358,023 Reasons to Consider Selling Tesla Stock Here

Recently, Tesla (TSLA) reported its first-quarter production and delivery figures. The company’s production for the quarter totaled 408,386 units, up 12.6% year-over-year (YOY). Model 3/Y production stood at 394,611 units. However, investors did not take kindly to the numbers, as the stock dropped 5.4% intraday on Apr. 2. The quarterly delivery figure of 358,023 units, although underscoring a 6.3% YOY increase, fell short of the 365,000 consensus estimate.

Tesla’s electric vehicle (EV) business has come under pressure as the company shifts its focus to energy storage offerings, Cybercab, and Optimus. Moreover, the pullback of the $7,500 federal tax credit has likely affected affordability for Tesla customers, while competition intensifies in the industry.

Against this backdrop, we take a closer look at Tesla as investors await its Q1 financials, to be reported Apr. 22 after market close.

About Tesla Stock

An American EV giant, Tesla also sells clean energy equipment, such as solar panels and battery storage. The company is seen as an influential giant, having accelerated the global shift toward electric mobility, pressuring rivals to electrify and normalizing EVs as desirable.

Tesla has long outgrown its image as purely an electric vehicle maker, pivoting toward a broader tech innovator by embedding advanced software, AI, and robotics into its ecosystem. This shift reframes cars as intelligent platforms, energy systems as smart grids, and future products, such as humanoid robots, as versatile AI companions.

On the other hand, the company is not without its controversies. Tesla’s rapid growth has brought scrutiny over production consistency, ambitious timelines, and quality issues. Headquartered in Austin, Texas, Tesla has a massive market capitalization of $1.35 trillion.

