Penguin Solutions (PENG) Valuation Check After Recent Rebrand And Share Price Momentum

Understanding Penguin Solutions after its recent rebrand

Penguin Solutions (PENG) recently changed its name from SMART Global Holdings, a shift that brings its high performance computing, AI infrastructure, memory, and LED businesses together under a single, clearer identity for investors to evaluate.

See our latest analysis for Penguin Solutions.

The recent rebrand has arrived alongside sharp near term share price momentum, with a 1 day share price return of 13.37% and 7 day share price return of 23.97%. This is set against a 36.21% 1 year total shareholder return and a weaker 5 year total shareholder return of 25.97%.

If Penguin Solutions has put AI infrastructure on your radar, this is a good time to see what else is moving in the space and check out 36 AI infrastructure stocks

With PENG trading at US$20.69 and sitting at a discount to both analysts’ US$27.00 price target and one intrinsic value estimate, should you view this as a genuine entry point, or as a sign that markets already expect stronger growth ahead?

Price-to-Earnings of 27.6x: Is it justified?

At a last close of $20.69, Penguin Solutions is trading on a P/E of 27.6x, which lines up as cheaper than both the estimated fair P/E of 47.4x and the broader US Semiconductor industry average of 35.8x, but higher than the peer group average of 23.8x.

The P/E multiple compares what investors are currently paying for each dollar of earnings, so it effectively reflects how optimistic the market is about future profitability. For a business operating across high performance computing, AI infrastructure, memory, and LEDs, earnings expectations can be sensitive to how reliably cash flows scale from these segments.

Here, the market is assigning a richer multiple than direct peers, which suggests expectations for stronger earnings than that smaller group. Yet the P/E still sits well below both the sector average and the SWS fair P/E level that our model suggests the price could move toward if the market reassesses those earnings. That spread between 27.6x and 47.4x leaves room for sentiment to shift if future results line up with current forecasts.

Compared with the US Semiconductor industry on 35.8x, Penguin Solutions trades at a discount that implies the wider sector is pricing in even higher earnings optimism than the stock currently receives. The gap to the 47.4x fair ratio also points to valuation headroom that a more bullish market could close.

Explore the SWS fair ratio for Penguin Solutions

Result: Price-to-Earnings of 27.6x (UNDERVALUED)

However, you also need to factor in risks such as execution across three different segments and any future reset in expectations if earnings forecasts prove too optimistic.

Find out about the key risks to this Penguin Solutions narrative.

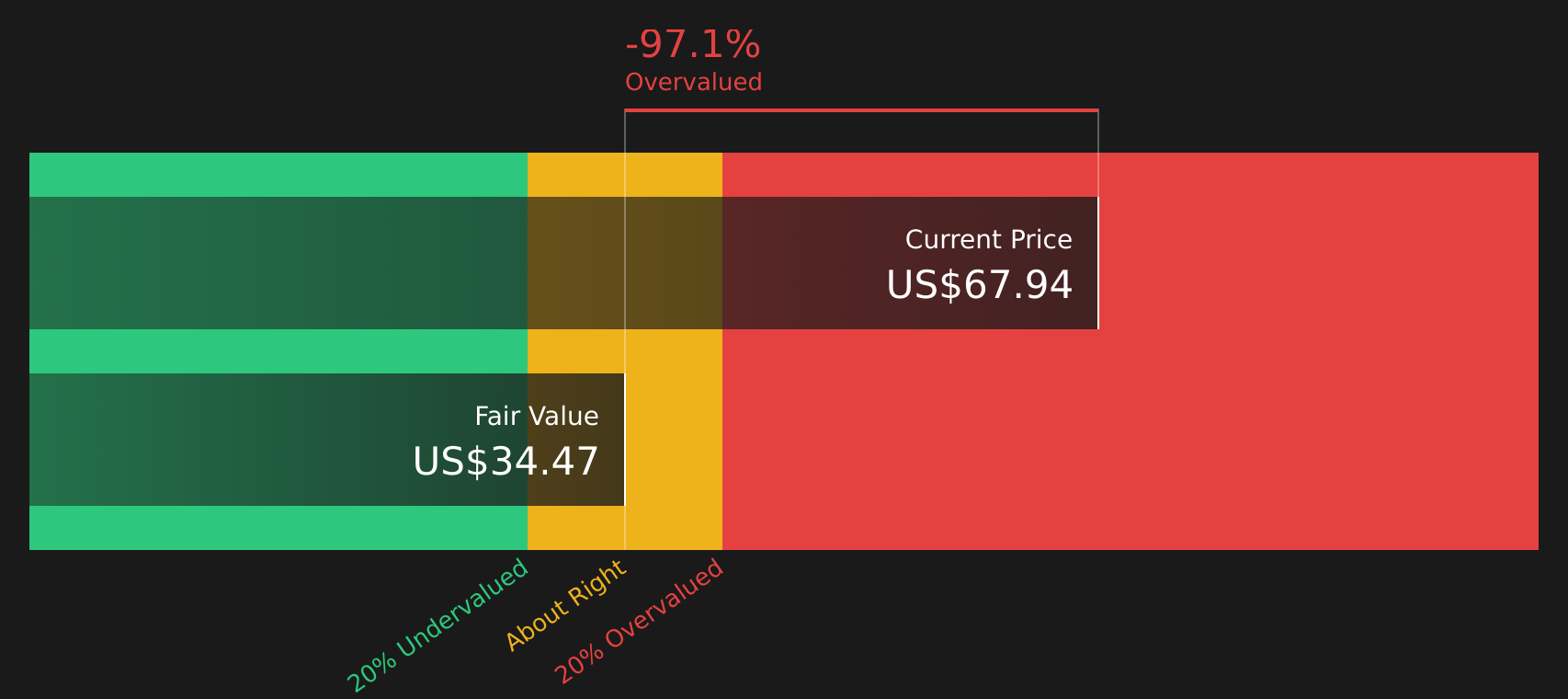

Another view: DCF points to a deeper discount

While the P/E suggests Penguin Solutions is priced below its fair ratio, the SWS DCF model goes further, putting fair value at $36.34 versus the current $20.69. That indicates a 43.1% discount. This raises the question of whether the earnings-based multiple is understating what future cash flows could be worth.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Penguin Solutions for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 58 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of signals here may feel balanced rather than clearly bullish or bearish, so act while the data is fresh and test the story against your own expectations by weighing up 4 key rewards

Looking for more investment ideas?

If Penguin Solutions has caught your attention, do not stop here. Use this momentum to line up other stocks that could fit your style and goals.

- Target potential value opportunities by scanning for companies that combine quality fundamentals with appealing pricing using the 58 high quality undervalued stocks.

- Prioritize resilience by focusing on businesses with strong financial footing through the solid balance sheet and fundamentals stocks screener (40 results).

- Hunt for potential future standouts that may not be widely followed yet through the screener containing 25 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English