Expanded Electro Dépôt Automation Contract Might Change The Case For Investing In GXO Logistics (GXO)

- GXO Logistics has renewed and expanded its long-standing partnership with French retailer Electro Dépôt, enlarging the Fos-sur-Mer distribution center to 55,000 square meters and adding a new 24,000-square-meter, automation-enabled facility in Port-Saint-Louis-du-Rhône to support small domestic appliance logistics across southern France and Spain.

- The partnership now blends advanced warehouse automation with on-site solar power and electric vehicle charging, tying Electro Dépôt’s supply chain expansion directly to GXO’s technology and ESG-focused logistics solutions in a key European port hub.

- We’ll now examine how this expanded, automation-rich Electro Dépôt contract could influence GXO’s investment narrative around growth, efficiency and ESG.

Find 59 companies with promising cash flow potential yet trading below their fair value.

GXO Logistics Investment Narrative Recap

To own GXO, you generally need to believe that outsourced, tech-enabled logistics and multi-year blue-chip contracts can turn modest organic revenue growth into improving profitability over time. The expanded Electro Dépôt deal reinforces the automation and ESG elements of that thesis, but by itself it does not clearly change the most immediate swing factors, which still look tied to Wincanton integration execution and leadership stability after significant senior management turnover.

The recent appointment of Ajit Kara as Senior Vice President of Account Management looks particularly relevant here. As GXO scales high-profile contracts like Electro Dépôt, a dedicated account management leader could matter for keeping large customers satisfied and expanding wallet share, which ties directly into the contract win pipeline that many investors see as a key near term catalyst, especially following guidance for 2026 organic revenue growth of 4% to 5%.

Yet beneath the automation headlines, investors should be aware of how integration risk around Wincanton could still...

Read the full narrative on GXO Logistics (it's free!)

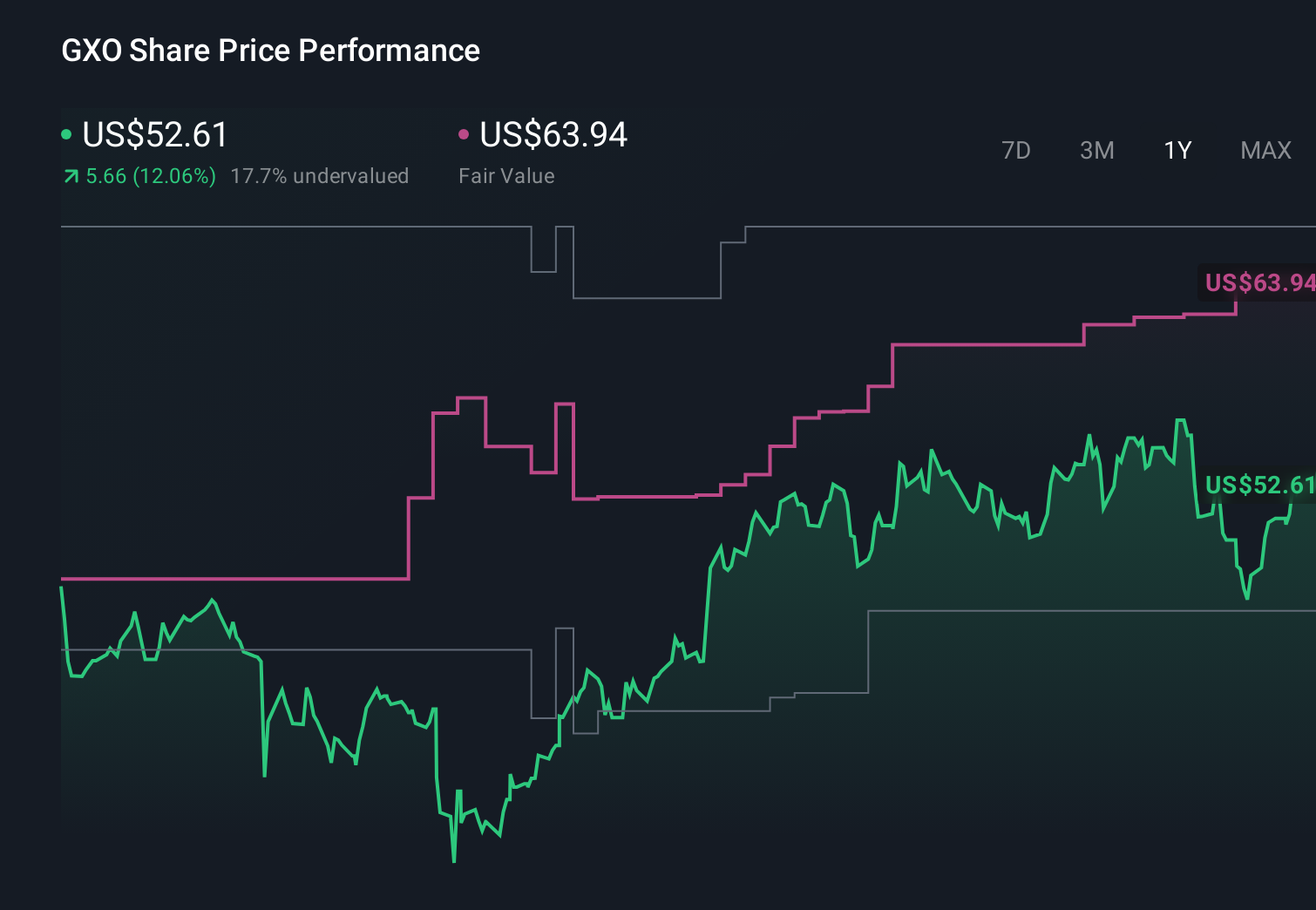

GXO Logistics' narrative projects $15.5 billion revenue and $318.9 million earnings by 2029.

Uncover how GXO Logistics' forecasts yield a $71.56 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts paint a more cautious picture, assuming revenue of about US$13.4 billion and earnings near US$173.8 million by 2028, so when you weigh this Electro Dépôt expansion against their focus on customer capacity realignments squeezing EBITDA, it highlights how differently you and other investors might interpret the same news and why it is worth comparing multiple viewpoints before deciding what it means for GXO’s story.

Explore 3 other fair value estimates on GXO Logistics - why the stock might be worth just $58.04!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your GXO Logistics research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free GXO Logistics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GXO Logistics' overall financial health at a glance.

No Opportunity In GXO Logistics?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English