The Bull Case For GoDaddy (GDDY) Could Change Following Its New AI Agentic Web Push – Learn Why

- In early April 2026, Cloudflare and GoDaddy announced a partnership to integrate AI Crawl Control into GoDaddy’s hosting platform, while GoDaddy also introduced an upgraded mobile app and enabled LegalZoom to register a cryptographically verifiable AI agent via GoDaddy ANS.

- Together, these moves position GoDaddy as a key infrastructure provider for the emerging agentic web, giving small businesses more control over how AI systems access and monetize their online content.

- We’ll now examine how GoDaddy’s AI Crawl Control integration and agent identity initiatives may influence its existing investment narrative.

Find 62 companies with promising cash flow potential yet trading below their fair value.

GoDaddy Investment Narrative Recap

To own GoDaddy, you need to believe its core domain and web presence base can keep supporting higher value software and AI services, even as competition intensifies. The Cloudflare AI Crawl Control deal and LegalZoom agent registration do not change the near term earnings and churn risk story in a material way, but they do tie GoDaddy more tightly to how AI interacts with small business websites.

Among the recent updates, the expanded GoDaddy app feels most directly linked to the existing catalyst of higher attach rates and ARPU from small businesses. By pulling website building, domains, messaging, and marketing into a mobile hub, it reinforces GoDaddy’s push toward recurring, higher margin services that sit on top of its domain franchise, even as investors weigh slower forecast revenue growth against that thesis.

Yet while these AI and app moves are encouraging, you should also understand how rising regulatory and privacy costs could quietly pressure margins over time and...

Read the full narrative on GoDaddy (it's free!)

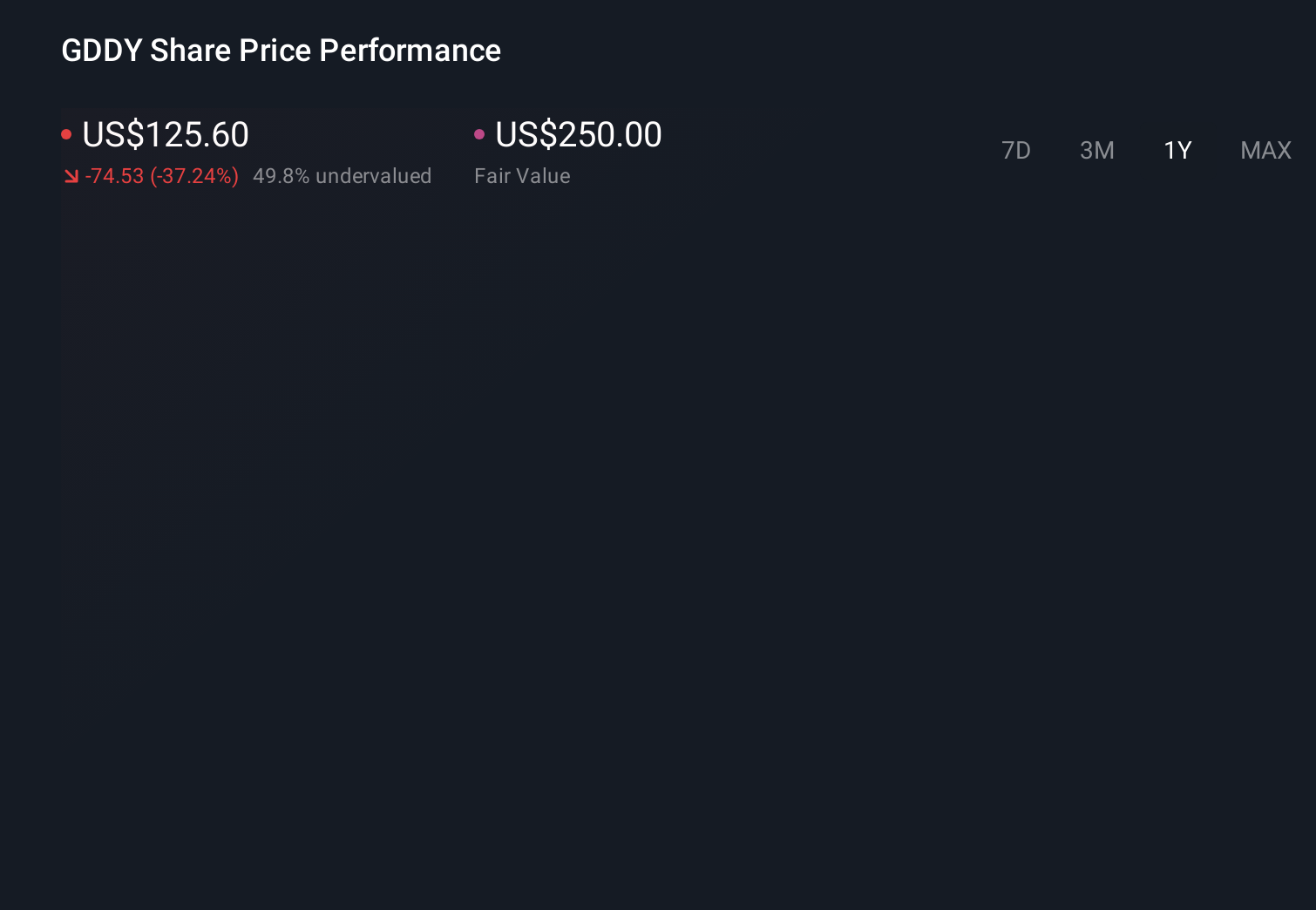

GoDaddy's narrative projects $5.9 billion revenue and $1.3 billion earnings by 2028. This requires 7.7% yearly revenue growth and an earnings increase of about $0.5 billion from $808.5 million today.

Uncover how GoDaddy's forecasts yield a $119.43 fair value, a 48% upside to its current price.

Exploring Other Perspectives

The most cautious analysts already assumed only about US$5.9 billion of revenue and US$1.1 billion of earnings by 2028, and they worry that GoDaddy’s AI agent identity push could still struggle to stand out or scale, which is a much more pessimistic take than the consensus and a reminder that your own view of these new announcements may lead you toward very different conclusions.

Explore 4 other fair value estimates on GoDaddy - why the stock might be worth just $117.67!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your GoDaddy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free GoDaddy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GoDaddy's overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English