Has Viasat (VSAT) Rallied Too Far After Recent Satellite Connectivity Headlines

- If you are wondering whether Viasat's share price still reflects good value or has already run too far, you will want to look closely at what the numbers are saying about its valuation.

- The stock last closed at US$55.39, with returns of 3.2% over the past week, 19.6% over the past month, 47.2% year to date, and a very large gain over the last year that is more than 6x.

- Recent headlines around Viasat have focused on its position in satellite communications and connectivity contracts. This helps frame how investors think about its future cash flows and risk profile and provides important context for the sharp share price moves you may have seen.

- Viasat currently holds a valuation score of 5 out of 6. The rest of this article will break down what different valuation methods say about that score, then finish with a broader way to think about what "fair value" really means for you as an investor.

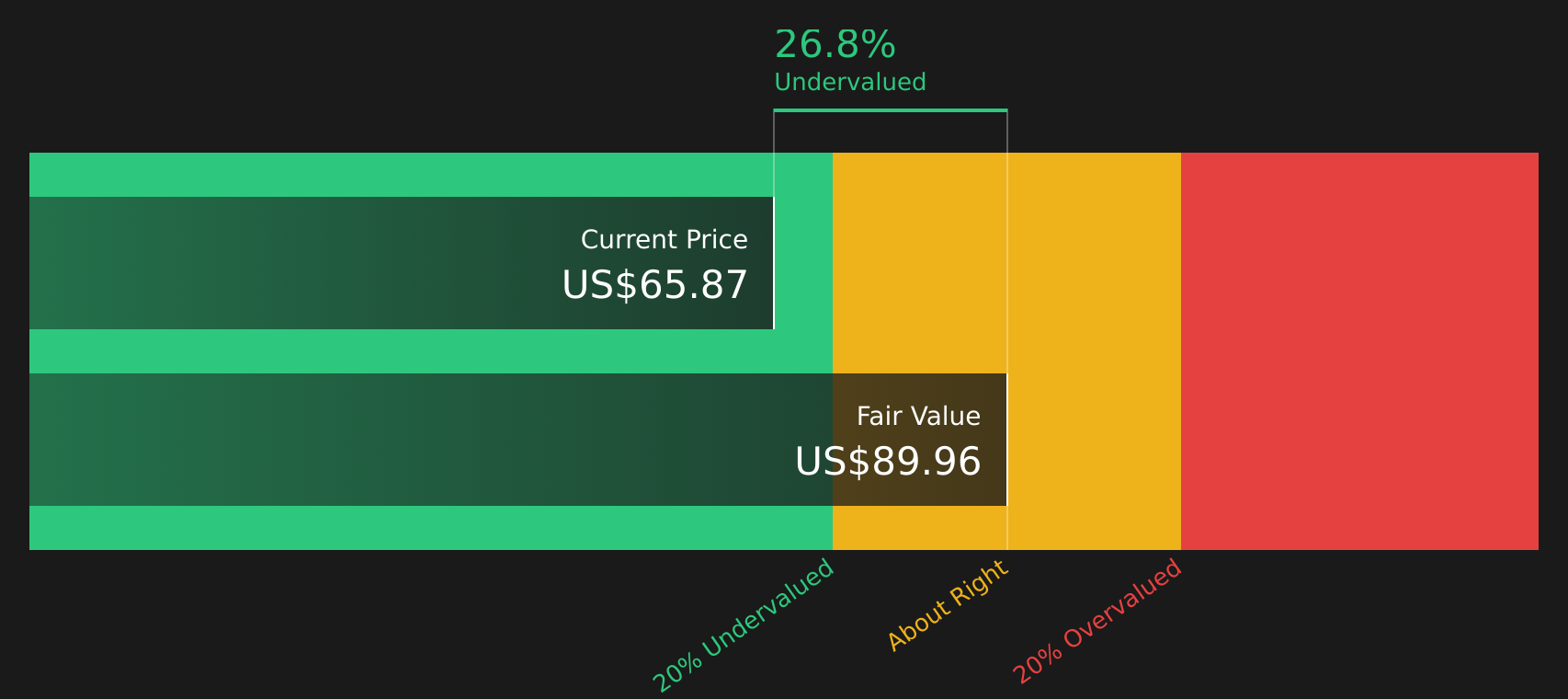

Approach 1: Viasat Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model starts with estimates of a company’s future cash flows and then discounts those back to today’s dollars to arrive at an intrinsic value per share.

