3 Asian Value Stocks Trading At Up To 49.1% Below Intrinsic Estimates

As geopolitical tensions in the Middle East show signs of easing, Asian markets are experiencing a cautious rebound, buoyed by optimism around diplomatic progress and solid economic data from China. In this environment, identifying undervalued stocks becomes essential for investors seeking opportunities amid fluctuating market sentiment.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| WuXi XDC Cayman (SEHK:2268) | HK$59.75 | HK$116.01 | 48.5% |

| Taiwan Surface Mounting Technology (TWSE:6278) | NT$158.50 | NT$315.57 | 49.8% |

| Softcare (SEHK:2698) | HK$29.38 | HK$58.01 | 49.4% |

| Premium Group (TSE:7199) | ¥1824.00 | ¥3636.44 | 49.8% |

| MicroPort Scientific (SEHK:853) | HK$9.44 | HK$18.25 | 48.3% |

| Lum Chang Creations (Catalist:LCC) | SGD1.00 | SGD1.96 | 49% |

| InSilico Medicine Cayman TopCo (SEHK:3696) | HK$68.35 | HK$134.33 | 49.1% |

| Hantech (KOSDAQ:A098070) | ₩43000.00 | ₩85055.24 | 49.4% |

| DIGITAL HEARTS HOLDINGS (TSE:3676) | ¥845.00 | ¥1631.79 | 48.2% |

| A-tieLtd (TSE:369A) | ¥2611.00 | ¥5085.28 | 48.7% |

Here we highlight a subset of our preferred stocks from the screener.

Bank of East Asia (SEHK:23)

Overview: The Bank of East Asia, Limited, along with its subsidiaries, offers a range of banking and financial services and has a market cap of HK$37.17 billion.

Operations: The company's revenue segments include Mainland China Operations (HK$3.53 billion), Overseas, Macau and Taiwan operations (HK$2.28 billion), Hong Kong Operations - Personal Banking (HK$6.87 billion), Treasury Markets (HK$1.62 billion), and Wealth Management (HK$1.31 billion).

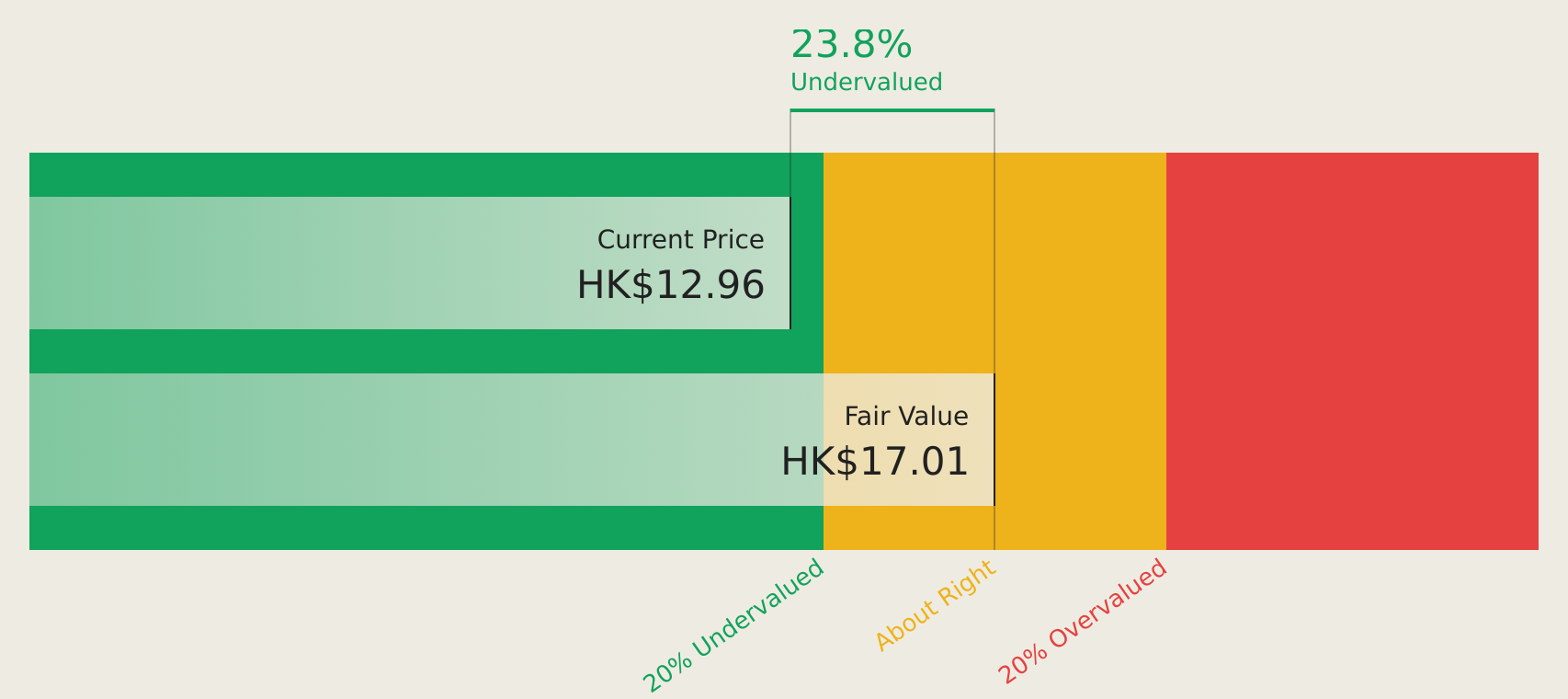

Estimated Discount To Fair Value: 20%

Bank of East Asia is trading at HK$14.06, below its estimated future cash flow value of HK$17.57, indicating potential undervaluation based on cash flows. Despite a forecasted low return on equity and high bad loan levels (2.7%), earnings are expected to grow significantly at 23.6% annually over the next three years, outpacing the Hong Kong market's growth rate of 12.5%. Recent debt management actions include redeeming USD 500 million notes, enhancing financial stability.

