A Look At Avista (AVA) Valuation After Governance Proposal To Lower Shareholder Approval Threshold

Avista (AVA) has proposed a governance change, asking shareholders at its AGM to amend its Restated Articles of Incorporation to lower certain approval thresholds from 80% of outstanding shares to a simple majority.

See our latest analysis for Avista.

Avista's share price has been firming, with a 1 day share price return of 1.62%, a 90 day share price return of 6.77%, and a 1 year total shareholder return of 2.50%, suggesting steady but measured momentum around the governance proposal and broader utility operations.

If this governance update has you thinking about other regulated power names, it could be a good moment to scan 28 power grid technology and infrastructure stocks

With Avista trading at US$41.34, close to its analyst price target and with only modest total returns over 1 and 3 years, the key question is whether the stock still offers value or if the market already prices in expectations for future growth.

Most Popular Narrative: 2.5% Overvalued

The most followed narrative pegs Avista's fair value at $40.33, slightly below the last close at $41.34, which suggests a modest premium in the current price and puts more focus on the assumptions behind its long term cash flows.

Robust, multi year capital investment plans approaching $3 billion (2025 to 2029), with additional upside from grid expansion projects and new generation needs tied to large load requests, position Avista to earn regulated returns and drive long term earnings expansion. Approval of favorable, all party rate settlements in Oregon and Idaho, alongside established constructive regulatory outcomes in Washington, increases predictability and supports improved future net margins and stable earnings through rate recovery.

Curious what sits behind that valuation gap? The narrative leans heavily on measured revenue growth, firmer margins, and a future earnings multiple that assumes steady utility style expansion.

Result: Fair Value of $40.33 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still meaningful risk that higher wildfire, grid modernization, and clean tech investment costs, if not fully recovered in rates, could pressure margins and future cash generation.

Find out about the key risks to this Avista narrative.

Another Angle On Value

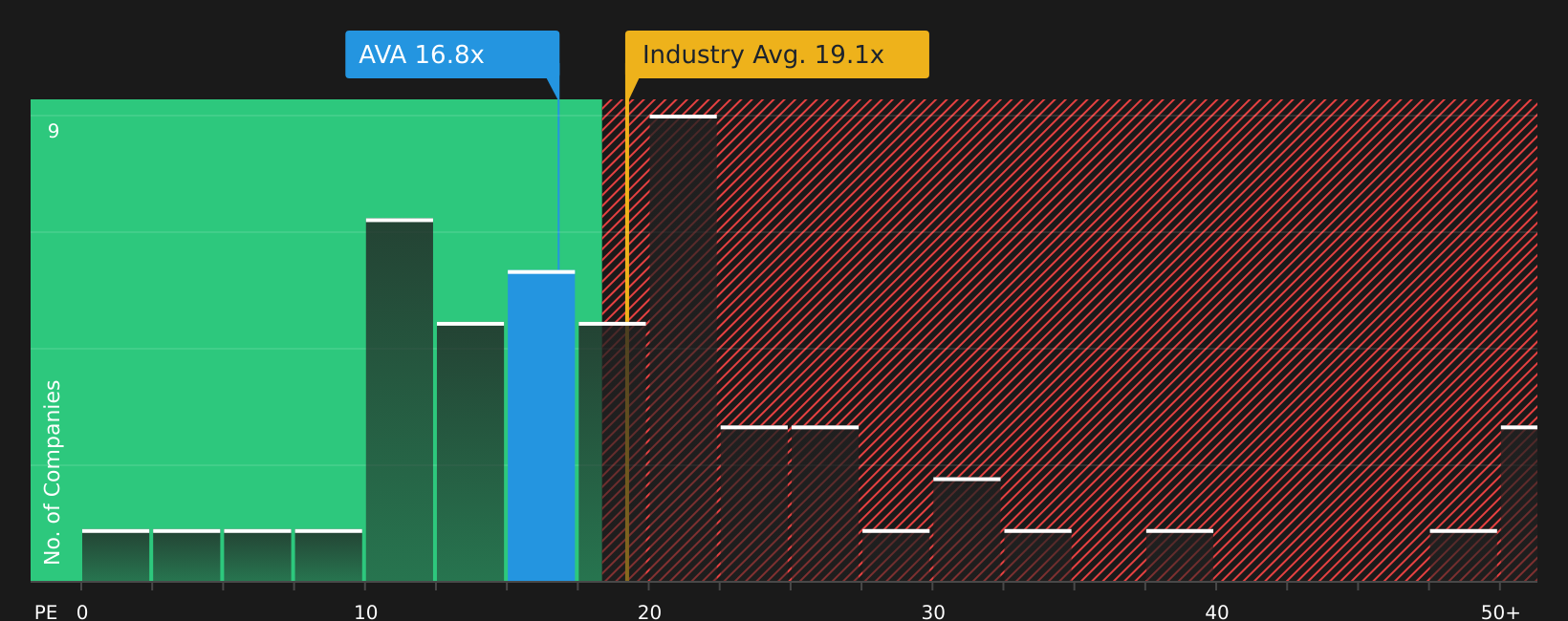

While the SWS DCF model flags Avista as overvalued at $41.34 versus an estimated future cash flow value of $36.73, the P/E view tells a different story. A P/E of 17.6x sits below peers at 25.3x, below the global industry at 19x, and below the 18.5x fair ratio. Which signal would you put more weight on?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Overall, the story here combines cautious optimism with clear watch points. It makes sense to review the full picture and decide quickly where you stand by weighing up the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

Do not stop your research with just one utility name. Widen your view with a few focused stock ideas that could sharpen your next move.

- Target quality at a discount by scanning 62 high quality undervalued stocks that pair solid fundamentals with prices that sit below many investors' radars.

- Focus on resilience and capital protection by reviewing 67 resilient stocks with low risk scores that score well on financial strength and business risk.

- Spot potential future standouts early by using the screener containing 25 high quality undiscovered gems before attention and capital crowd into the same familiar names.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English