For Viasat, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $289.7 million. Analysts provide specific projections out to 2028, with free cash flow for that year estimated at $555.2 million, and Simply Wall St then extrapolates further out to 2035. All of these future cash flows are discounted back into today’s money using the DCF framework.

On this basis, the DCF model suggests an intrinsic value of about $75.80 per share, compared with the recent share price of $55.39. That gap implies the stock is around 26.9% undervalued according to these cash flow assumptions and discount rates.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Viasat is undervalued by 26.9%. Track this in your watchlist or portfolio, or discover 62 more high quality undervalued stocks.

Approach 2: Viasat Price vs Sales

For companies where earnings can be volatile or negative, the P/S ratio is often a useful way to compare what the market is paying for each dollar of revenue. It sidesteps short term swings in profit and focuses on the top line, which can be especially relevant in capital intensive sectors like communications.

In general, higher growth expectations or lower perceived risk can justify a higher “normal” P/S multiple, while slower growth or higher risk usually support a lower multiple. Viasat currently trades on a P/S of 1.63x. That sits below the communications industry average of 2.22x and well below the peer group average of 9.69x, which on the surface points to a lower revenue multiple than many comparables.

Simply Wall St’s Fair Ratio for Viasat is 2.13x. This is a proprietary estimate of what the P/S might be given factors such as earnings growth, profit margins, industry, market cap and company specific risks. Because it blends these elements rather than relying only on broad peer or industry comparisons, it can give a more tailored sense of what “fair” looks like. With the current 1.63x P/S sitting below the 2.13x Fair Ratio, the shares screen as undervalued on this measure.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Viasat Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Meet Narratives, a simple tool on Simply Wall St’s Community page that lets you set your own story for Viasat, link it to specific forecasts for future revenue, earnings and margins, and then see a Fair Value that you can compare with the current price to decide whether the trade off looks attractive for you.

Each Narrative connects three pieces: your view of Viasat’s story, the numbers that go with that view, and the Fair Value that falls out of those assumptions. It then updates automatically when fresh information such as news or earnings is added to the platform.

For example, one Viasat Narrative currently aligns with a higher Fair Value of US$58.00 and assumes revenue growth of 6.9% a year, earnings of US$589.1m by around March 2029 and a P/E of 20.6x. A more cautious Narrative points to a Fair Value of about US$26.66, revenue growth of 3.25% a year, earnings of US$393.4m by around 2028 and a future P/E of 10.48x. Your job as an investor is to decide which story you believe is closer to reality or to create your own in between.

For Viasat however we will make it really easy for you with previews of two leading Viasat Narratives:

Fair Value in this bullish Narrative: US$58.00 per share

Current price vs this Fair Value: around 4.5% below the Narrative Fair Value

Revenue growth used in this Narrative: 6.93% a year

- Assumes ViaSat 3, shared infrastructure and multi orbit networks expand the serviceable market and support higher free cash flow over time.

- Builds in higher profit margins and earnings by 2029, with the business valued on a future P/E that is below the broader US Communications industry level quoted in the Narrative.

- Flags real execution risks around LEO competition, high capital expenditure, integration of Inmarsat and pressure on satellite broadband demand.

Fair Value in this more cautious Narrative: US$41.13 per share

Current price vs this Fair Value: around 34.7% above the Narrative Fair Value

Revenue growth used in this Narrative: 4.14% a year

- Anchors on a lower Fair Value range that reflects execution risk on ViaSat 3, integration work and possible defense spinout scenarios.

- Builds in modest revenue growth, higher discount rate assumptions in earlier work and a need for the business to improve margins from loss making levels to industry type profitability.

- Highlights concerns around high capital spending, subscriber declines in US fixed broadband, stronger competitors and ongoing regulatory and legal costs.

Taken together, these two Narratives frame the current debate around Viasat, with one set of assumptions pointing to additional upside and another arguing that expectations are already full. Your next step is to decide which story lines up better with your own view of the business risks and future cash flows, or to create a Narrative that sits between these two bookends.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Viasat on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Viasat? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English