Boeing Has Experienced a Rash of Safety Issues. Can the Company Reassure Investors That the Stock Is a Buy in 2026?

Key Points

Boeing faces ongoing safety and certification challenges affecting production and margins.

Recent management changes and integration efforts have led to operational improvements.

Profitability in the key commercial airplanes segment is delayed, with cautious optimism for 2026-2027.

Perhaps the question in the title should be subtly different. It's not just safety issues per se; it's also the cost of fixing them and ensuring that more issues don't crop up again that Boeing (NYSE: BA) needs to convince investors on. The latest updates on the matter have proven mixed, but is the 18% sell-off since the last earnings report now making the stock a good value?

Boeing's safety issues

A combination of safety issues, including high-profile 737 MAX crashes and consequent groundings, and a production cap imposed by the Federal Aviation Administration (FAA) after a blowout on an Alaska Airlines flight, has caused investors to express concern about Boeing's safety record. Moreover, the costs of dealing with their consequences, including groundings, production delays, certification delays, and potentially lost orders, have led to significant cash burn at the company in recent years.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Boeing.

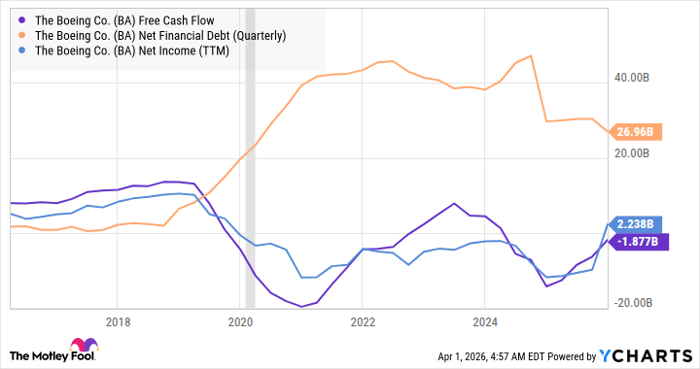

Throw in the travel lockdowns imposed on the populace during COVID-19's height, and Boeing has had a rough time in recent years, with debt ballooning and income and cash flow deteriorating.

BA Free Cash Flow data by YCharts.

Boeing's latest updates are mixed

The good news is that new CEO Kelly Ortberg has stabilized the business. Boeing is now producing 737 MAX aircraft at a rate of 42 a month and expects to ramp to 47 a month by midyear. Moreover, Boeing is on track to open a new 737 MAX production line in its Everett facility (in addition to production lines in Renton) to help it ramp production further.

CFO Jesus Malave recently confirmed that 737 MAXs would begin production at Everett in the summer during the recent Bank of America Global Industrials conference.

However, investors also need to consider several negatives related to safety, FAA inspections, and quality control:

- Malave said that the Spirit acquisition put pressure on its commercial airplanes (BCA) segment margins, and the return to positive margins will be "pushed out a year to about until 2027. This year will be negative. And in fact, in this quarter, will be negative around 7.5%, 8%."

- Boeing had to reset schedules on the 737 MAX-7 and 737 MAX-10 variants, as well as the new widebody 777X, due to pushouts in expected certification to 2026 (for the 737-7 and 737-10) and 2027 (for the 777X). Malave confirmed that management still expects these adjusted certification expectation dates to hold.

- Boeing had a brief pause in 737 MAX production in the first quarter, which would cause 10 of the expected 120 deliveries to slip into the second quarter.

- Deliveries on the widebody 787 would be "lighter" than the expected 20 due to seating certification issues, but "we continue to expect that we'll deliver 90 to 100 aircraft this year," according to Malave.

What it means for Boeing investors

The delayed return to profit at BCA due to integrating Spirit, the previous certification pushouts on the 777X and 737 MAX variants, and the need to play catch-up on 737 MAX and 787 production in 2026 all speak to the ongoing pressure at Boeing to deliver.

Boeing is dealing with its quality control issues. But investors will want to see the 737 MAX variant certifications in 2026, and the company catch up with the production schedule on the 737 MAX and 787, before feeling fully confident buying in here. Until then, the stock likely remains a cautious buy.

Bank of America is an advertising partner of Motley Fool Money. Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Boeing. The Motley Fool recommends Alaska Air Group. The Motley Fool has a disclosure policy.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English