Should Axon Enterprise’s (AXON) Denver Camera Deal Reframe How Investors View Its Public-Safety Data Strategy?

- In late March, the Denver City Council approved a US$150,000, yearlong contract for Axon Enterprise to provide license plate camera technology to the Denver Police Department, replacing a prior system and keeping data control with the city amid an ongoing debate over surveillance rules.

- This deal not only broadens Axon’s footprint in municipal public safety technology, it also places the company at the center of evolving privacy and regulatory discussions that could influence future product adoption.

- We’ll now examine how Axon’s Denver license plate camera contract, set against recent earnings expectations, may influence its overall investment narrative.

Find 59 companies with promising cash flow potential yet trading below their fair value.

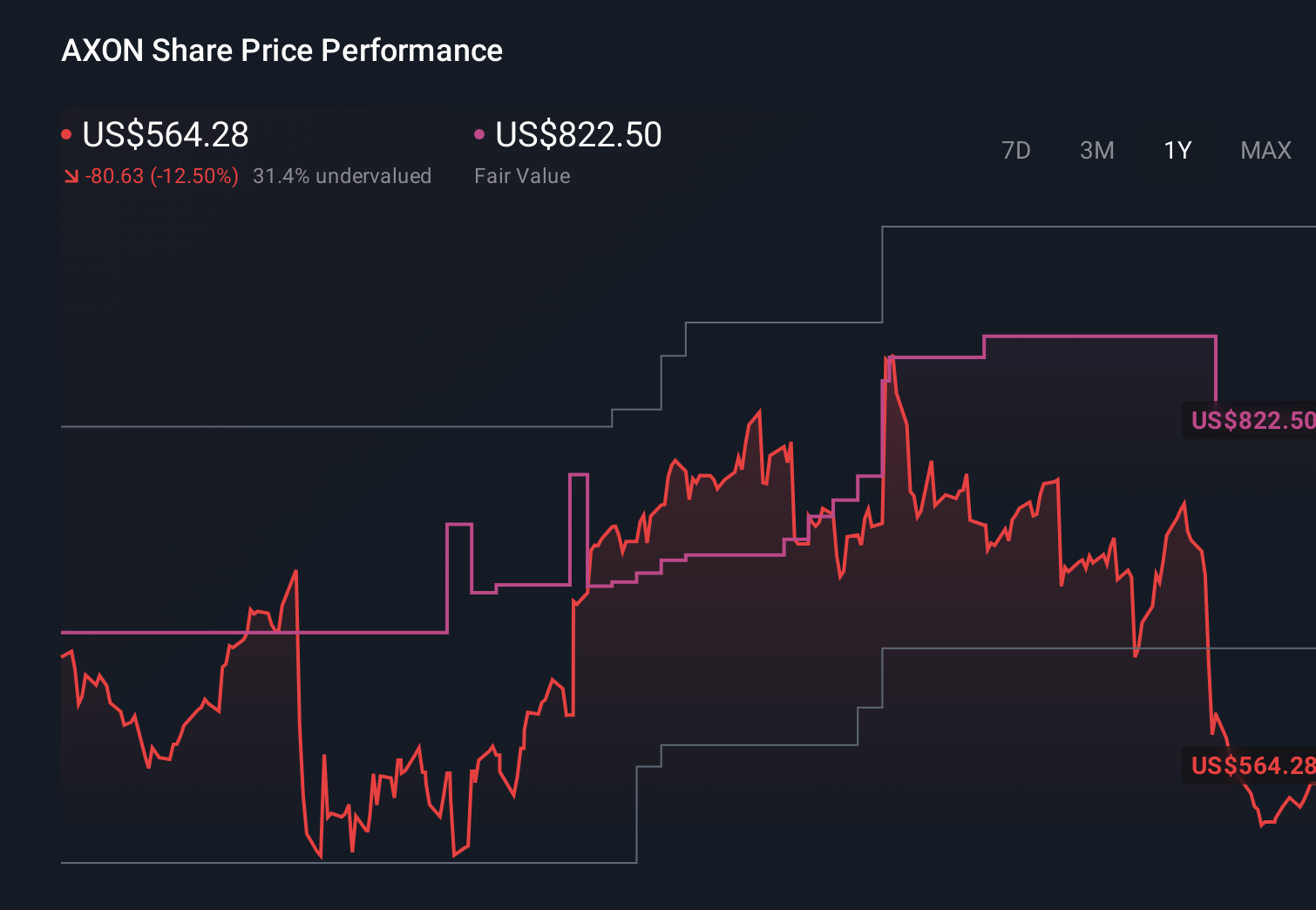

Axon Enterprise Investment Narrative Recap

To own Axon, you need to believe that demand for connected public safety tools can support its premium valuation and earnings growth expectations, despite recent share volatility. The Denver license plate camera contract supports the core thesis of deeper integration with agencies, but at US$150,000 it is not large enough to materially change near term earnings catalysts or meaningfully alter the current key risk around regulatory and privacy pushback.

The most relevant backdrop to Denver’s surveillance debate is Axon’s recent underperformance in the market, even as analysts still expect double digit revenue and earnings growth and assign it a Zacks Rank of #3 (Hold) with a forward P/E above 50. The contract highlights how product adoption is increasingly intertwined with privacy rules at a time when Axon is already under scrutiny for its valuation and dependence on government customers.

But investors should also be aware that growing privacy regulation and public pushback around surveillance could...

Read the full narrative on Axon Enterprise (it's free!)

Axon Enterprise's narrative projects $4.6 billion revenue and $476.0 million earnings by 2028.

Uncover how Axon Enterprise's forecasts yield a $815.00 fair value, a 97% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far more cautious picture, even while assuming revenue could still climb to about US$5.9 billion and earnings to roughly US$460 million by 2029, arguing that regulatory pressures on surveillance tools like Denver’s cameras and stricter data privacy rules could both limit Axon’s AI edge and make those growth targets harder to achieve than the consensus currently implies.

Explore 11 other fair value estimates on Axon Enterprise - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Axon Enterprise research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Axon Enterprise research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Axon Enterprise's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English