No Bottom in Sight for the S&P 500: Why Sandisk Stock Has Staged a Major Rally While the Rest of the Index Is Down Bad

The S&P 500 ($SPX) is entering April after a tough first quarter, with the index on course to record its worst Q1 since 2022. However, the stock market did bounce on April 1, largely due to hopes of deescalation in the Middle East. This has lifted sentiment, even if it does not take away from what has been a tough quarter. Therefore, while the stock market may be green today, overall sentiment has remained difficult. But that makes Sandisk (SNDK) one of the most interesting and strongest plays this year.

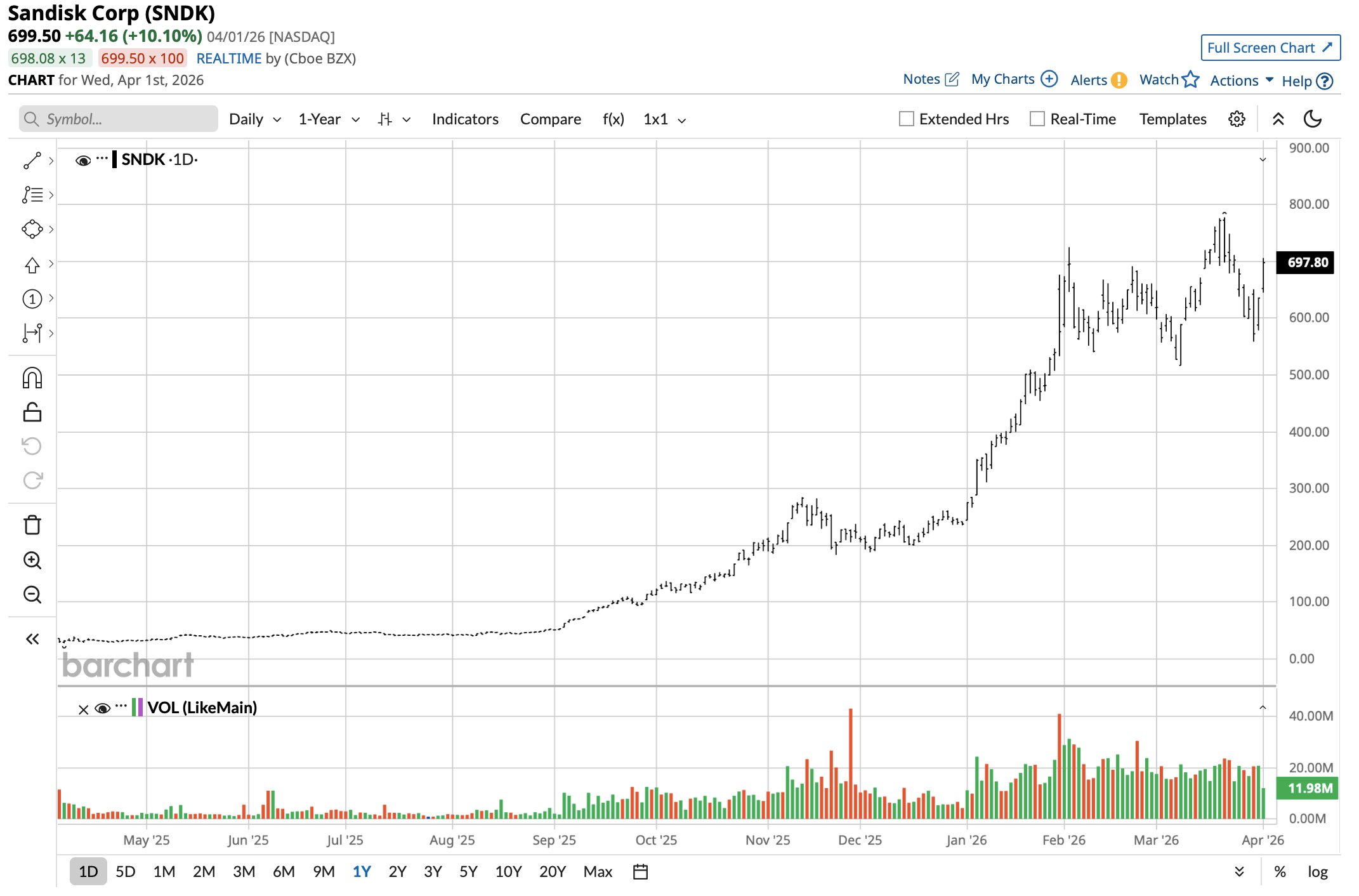

Sandisk has been one of the top-performing stocks in the S&P 500 in 2026 despite the broader market, gaining around 196% year-to-date (YTD) even after a sharp decline from its 52-week high in late March. SNDK stock has not performed like other names in the market, with investors seeing a play in a tech industry segment where prices are likely to improve instead of decline.

About Sandisk

Separated from Western Digital (WDC) in February 2025 and headquartered in Milpitas, California, Sandisk mainly focuses on flash and advanced memory technologies. No longer part of a larger conglomerate, investors are increasingly looking to Sandisk as a pure play on NAND prices, enterprise SSD demand, and AI infrastructure storage.

That kind of pure-play model is a huge part of the appeal. Sandisk currently has a market capitalization of around $103.5 billion. The stock now trades near $701, up more than 2,400% from its 52-week low of $27.89 and only 10% off its 52-week high of $777.60.

But even after such a monster move, the underlying numbers are a bit more complicated.

The trailing price-to-earnings (P/E) ratio is 112.6 times, which is certainly rich, but the forward P/E is closer to 18 times. That is a huge difference. While Sandisk's trailing P/E is certainly high, the forward P/E actually discounts a huge step-up in earnings instead of being a wild multiple based on steady-state earnings. This is a pattern often seen when a cyclical business experiences a huge move into the sweet spot of the business cycle.

