ePlus’ AI-Era Memory Reclamation Push Might Change The Case For Investing In ePlus (PLUS)

- Earlier in April 2026, ePlus announced a Memory Optimization and Reclamation Assessment aimed at helping enterprises reclaim underused memory capacity amid severe AI-driven memory chip shortages and supply chain constraints identified by Gartner.

- By focusing on uncovering “zombie” and stranded memory and providing an optimization roadmap with cost-avoidance insights, ePlus is positioning itself as a practical partner for customers struggling to secure or afford new memory hardware.

- Next, we’ll examine how this memory optimization push, amid sector relief from easing Middle East tensions, may reshape ePlus’s investment narrative.

Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

ePlus Investment Narrative Recap

To own ePlus, you need to believe it can convert strong demand for AI, cloud and security “plumbing” into durable, higher quality earnings despite margin pressure and lumpy project work. The new Memory Optimization and Reclamation Assessment looks helpful for near term customer conversations but does not fundamentally change the biggest near term swing factors: mix driven margin pressure and exposure to large, non recurring enterprise deals.

The new memory assessment is the clearest tie to today’s AI driven supply constraints, aiming to help customers unlock capacity when new hardware is scarce or expensive. It aligns with ePlus’s focus on higher value services around AI infrastructure and could support the broader push toward more recurring, consultative relationships, which many investors are watching as a counterweight to project driven revenue volatility.

Yet against these potential benefits, investors should still pay attention to how exposed ePlus remains to large, one off enterprise projects and what that could mean if ...

Read the full narrative on ePlus (it's free!)

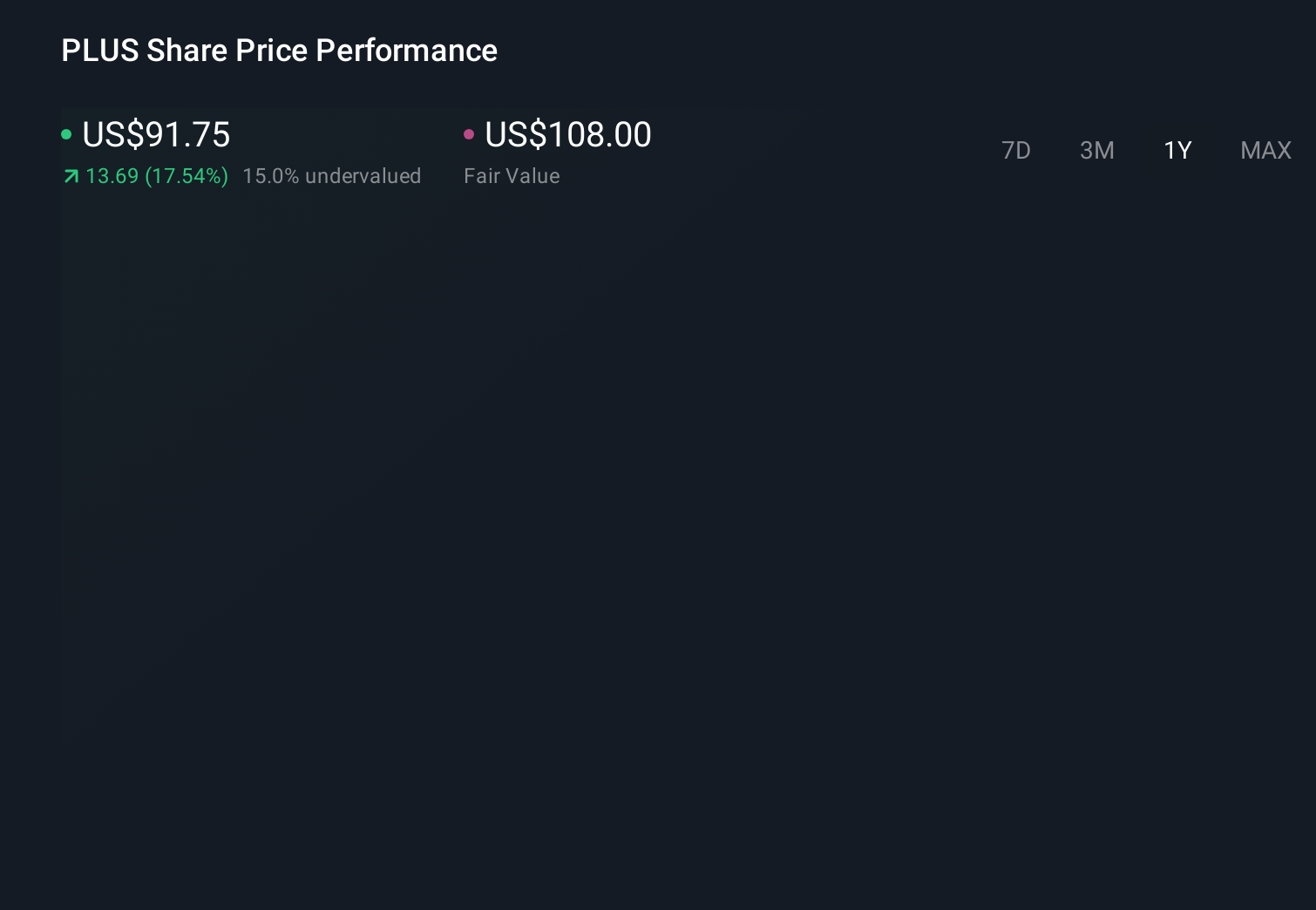

ePlus' narrative projects $2.8 billion revenue and $142.6 million earnings by 2029. This requires 5.4% yearly revenue growth and a $5.5 million earnings decrease from $148.1 million today.

Uncover how ePlus' forecasts yield a $115.00 fair value, a 35% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$96.89 to US$115, showing how far individual views on ePlus can diverge. You can set those against the current enthusiasm around AI infrastructure demand and ePlus’s memory optimization push to judge how resilient you think its earnings profile might be over time.

Explore 2 other fair value estimates on ePlus - why the stock might be worth as much as 35% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ePlus research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ePlus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ePlus' overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English