Does StoneCo's (STNE) Linx-Funded Special Dividend Reveal Its Evolving Capital Allocation Playbook?

- StoneCo Ltd. previously announced that its Board approved an extraordinary cash dividend of US$2.53 per share, paid on May 4, 2026, to shareholders of record on April 24, 2026, alongside an increase of about 3.8 million shares for its Long Term Incentive Plan.

- This one‑time dividend, funded by proceeds from the completed Linx sale, highlights how StoneCo is choosing to return excess capital while expanding its incentive pool.

- Now, we’ll examine how this extraordinary dividend funded by the Linx sale affects StoneCo’s capital allocation and broader investment narrative.

We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

StoneCo Investment Narrative Recap

To own StoneCo, you largely need to believe in its ability to keep growing with Brazil’s shift to digital payments and financial services for small businesses, while managing credit and competition risks. The one time US$2.53 per share dividend funded by the Linx sale mainly reshapes how excess capital is returned, rather than changing the near term business catalyst of client and revenue growth or the key risk around slower TPV and higher credit costs.

The extraordinary dividend sits alongside an active capital return story, including the BRL 2,000 million buyback program under which StoneCo had already repurchased over 29 million shares by late 2025. Together, these moves frame how the company is choosing between reinvestment, buybacks, and cash returns at a time when earnings reached about BRL 2,360.7 million in 2025, which could influence how you think about both upside catalysts and balance sheet risk.

Yet against this backdrop of cash returns and earnings progress, the risk of rising competition and alternative payment rails is something investors should be aware of...

Read the full narrative on StoneCo (it's free!)

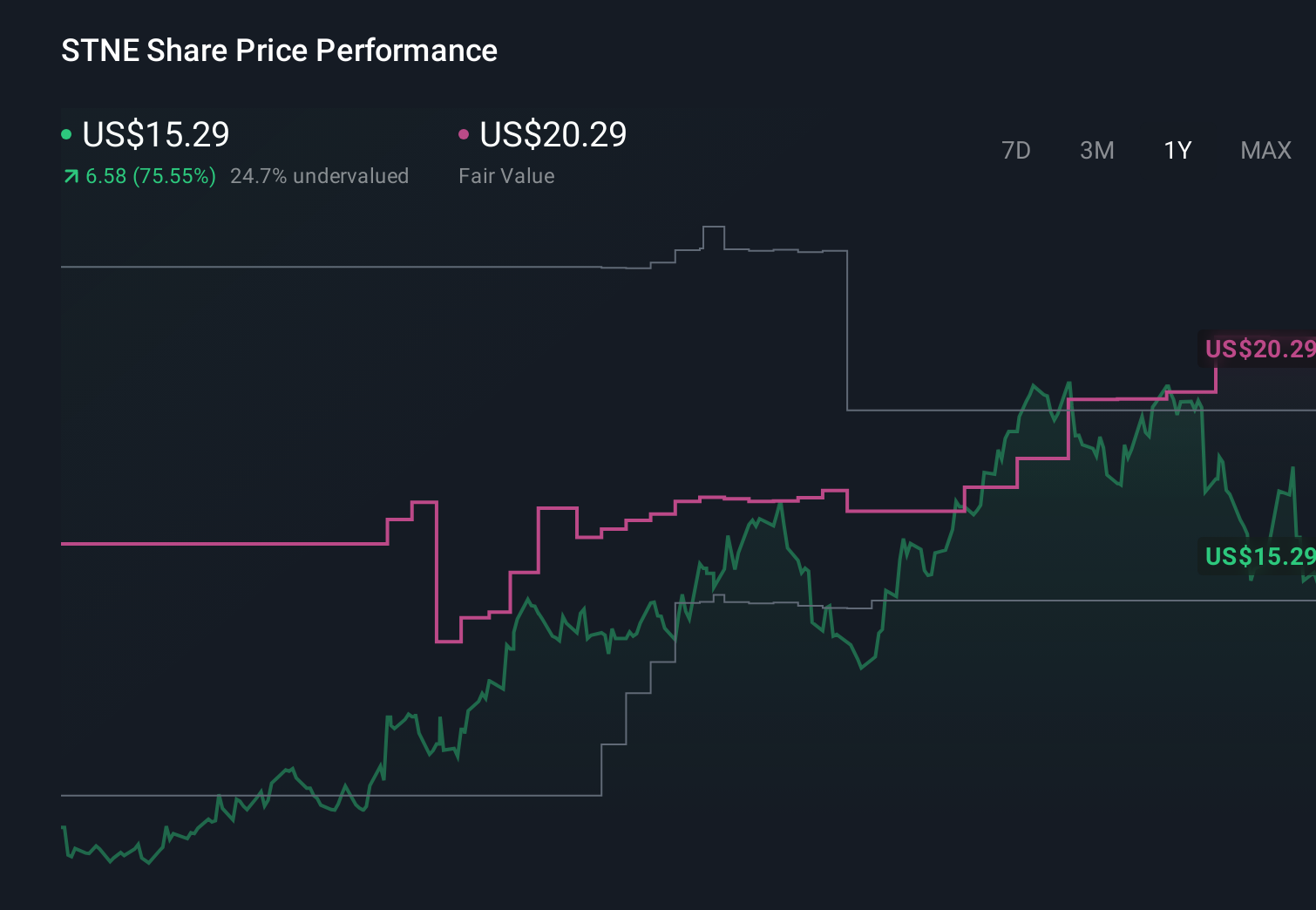

StoneCo’s narrative projects R$17.4 billion revenue and R$5.0 billion earnings by 2028. This requires 8.2% yearly revenue growth and an earnings increase of roughly R$6.3 billion from R$-1.3 billion today.

Uncover how StoneCo's forecasts yield a $20.29 fair value, a 34% upside to its current price.

Exploring Other Perspectives

While consensus focuses on steady growth and capital returns, the most optimistic analysts, who once projected earnings near R$5.4 billion by 2029, see far greater upside potential that the Linx funded dividend might reinforce or challenge as views on competition and transaction growth evolve.

Explore 9 other fair value estimates on StoneCo - why the stock might be worth 13% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your StoneCo research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free StoneCo research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate StoneCo's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English