Sandisk Beats on Earnings

The recent earnings release is arguably the biggest reason that SNDK stock is still working. For Q2 2026, Sandisk reported revenue of $3.03 billion and non-GAAP EPS of $6.20, beating consensus estimates. Revenue was up 61% year-over-year (YOY), and the company saw significant margin expansion and improved cash flows.

Data-center demand remains an important factor. Data-center revenue was up 64% sequentially during the quarter. Sandisk also provided fiscal Q3 guidance of $4.4 billion to $4.8 billion in revenue and non-GAAP EPS of $12 to $14. This would represent another huge jump in profitability. Overall, Sandisk is benefiting from an extremely favorable pricing and mix environment, likely driven by the AI boom and continued supply discipline in the NAND market.

There is another way to look at this: the market implications. Memory stocks like Sandisk are also rising after Bernstein said the selloff driven by the Alphabet's (GOOGL) TurboQuant algorithm was overdone. This is important because Sandisk is not just moving up due to the latest earnings report — it's moving because the market was getting too bearish, too quickly, on the idea that memory efficiency would somehow destroy demand.

What Do Analysts Expect for Sandisk Stock?

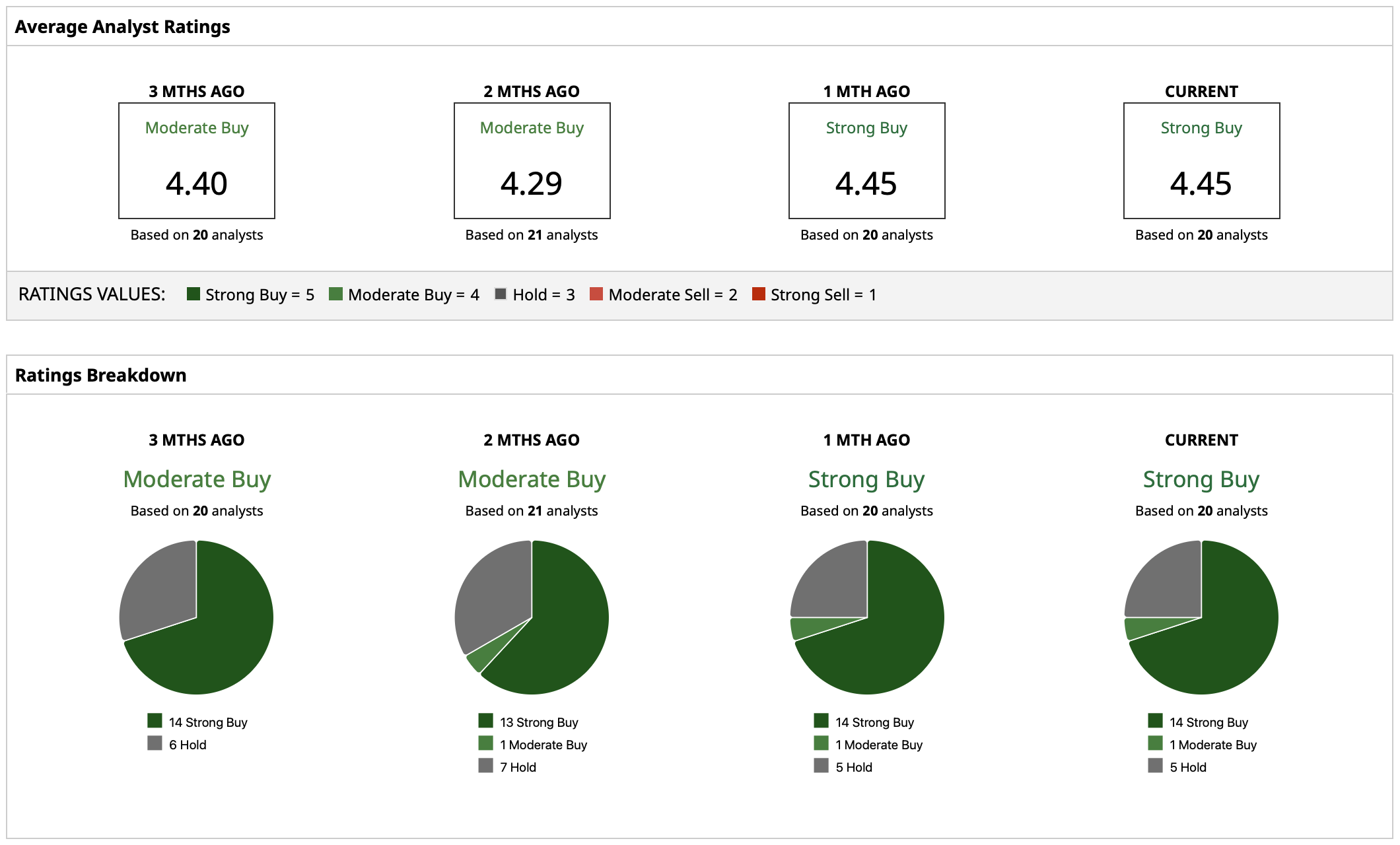

Wall Street still likes SNDK stock, assigning a “Strong Buy” consensus and a rating of 4.45 based on 20 analysts with coverage. Just three months ago, this average was at 4.4, so it has increased somewhat instead of decreasing after the run-up. That's worth paying attention to, since analysts often become more conservative after a huge run-up in a stock.

The mean target price of $752.24 indicates potential upside of 7% from current levels, while the high target price of $1,000 indicates potential upside of 43%. However, the low $450 target reminds investors that SNDK is a memory stock, and memory stocks can still be volatile even when they have great underlying fundamentals.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English