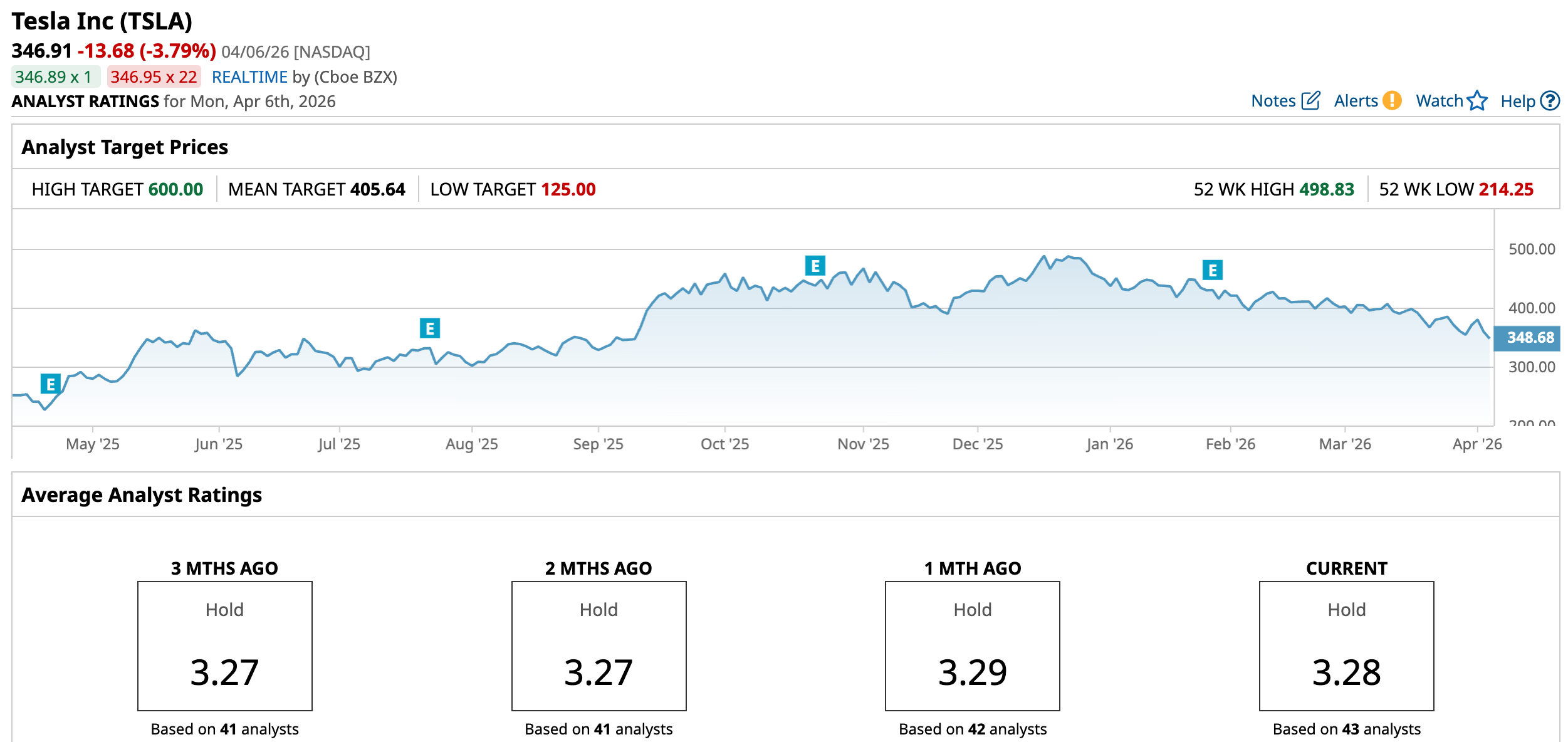

The company’s stock reached an all-time intraday high of $498.83 in December 2025, but it is down 30% from that level. Although down from its historic highs, the stock has gained 46.74% over the past 52 weeks. However, Tesla has recently been hit by a barrage of headwinds, including increased competition and reduced EV tax credits, which have led to a selloff. The company’s stock is down 21.87% year-to-date (YTD).

Tesla’s 14-day RSI stands at 36.10, indicating that, due to persistent downward pressure, the stock is closer to being oversold than overbought. However, it also comes with a hefty valuation. Its forward-adjusted price-to-earnings (non-GAAP) ratio of 174.57 times is significantly higher than the industry average of 14.64 times.

Factors Affecting Tesla

Of the barrage of factors hindering its solid growth trajectory, chief among them is the intensifying competition in the EV industry. Chinese automakers like BYD (BYDDY), Nio (NIO), and Xpeng (XPEV) have essentially flooded the market with cheaper alternatives that match many of Tesla’s features. The lower price point of these vehicles makes them well-suited to value propositions in markets like Asia and Europe. After multiple price cuts through 2024 and 2025, Tesla likely has few remaining options for price reductions.

Amid this, Federal safety regulators from the National Highway Traffic Safety Administration (NHTSA) have intensified their probe into Tesla’s Full Self-Driving (supervised) system after identifying several crashes, including a fatal one, in which FSD did not operate as intended. The probe originally started in 2024 and was recently escalated to an “engineering analysis.” The move comes as Tesla is set to launch its driverless robotaxi called Cybercab.

Nevertheless, investors are assessing Tesla through the lens of a software and energy storage company rather than just an EV maker. This changes the narrative of the view for investors of the firm's long-term growth drivers. The future of this tech giant seems to lie in FSD and physical AI, such as its humanoid robot Optimus. CEO Elon Musk has stated that the Optimus third-gen robot is mobile but not yet ready to be unveiled, although the earlier goal was to release it in the first quarter itself.

Tesla Delivered 2025 Results Amid EV Market Pressures

Tesla reported subdued results last year, with production falling 7% YOY and deliveries dropping 9%. This was also the second year in a row that the company reported drops in production and delivery units. Conversely, its storage solution offerings have grown, with storage deployed rising 49% from the prior year to 46.7 GWh. Moreover, active FSD subscriptions rose by 38% YOY to 1.10 million.

Tesla’s total revenues declined by 3% YOY to $94.83 billion, as automotive revenues fell 10% to $69.53 billion. There were also persistent margin pressures, as its adjusted EBITDA margin dropped by 104 basis points to 15.4%. Its annual non-GAAP EPS decreased 28% from the prior year to $1.66.

Analysts still believe Tesla has the ability to grow its bottom line. For the current year, Tesla’s EPS (on a diluted basis) is expected to grow 31.2% YOY to $1.43, followed by a 37.1% increase to $1.96 for the next year.

What Do Analysts Think About Tesla’s Stock?

