CNH Industrial (CNH) Is Up 7.9% After Mixed 2025 Results And Analyst Debate Intensifies

- In the past few days, CNH Industrial reported its fourth-quarter and full-year 2025 results, highlighting softer equipment demand alongside operational progress and lower dealer inventories.

- At the same time, differing analyst views following the update have sharpened the debate over how effectively CNH Industrial is managing through a weaker machinery cycle.

- We’ll now explore how CNH Industrial’s weaker equipment demand yet improved operational execution may influence its existing investment narrative and outlook.

Find 55 companies with promising cash flow potential yet trading below their fair value.

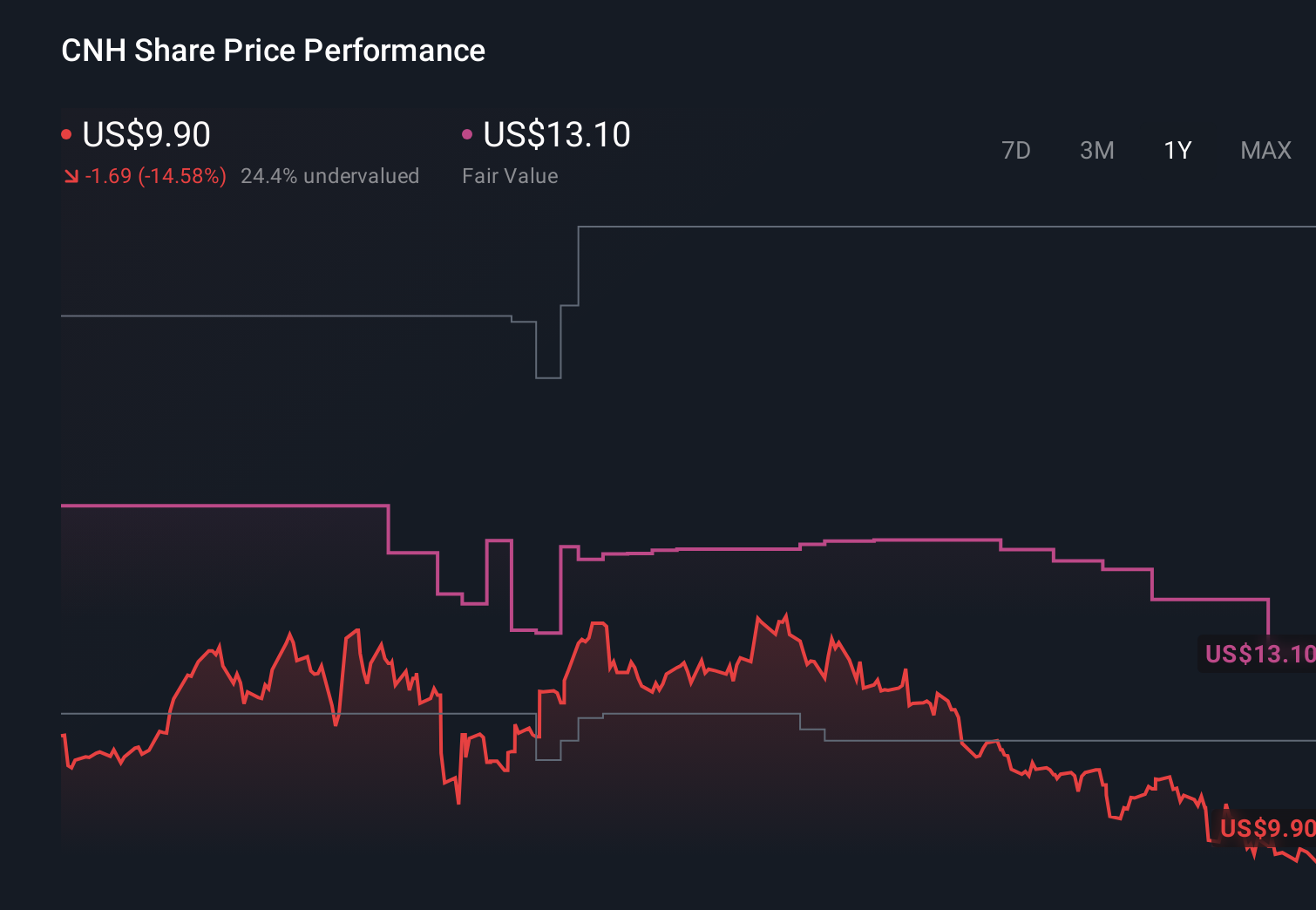

CNH Industrial Investment Narrative Recap

To own CNH Industrial, you need to believe that its push into connected, precision equipment and operational discipline can offset a softer machinery cycle. The latest results, showing weaker equipment demand but better execution and leaner dealer inventories, keep the near term catalyst squarely on how efficiently CNH converts this trough period into healthier margins, while the key risk remains pressure on profitability from softer North American ag markets and higher input costs. For now, this news does not radically change that balance.

Among recent announcements, the most relevant here is CNH’s decision to extend its EUR 3.25 billion revolving credit facility out to 2031. In the context of weaker equipment demand and mixed analyst views, this additional liquidity flexibility matters because it can support ongoing investments in precision technology, product refreshes, and operational improvements that many investors see as central to the company’s longer term earnings potential once demand conditions improve.

Yet behind the operational progress, investors should be aware that rising input costs and tariff uncertainty could still...

Read the full narrative on CNH Industrial (it's free!)

CNH Industrial's narrative projects $18.7 billion revenue and $1.6 billion earnings by 2028. This requires 1.2% yearly revenue growth and a $777.0 million earnings increase from $823.0 million today.

Uncover how CNH Industrial's forecasts yield a $13.99 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much tougher picture than consensus, assuming roughly flat revenues near US$18.4 billion and earnings of about US$1.1 billion by 2028, and warning that if CNH falls behind in precision and autonomous tech, the current debate over weaker demand and inventory management could look mild compared with the longer term competitive and margin risks they see.

Explore 6 other fair value estimates on CNH Industrial - why the stock might be worth as much as 62% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your CNH Industrial research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CNH Industrial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CNH Industrial's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English