A Look At AllianceBernstein (AB) Valuation After Leadership Shift In Business Owner Segment

Leadership shift in business owner segment

AllianceBernstein Holding (AB) is in focus after its private wealth arm expanded Kim Mustin’s role to lead the Business Owner segment nationally, highlighting this client group as a key area of emphasis.

See our latest analysis for AllianceBernstein Holding.

That leadership shift comes as the stock trades at US$38.63, with a 7 day share price return of 8.33% and a 1 year total shareholder return of 16.12%, pointing to firm but measured momentum around the story.

If this kind of targeted growth focus has your attention, it may be a good moment to broaden your search and check out 20 top founder-led companies

With the units trading close to analyst targets and an intrinsic value estimate that sits slightly above the market price, the real question is whether AllianceBernstein still offers upside or if investors are already paying for future growth.

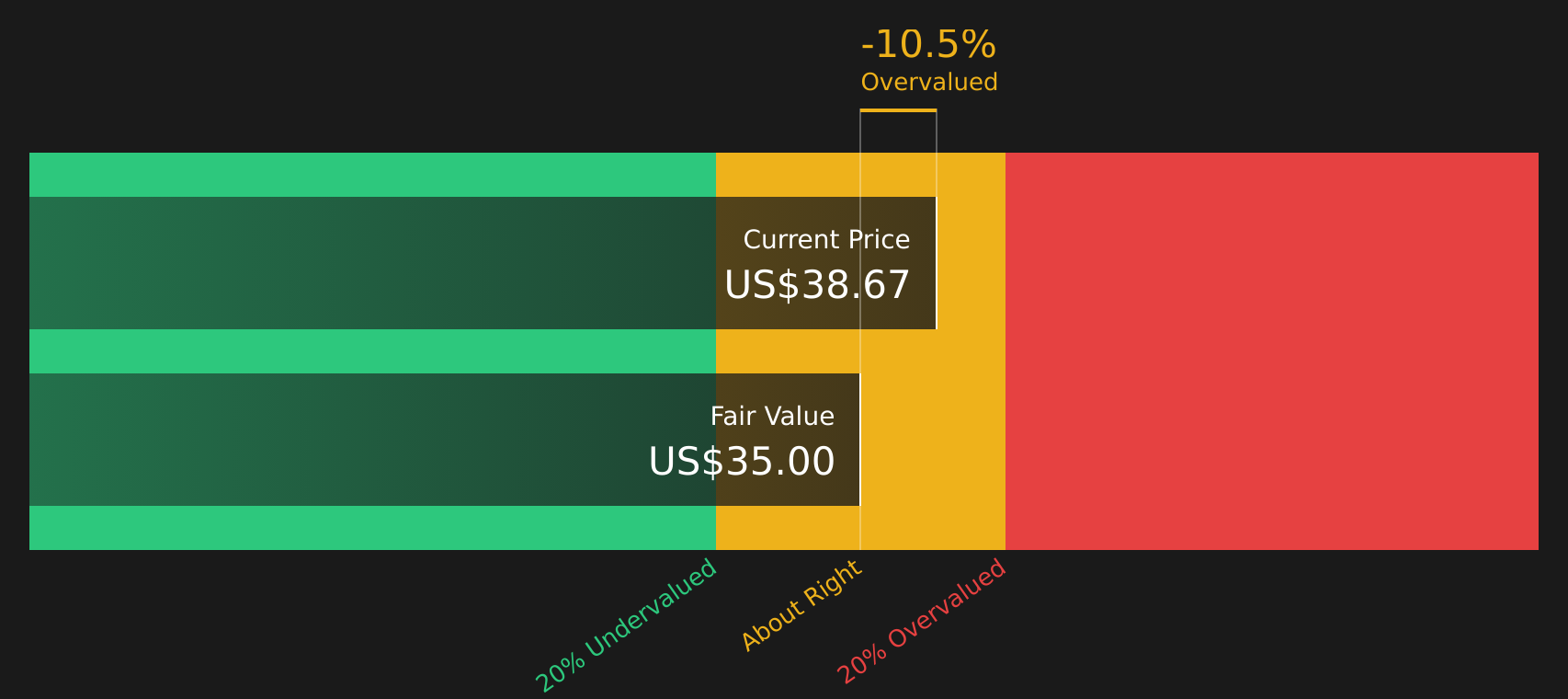

Most Popular Narrative: 3.4% Undervalued

The most followed narrative pegs AllianceBernstein Holding’s fair value at $40, only modestly above the last close at $38.63. This frames the current price as close to that estimate but not stretched.

AllianceBernstein is expanding into high-growth markets such as Asia, U.S. high net worth, and global insurance, supported by its differentiated distribution platform, which is expected to drive revenue growth. The company is enhancing its margin profile by relocating its office and implementing margin accretion initiatives, which are projected to improve net margins as they move into 2025.

Curious what kind of revenue surge and profit margins are baked into that fair value, and how a higher future P/E and buybacks fit into the story.

Result: Fair Value of $40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story could shift quickly if fee pressure intensifies, or if equity outflows and softer alternative flows persist, challenging the current earnings and valuation narrative.

Find out about the key risks to this AllianceBernstein Holding narrative.

Another View: Cash Flow Model Flips The Story

While the popular narrative labels AB as 3.4% undervalued at a fair value of $40, the Simply Wall St DCF model points to a future cash flow value of $35.07, below the current $38.63 price. That leans toward AB looking expensive; which story do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AllianceBernstein Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 59 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed messages in the story so far? If this balance of potential risks and rewards has you on the fence, move quickly, review the details for yourself, and then weigh up the 2 key rewards and 4 important warning signs.

Looking for more investment ideas?

If AB is already on your radar, do not stop there, widening your watchlist now could be the difference between spotting opportunities early or missing them completely.

- Spot potential mispriced quality by scanning 59 high quality undervalued stocks that pair stronger fundamentals with valuations some investors may be overlooking.

- Secure more predictable income by checking 13 dividend fortresses that focus on higher yields backed by supportive financial profiles.

- Prioritise capital preservation by reviewing 68 resilient stocks with low risk scores where business strength and lower risk scores sit at the center of the idea list.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English