A Look At Northrop Grumman (NOC) Valuation After A Recent Share Price Pullback

Northrop Grumman Stock Snapshot

Northrop Grumman (NOC) is drawing attention after recent share performance, with a last close of $702.50 and mixed returns over different periods, including a roughly 7% decline over the past month.

See our latest analysis for Northrop Grumman.

The recent pullback, with a 30 day share price return of around negative 7%, comes after strong momentum earlier in the year. This includes a 90 day share price return of almost 20% and a 1 year total shareholder return of about 39%, which suggests sentiment has cooled but longer term holders have still seen solid gains.

If you are looking beyond defense to see where capital is flowing next, this could be a good moment to size up 28 power grid technology and infrastructure stocks

With Northrop Grumman now at $702.50 after a recent 7% pullback but strong multi year returns, the key question is simple: is the stock now underpriced, or has the market already baked in future growth?

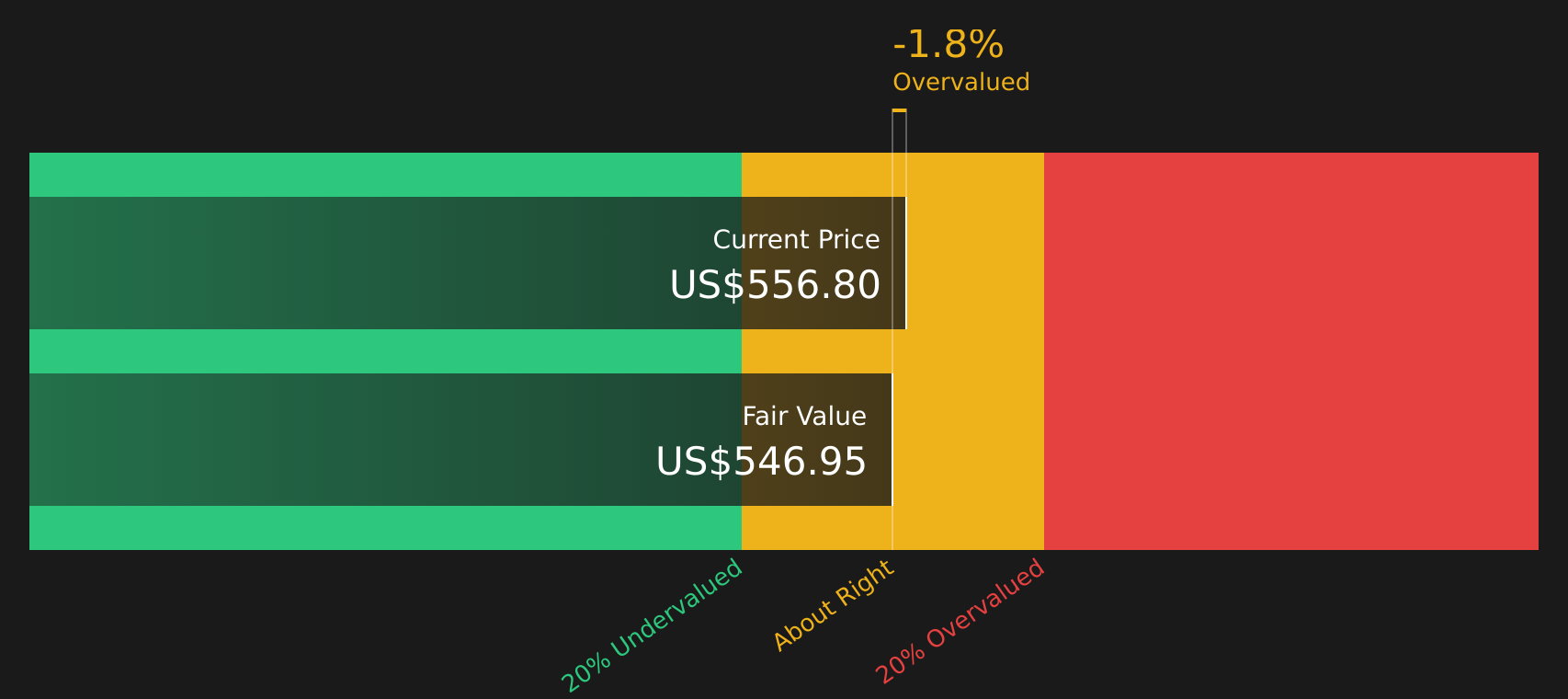

Most Popular Narrative: 3.2% Undervalued

Northrop Grumman’s most followed narrative points to a fair value of about $725.72, slightly above the last close at $702.50, which frames the current pullback as relatively modest against that model.

The ramp-up of advanced autonomous and integrated systems such as Beacon and IBCS, combined with ongoing investments in solid rocket motor capacity (targeting a near-doubling by 2029), positions the company to capitalize on high-growth, higher-margin market segments, thereby enhancing future operating margins and underlying cash flow.

Curious how this growth push translates into that fair value number? The narrative leans on steady revenue expansion, slightly slimmer margins, and a higher future earnings multiple. The mix of these assumptions is what really drives the $725.72 figure.

Result: Fair Value of $725.72 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the whole story can change quickly if major U.S. contracts face budget cuts or if cost overruns on big programs begin to squeeze margins.

Find out about the key risks to this Northrop Grumman narrative.

Another View: DCF Sends a Different Signal

There is a catch. While the analyst narrative and fair value estimate of $725.72 frame Northrop Grumman as about 3.2% undervalued, the SWS DCF model points the other way, with an estimated future cash flow value of $516.25, which would put the current $702.50 share price above that mark.

That gap between earnings based fair value and the cash flow driven DCF view raises a simple question for you as an investor: which set of assumptions about growth, margins and required returns feels more realistic over the long haul, and how much valuation risk are you comfortable taking on if the DCF view proves closer to reality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Northrop Grumman for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 62 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment split between modest undervaluation, a lower DCF value and a mix of risks and rewards, you may want to review the numbers yourself and decide where you stand. You can then weigh up the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Northrop Grumman is already on your radar, do not stop there. The market is full of other opportunities that might fit your style even better.

- Target powerful upside potential with smaller names that still pass strict quality filters by scanning 31 elite penny stocks with strong financials.

- Zero in on companies that blend resilient balance sheets with real earning power by using the solid balance sheet and fundamentals stocks screener (39 results).

- Spot opportunities the crowd might be missing by checking the screener containing 25 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English