Wall Street analysts have differing opinions on Tesla’s stock at the moment. Last month, analysts at Canaccord Genuity lowered the stock's price target from $520 to $420, but kept the rating at “Buy.” Canaccord analysts noted the company’s sluggish performance in China, while weak conditions prevail in the U.S. and Europe.

On the other hand, GLJ Research analysts reiterated a “Sell” rating on Tesla, stating that its Q1 volume increase was margin-dilutive subsidy arbitrage in Korea rather than organic demand recovery.

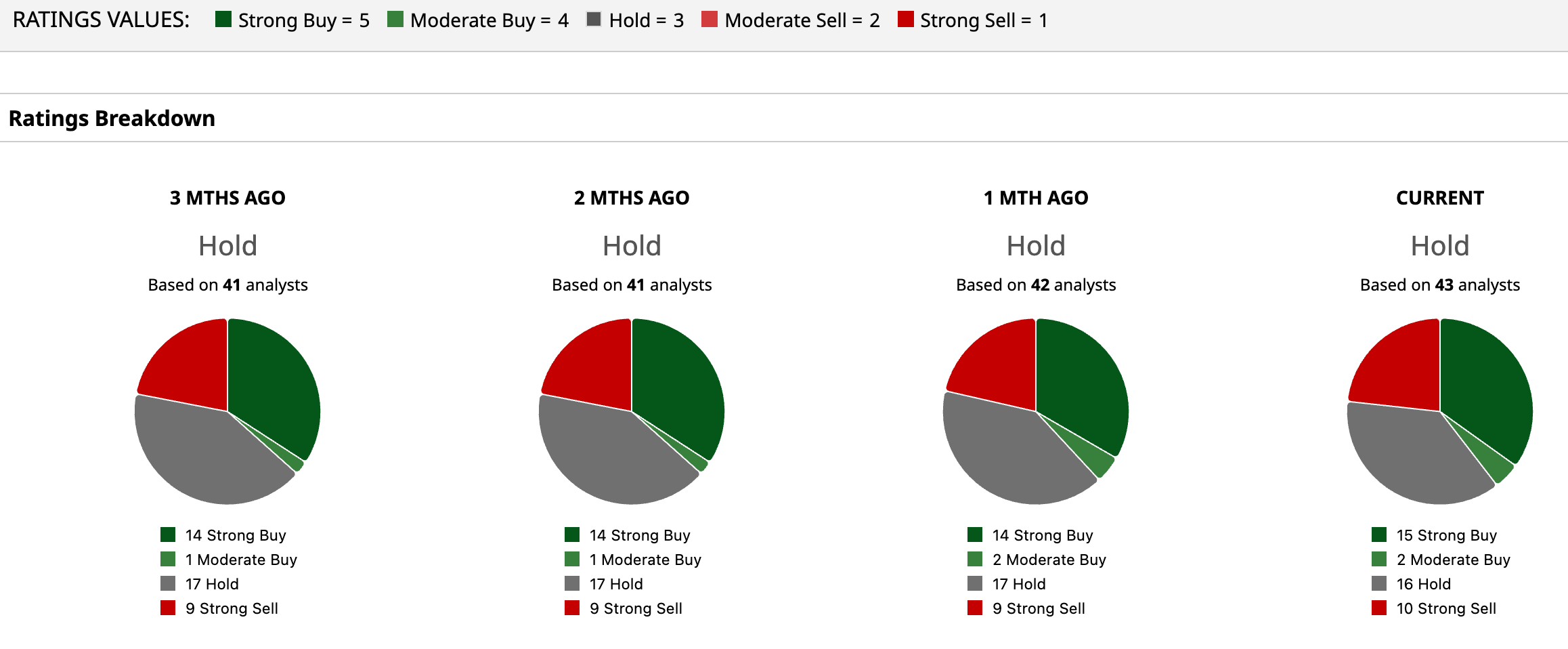

Wall Street analysts are taking a cautious stance on Tesla’s stock now, with a consensus “Hold” rating overall. Of the 43 analysts rating the stock, 15 analysts gave a “Strong Buy” rating, two analysts gave a “Moderate Buy” rating, while 16 analysts are playing it safe with a “Hold” rating, and 10 analysts gave a “Strong Sell” rating. The consensus price target of $405.64 represents a 16.9% upside from current levels. Moreover, the Street-high price target of $600 indicates a 73% upside from current levels.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English