A Look At Teekay Tankers (TNK) Valuation As Tanker Rates Hit Multi Decade Highs And 2026 Outlook Brightens

Teekay Tankers (NYSE:TNK) is back in focus as the closure of the Strait of Hormuz lifts spot tanker rates to multi decade highs. Management is also pointing to a potential record first quarter for 2026.

See our latest analysis for Teekay Tankers.

That backdrop of disrupted shipping routes has been reflected in the share price, with Teekay Tankers recording a 48.17% 3 month share price return and a 132.46% 1 year total shareholder return, suggesting momentum has been building rather than fading.

If you are looking beyond tankers for other areas of the market with strong thematic drivers, this is a good moment to scan 28 power grid technology and infrastructure stocks

With the share price already up triple digits over 12 months and trading close to the US$78.40 analyst target, and with revenue and net income growth turning lower, the key question is whether Teekay Tankers is now fully priced or if markets are still underestimating future growth.

Most Popular Narrative: 13.6% Overvalued

At a last close of $76.99 versus a fair value estimate of $67.80, the most widely followed Teekay Tankers narrative points to a premium that rests heavily on how the tanker cycle and fleet renewal story play out over time.

Teekay Tankers' active fleet renewal, recycling proceeds from older vessel sales into newer, more fuel efficient ships, will reduce operational costs and position the company to benefit from tightening environmental regulations, supporting margin improvement and long term earnings growth.

Curious how a shrinking revenue base can still back a premium price tag? The narrative leans on fatter margins, a richer future earnings multiple, and disciplined balance sheet assumptions to make the math work.

Result: Fair Value of $67.80 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on tanker demand holding up and on Teekay Tankers successfully renewing its fleet. Weaker oil trade or slower replacement could potentially pressure margins.

Find out about the key risks to this Teekay Tankers narrative.

Another Angle: Multiples Point the Other Way

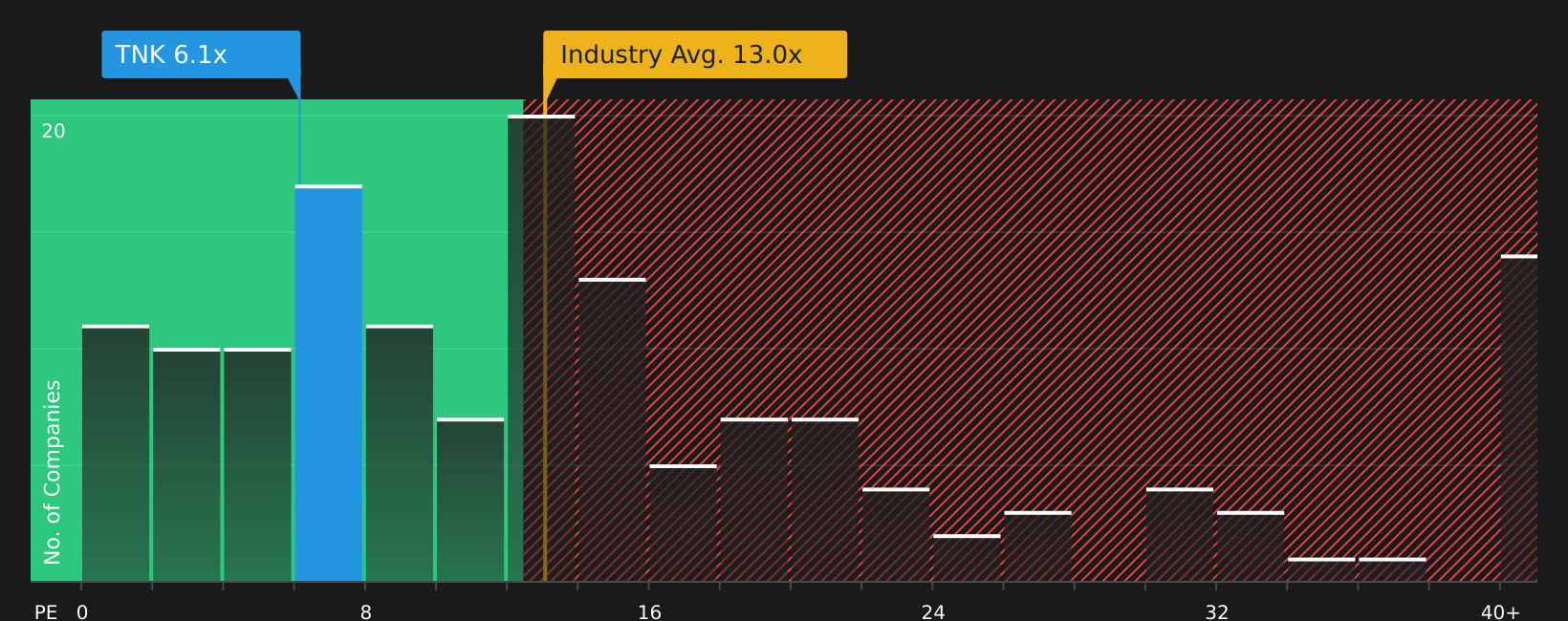

While the most popular narrative tags Teekay Tankers as 13.6% overvalued against a $67.80 fair value, the current P/E of 7.6x tells a different story. It sits well below peers at 13x, the US Oil and Gas average at 15.6x, and the fair ratio of 13.9x, which signals a wide gap the market could still close. So is the premium really in the price, or is the multiple hinting at a different balance of risk and reward?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals on value, risk, and reward, this is a moment to check the numbers yourself and decide where you stand. A good place to begin is 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If Teekay Tankers has your attention, do not stop here. The next winners you add to your watchlist could come from focused stock lists built around clear strengths.

- Target quality at a discount and scan 58 high quality undervalued stocks that combine strong fundamentals with prices that may not fully reflect their strengths.

- Strengthen your income stream and review 13 dividend fortresses that aim to pair higher yields with resilience.

- Prioritise resilience and stress test your portfolio with 68 resilient stocks with low risk scores that score well on stability and downside protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English