Is Tripadvisor (TRIP) Share Price Weakness Creating A Potential Opportunity For Investors?

- If you are wondering whether Tripadvisor is a bargain at its current share price or cheap for a reason, this article breaks down what the market might be implying about its value.

- The stock last closed at US$10.71, with a 12.6% return over the past week and 7.3% over the past month, but a 26.8% decline year to date and a 25.2% decline over the past year.

- Recent headlines around Tripadvisor have focused on ongoing competition among travel platforms and how consumer behavior is evolving as more trips are researched and booked online. These themes help frame why the share price has been volatile over shorter periods while longer term returns have been weaker.

- On Simply Wall St's valuation checks, Tripadvisor currently has a valuation score of 2 out of 6. This sets up a closer look at how different valuation methods treat the stock today and points to an even broader way of thinking about value at the end of this article.

Tripadvisor scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Tripadvisor Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of the cash Tripadvisor could generate in the future and discounts those back into today’s dollars, aiming to show what the business might be worth on a per share basis.

Tripadvisor’s last twelve months Free Cash Flow (FCF) is about $169.9 million. Simply Wall St uses a 2 Stage Free Cash Flow to Equity model, combining analyst forecasts for the earlier years with its own extrapolated estimates further out. In this model, projected FCF reaches $322 million in 2030, with intermediate years such as 2026 to 2029 ranging from about $241.6 million to $292 million, all in $ terms.

