Will Stronger M&A And Valuation Advisory Earnings Change Houlihan Lokey's (HLI) Risk-Reward Narrative?

- In early April 2026, Houlihan Lokey reported third-quarter fiscal 2026 results that beat analyst expectations, with adjusted earnings per share of US$1.94 and revenue of US$717 million, driven largely by growth in its M&A and valuation advisory businesses even as restructuring activity softened.

- The company also disclosed a small insider sale by its General Counsel and a prospectus supplement for the potential resale of 32,421 shares tied to a prior acquisition, highlighting how dealmaking and integration continue to influence its capital structure and earnings mix.

- We’ll now examine how stronger M&A and valuation advisory earnings reshape Houlihan Lokey’s existing investment narrative and its risk-reward profile.

Find 58 companies with promising cash flow potential yet trading below their fair value.

Houlihan Lokey Investment Narrative Recap

To own Houlihan Lokey, you need to believe the firm can balance cyclical swings between M&A and restructuring while keeping margins intact despite high compensation costs. The latest earnings beat supports confidence in its dealmaking and valuation franchises, but the stock’s pullback underscores how quickly sentiment can shift if restructuring stays weak. For now, the news mostly sharpens, rather than changes, the key risk that revenue remains heavily tied to U.S. deal volumes.

The most relevant disclosure here is the strong third quarter, where M&A and valuation advisory produced 24% pretax earnings growth and now account for over three quarters of the business. That mix reinforces the near term catalyst of recovering deal activity, but also raises the stakes if global M&A outside the U.S. remains subdued. The small insider sale and resale prospectus look immaterial against these bigger questions about revenue concentration and cost discipline.

Yet behind the stronger M&A numbers, investors should still be aware of how quickly restructuring revenue can fade if...

Read the full narrative on Houlihan Lokey (it's free!)

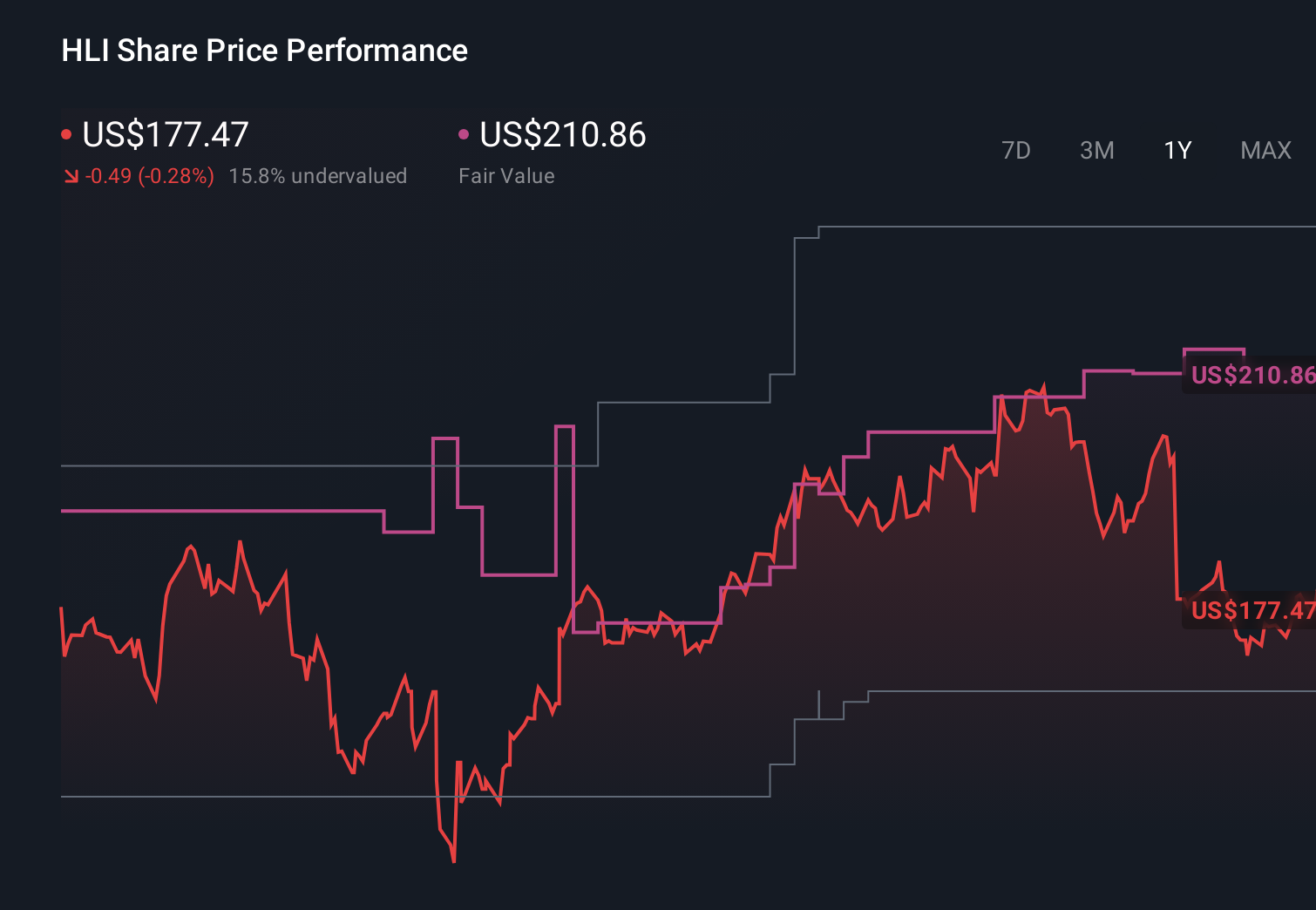

Houlihan Lokey's narrative projects $3.5 billion revenue and $654.6 million earnings by 2028.

Uncover how Houlihan Lokey's forecasts yield a $210.86 fair value, a 49% upside to its current price.

Exploring Other Perspectives

Before this earnings surprise, the most optimistic analysts were penciling in about US$3.8 billion of revenue and US$653.0 million of earnings by 2028, which is far more upbeat than the consensus. If you are weighing that bullish view against the risk that restructuring underperforms when defaults stay low, this quarter’s news could either reinforce or challenge those expectations, so it is worth comparing how your own assumptions differ from these pre news forecasts.

Explore 2 other fair value estimates on Houlihan Lokey - why the stock might be worth just $190.51!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Houlihan Lokey research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Houlihan Lokey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Houlihan Lokey's overall financial health at a glance.

Looking For Alternative Opportunities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English