Assessing Avista (AVA) Valuation After Recent Share Price Momentum

What recent returns say about Avista (AVA) right now

With no single headline event driving attention, Avista (AVA) is back on the radar as investors reassess the regulated utility after a month that included a 5.3% return and a past 3 months gain of 4.2%.

See our latest analysis for Avista.

At a share price of $41.88, Avista’s recent 5.3% 30 day share price return and 8.2% year to date share price return contrast with a 5.2% 1 year total shareholder return, suggesting momentum has picked up recently.

If Avista’s move has you thinking about other regulated and infrastructure linked ideas, it could be a good moment to scan 30 power grid technology and infrastructure stocks

With Avista trading at $41.88, sitting close to a $42.00 analyst target and carrying a value score of 3, the key question is whether this regulated utility is still mispriced or if the market already reflects its future growth.

Most Popular Narrative: 3.8% Overvalued

Avista’s most followed narrative puts fair value at about $40.33, a touch below the recent $41.88 close, which sets up a tight valuation debate.

Robust, multi-year capital investment plans approaching $3 billion (2025 to 2029), with additional upside from grid expansion projects and new generation needs tied to large load requests, position Avista to earn regulated returns and drive long-term earnings expansion.

Want to see what is baked into that price tag? Revenue growth, margin shifts, and a future earnings multiple all work together here, and the exact mix may surprise you.

Using a 6.98% discount rate, the narrative links those long range cash flow expectations to a fair value that sits slightly below where the shares trade today, so the gap is small but meaningful for investors who care about entry points.

Result: Fair Value of $40.33 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still meaningful risk that wildfire exposure and heavier grid investment needs, if not fully recovered in rates, could pressure cash flows and reduce flexibility.

Find out about the key risks to this Avista narrative.

Another way to look at Avista’s price

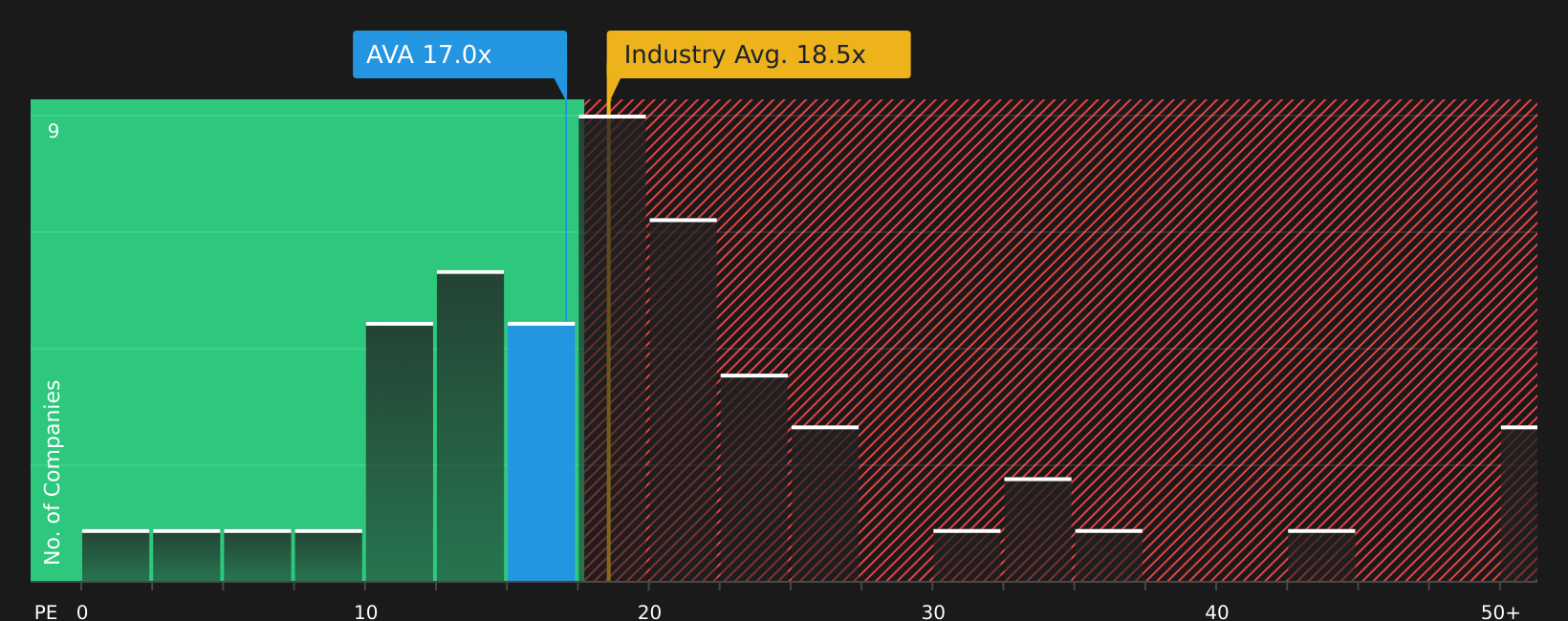

While the narrative model points to Avista being about 3.8% above its $40.33 fair value, the current P/E of 17.8x tells a slightly different story. That multiple sits below both the global Integrated Utilities average of 19.3x and an 18.4x fair ratio, which hints at only limited mispricing either way. Where does that leave you on the risk versus upside trade off?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment finely balanced between risk and reward, this is a good moment to act quickly and test the data for yourself using the 4 key rewards and 2 important warning signs

Ready for more investment ideas?

Do not stop with a single utility stock. Broader context across different types of companies can sharpen your judgment and help you spot opportunities others overlook.

- Target resilience by scanning companies that appear better equipped for shocks through the 71 resilient stocks with low risk scores.

- Zero in on value by reviewing businesses that combine quality metrics with appealing prices via the 58 high quality undervalued stocks.

- Strengthen your income options by checking companies that focus on returning cash to shareholders using the 11 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English