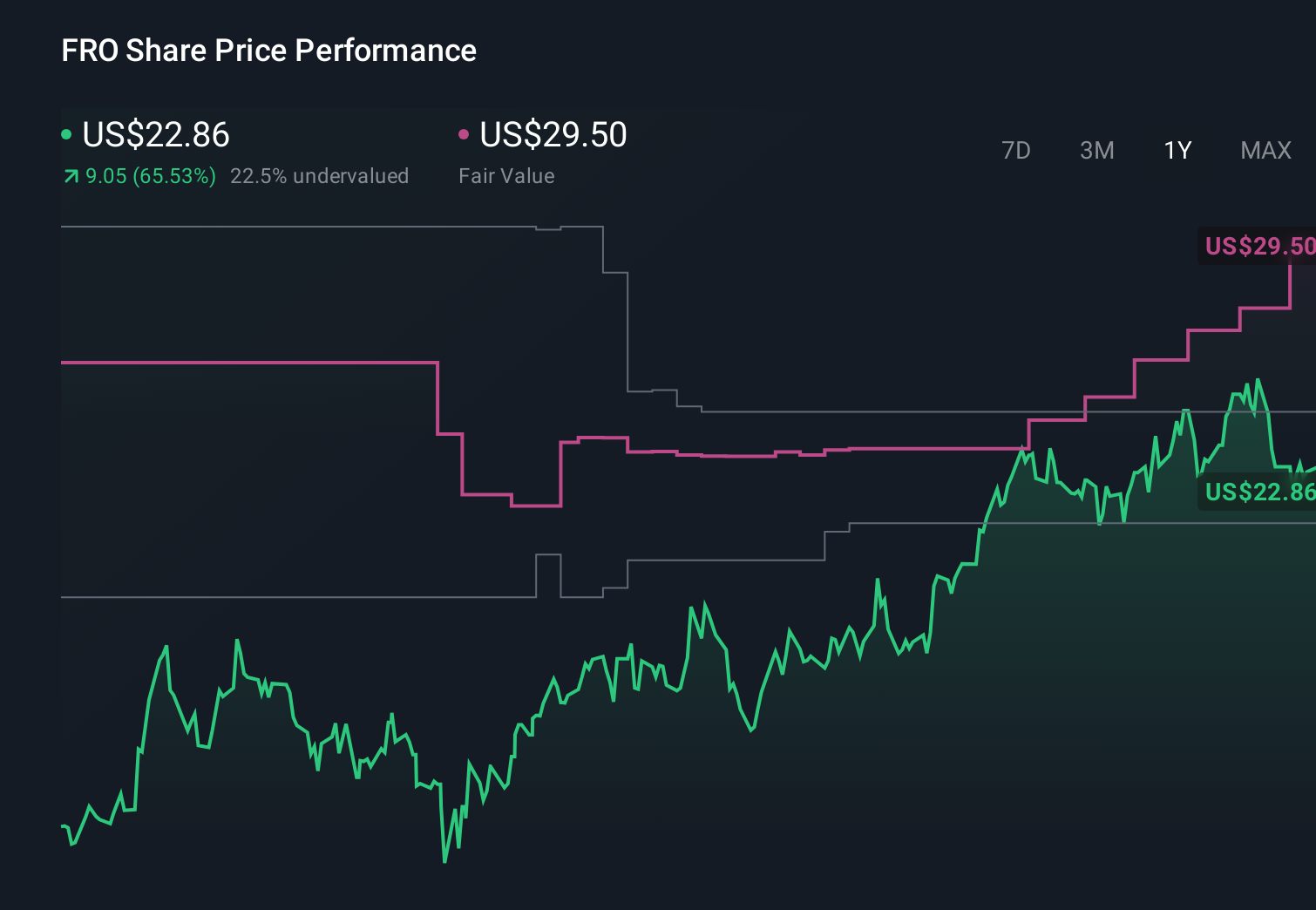

Frontline Investment Narrative Recap

To own Frontline today, you need to believe that tight VLCC supply and firm spot markets can continue to underpin attractive day rates, while the company manages its balance sheet and environmental pressures. The latest Middle East disruptions support the near term rate backdrop, but they do not fundamentally change the biggest current risk, which remains exposure to volatile spot earnings and potential swings in global oil demand and trade flows.

The most relevant recent development here is Frontline’s one year time charter-out of seven VLCCs at about US$76,900 per day, which helps partially lock in cash flows while spot markets react to geopolitical shocks. This move sits alongside the board refresh, including recent director resignations, and forms part of how the company is trying to balance near term earnings visibility with the cyclicality and geopolitical sensitivity that drive its key catalysts.

Yet while higher rates can look attractive today, investors should also be aware of how quickly spot exposure can turn against them if...

Read the full narrative on Frontline (it's free!)

Frontline’s narrative projects $1.6 billion revenue and $697.7 million earnings by 2029. This implies a 7.1% yearly revenue decline and an earnings increase of about $318.6 million from $379.1 million today.

Uncover how Frontline's forecasts yield a $41.25 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming revenue near US$1.6 billion and earnings around US$686.0 million by 2028, highlighting a much more cautious view than the consensus. If you compare those assumptions with the heightened Middle East tensions and the risk of disrupted trade routes increasing costs and complexity, you can see how opinions about Frontline’s outlook can differ sharply and why it is worth exploring these alternative views for yourself.

Explore 5 other fair value estimates on Frontline - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Frontline research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Frontline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontline's overall financial health at a glance.

Ready For A Different Approach?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English