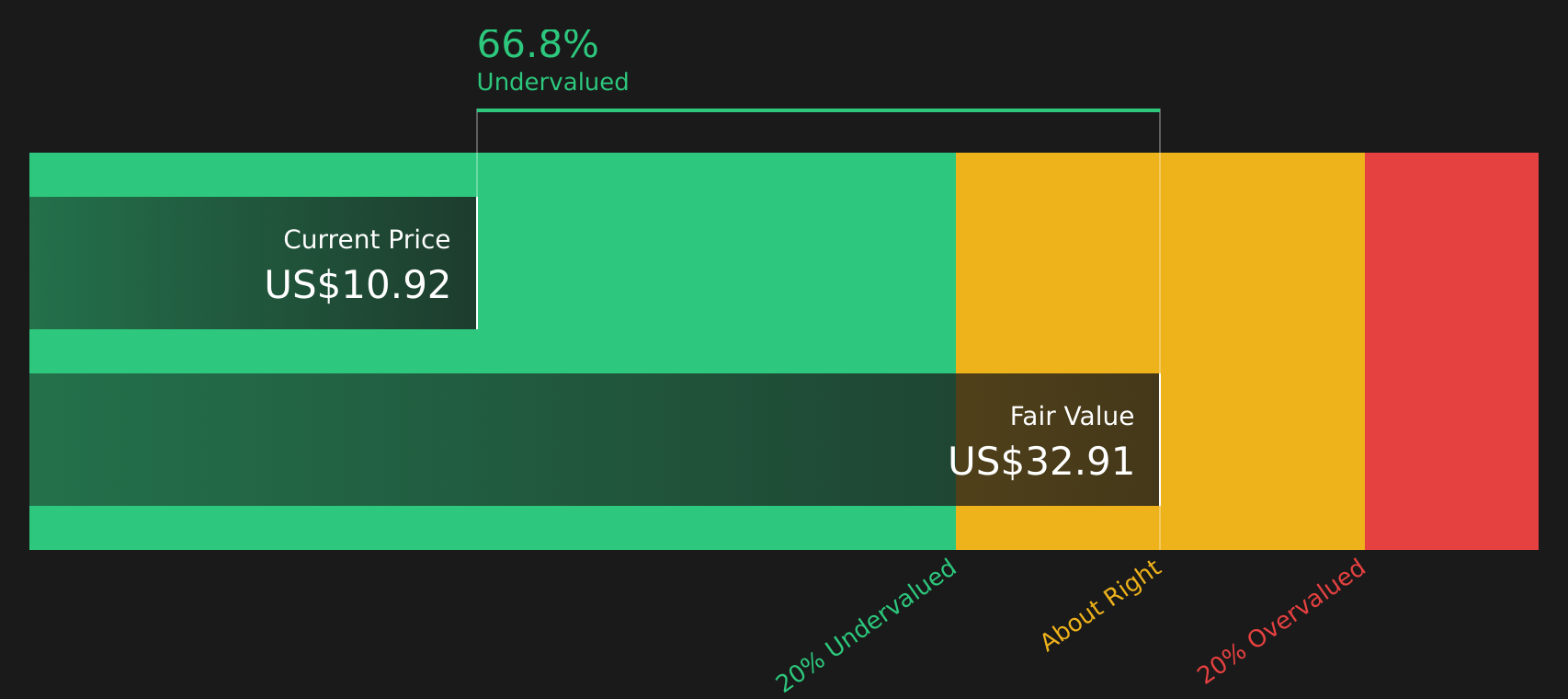

Pulling those projections together and discounting them back, the DCF model arrives at an estimated intrinsic value of about $33.17 per share, compared with the recent share price of US$10.71. That implies the shares trade at a 67.7% discount to this DCF estimate, which indicates the stock may be materially undervalued on this set of cash flow assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Tripadvisor is undervalued by 67.7%. Track this in your watchlist or portfolio, or discover 63 more high quality undervalued stocks.

Approach 2: Tripadvisor Price vs Earnings

For profitable companies, the P/E ratio is a common way to think about value because it links what you pay for each share to the earnings that support that share. A higher or lower P/E can make sense depending on what the market expects for future growth and how much risk investors see in the business and its industry.

Tripadvisor currently trades on a P/E of 30.73x. That compares with an Interactive Media and Services industry average P/E of 14.04x and a peer group average of 17.98x, so the stock is priced above both of those benchmarks. Simply Wall St also calculates a Fair Ratio of 23.22x, which is the P/E that might be expected given factors such as Tripadvisor’s earnings growth profile, industry, profit margins, size and risk characteristics.

This Fair Ratio is more tailored than a simple comparison with peers or the industry, because it adjusts for Tripadvisor’s own fundamentals instead of assuming all companies deserve the same multiple. With the current P/E of 30.73x sitting above the Fair Ratio of 23.22x, this approach points to the shares looking relatively expensive on earnings.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Tripadvisor Narrative

Earlier it was mentioned that there is an even better way to think about value. Narratives on Simply Wall St give you a simple story behind your numbers, connecting your view of Tripadvisor’s future revenue, earnings and margins to a specific forecast and Fair Value that you can compare with today’s share price.

Each Narrative on the Community page is a clear, shareable storyline that ties what you believe about the business to a full financial model. Instead of only looking at a P/E of 30.73x or a single analyst target, you see the logic that leads to a Fair Value.

For Tripadvisor, one investor might align with a cautious Narrative that ties a Fair Value of US$8.50 to modest revenue growth, slimmer margins and a higher discount rate, while another might choose a more optimistic Narrative with a Fair Value of about US$24.10 that assumes faster growth, higher margins and strong earnings power.

As new news or earnings arrive, these Narratives update automatically so you can quickly see how Fair Value shifts relative to the current price and decide whether the story you believe in still matches where Tripadvisor trades today.

For Tripadvisor, however, we will make it really easy for you with previews of two leading Tripadvisor Narratives:

Start with the optimistic case if you think Tripadvisor can compound value from here.

Fair value in this Narrative: US$14.38 per share.

Gap to this fair value vs the last close of US$10.71: about 25.5% below the narrative fair value.

Revenue growth assumption: 4.53% a year.

- Analysts in this camp link value to growth in experiential travel, with Viator and TheFork expanding Tripadvisor's reach and supporting the earnings model.

- They see AI tools, personalization and rewards programs helping shift users toward the app and higher value, repeat behavior over time.

- Portfolio simplification, recurring style B2B revenue and a long running global brand are treated as positives for cash flow resilience.

Then weigh that against a more cautious view that focuses on structural pressure and competition.

Fair value in this Narrative: US$8.50 per share.

Gap to this fair value vs the last close of US$10.71: about 26.0% above the narrative fair value.

Revenue growth assumption: 1.56% a year.

- This view puts more weight on traffic and market share risks as users spend more time in walled gardens, direct booking channels and larger travel platforms.

- It also factors in higher compliance and data privacy costs that could limit how effectively Tripadvisor monetizes its audience.

- Under this Narrative, Tripadvisor still generates earnings and free cash flow, but the multiple and growth inputs are tempered by these competitive and regulatory headwinds.

Both Narratives use explicit assumptions about revenue, margins, required returns and fair value. Your next step is to decide which set of inputs feels closer to the Tripadvisor story you believe in, and whether the current price gives you enough upside or downside protection for that view.

Do you think there's more to the story for Tripadvisor? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English