A Look At New Oriental Education & Technology Group (EDU) Valuation After Recent Share Price Moves

Why New Oriental Education & Technology Group (EDU) is on investor radars

New Oriental Education & Technology Group (EDU) has drawn attention after recent share price moves, with the stock closing at US$56.42 and showing mixed returns over the past year and the past 3 months.

For readers tracking performance, the company shows a 1 day return of a 0.8% decline, a 7 day gain of 1.2%, and a month gain of 7.4%, while the past 3 months reflect a 2.4% decline.

See our latest analysis for New Oriental Education & Technology Group.

At around US$56.42, short term share price momentum has been positive over the past month, while the 1 year total shareholder return of 19.4% points to steadier gains despite some weaker recent quarterly share price returns.

If you are weighing EDU alongside other ideas, it can help to broaden your watchlist and see which companies stand out in our screener of 20 top founder-led companies

So with revenue and net income growth, a US$9.1b market value, and shares trading below some valuation estimates, is EDU still undervalued or is the market already pricing in the group’s future potential?

Most Popular Narrative: 17.4% Undervalued

With New Oriental Education & Technology Group last closing at $56.42 against a narrative fair value of $68.34, the gap between price and projected worth is clear, and the narrative behind that gap leans heavily on earnings power and capital returns.

Aggressive share repurchases and the introduction of a three-year capital return plan committing at least 50% of net income to buybacks and dividends provide a direct and ongoing catalyst for EPS growth and shareholder value creation, especially when combined with rising profitability.

Curious what earnings path and margin profile could justify that higher fair value on a lower future P/E and a 7.8% discount rate? The core of this narrative leans on a specific blend of revenue growth, margin expansion and shrinking share count that does not line up neatly with current pricing, and the full breakdown shows exactly how those moving parts are expected to work together.

Result: Fair Value of $68.34 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on overseas study headwinds easing, and on newer non academic and cultural tourism ventures not dragging on margins or earnings for longer than expected.

Find out about the key risks to this New Oriental Education & Technology Group narrative.

Another way to look at EDU’s valuation

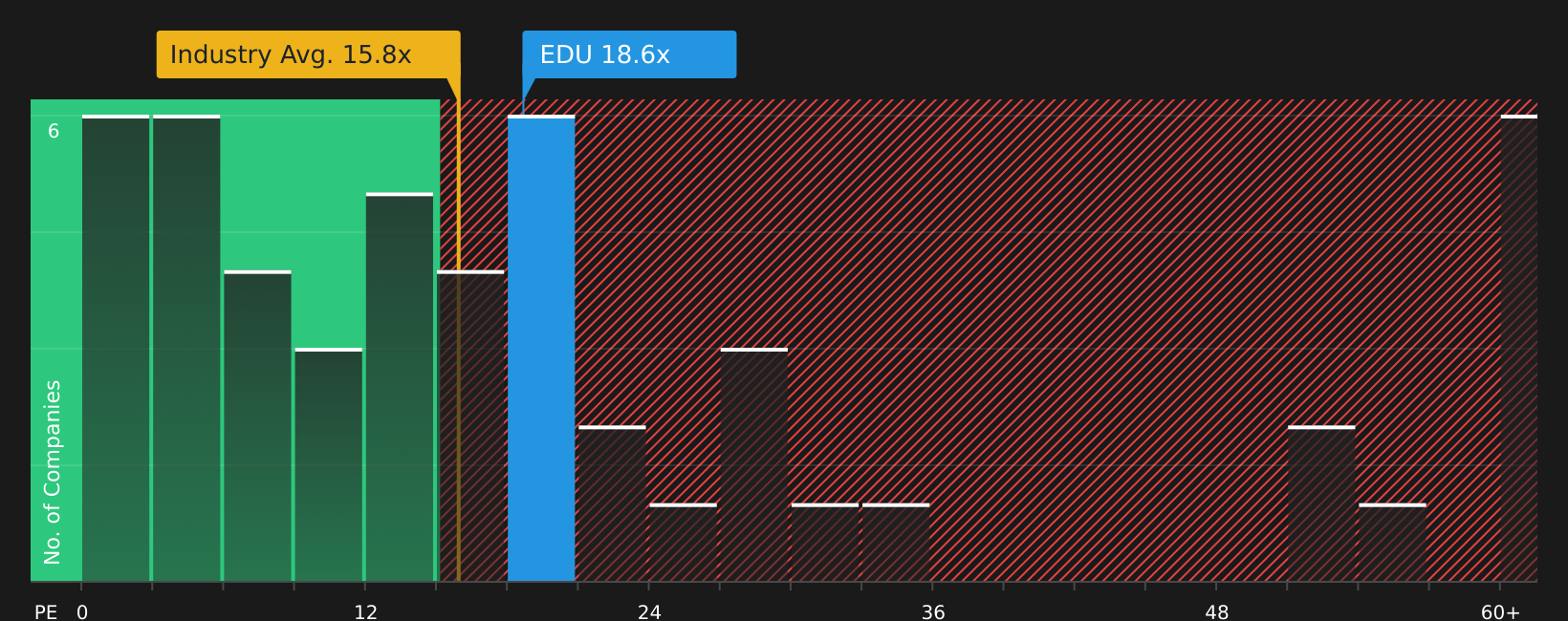

The earlier narrative leans on discounted future cash flows to argue EDU looks 17.1% below fair value. A simple P/E check tells a different story. EDU trades on 23.6x earnings, which is higher than the US Consumer Services industry at 18.2x and peers at 19.1x, yet below its own fair ratio of 26.7x. That mix suggests some cushion but also less room for error if expectations change. Which signal do you put more weight on?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

The mix of discount and higher P/E might feel conflicted, so it is worth looking at the underlying drivers yourself and weighing the trade offs. To see what investors are currently optimistic about, take a closer look at the 3 key rewards

Looking for more investment ideas?

If EDU is already on your radar, do not stop there. Broaden your opportunity set with other ideas that match your style before the market moves on.

- Target potential mispricing by scanning companies that combine quality with value using our 62 high quality undervalued stocks

- Build a steadier income stream by focusing on companies with robust payouts and yields screened through the 12 dividend fortresses

- Prioritise resilience by zeroing in on businesses that show stronger financial footing with the solid balance sheet and fundamentals stocks screener (39 results)

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English