- The growth report we've compiled suggests that Bank of East Asia's future prospects could be on the up.

- Take a closer look at Bank of East Asia's balance sheet health here in our report.

InSilico Medicine Cayman TopCo (SEHK:3696)

Overview: InSilico Medicine Cayman TopCo is an AI-driven biotech company focused on developing and manufacturing novel drugs across Hong Kong, the United States, the United Kingdom, Mainland China, and internationally with a market cap of HK$39.12 billion.

Operations: The company's revenue from biotechnology is $56.24 million.

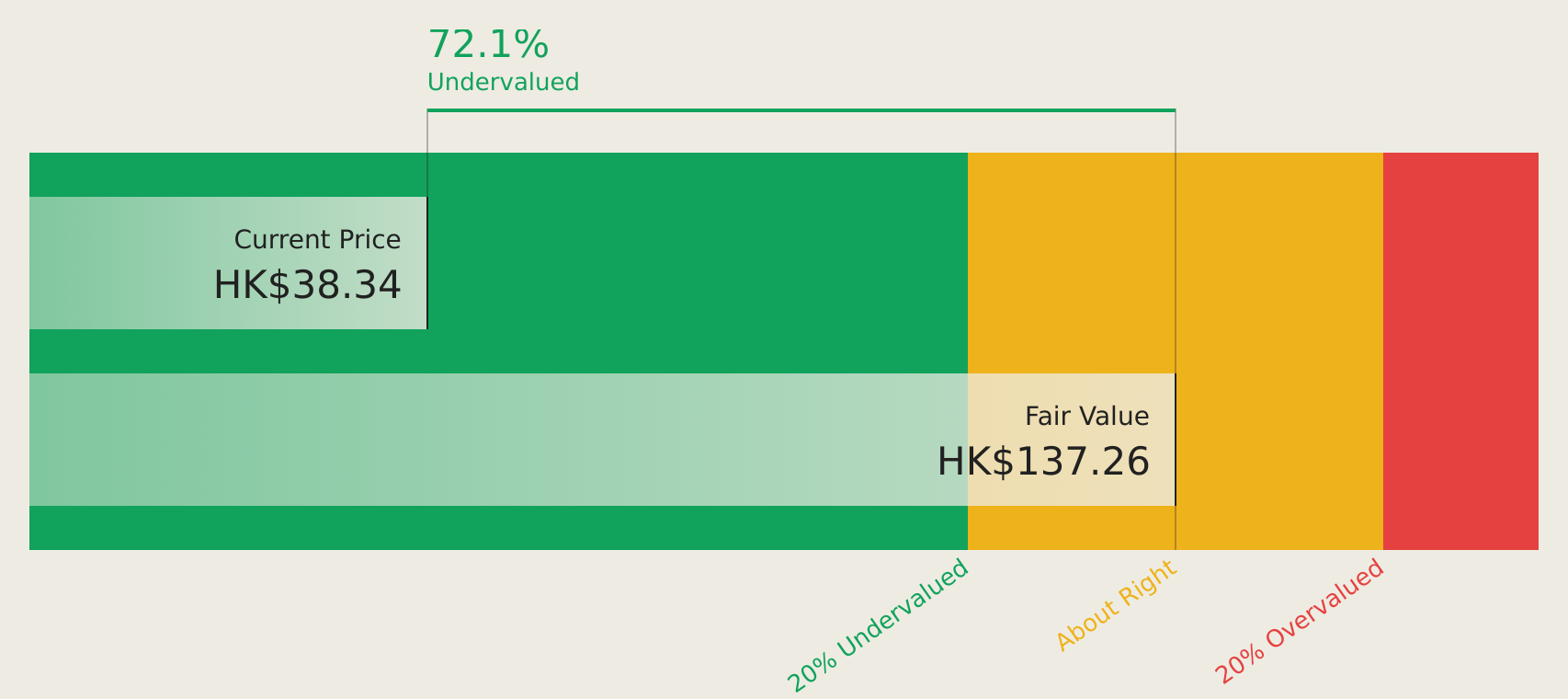

Estimated Discount To Fair Value: 49.1%

InSilico Medicine Cayman TopCo, trading at HK$68.35, is significantly undervalued based on cash flows with an estimated future value of HK$134.33. Despite a volatile share price and substantial net losses in 2025, the company is expected to become profitable within three years. Revenue growth forecasts exceed 43% annually, surpassing market averages. Recent collaborations and product advancements highlight its strategic focus on AI-driven drug discovery, potentially enhancing long-term financial performance despite current challenges.

- In light of our recent growth report, it seems possible that InSilico Medicine Cayman TopCo's financial performance will exceed current levels.

- Click here to discover the nuances of InSilico Medicine Cayman TopCo with our detailed financial health report.

MicroPort Scientific (SEHK:853)

Overview: MicroPort Scientific Corporation, along with its subsidiaries, is involved in the innovation, manufacturing, and marketing of medical devices across various regions including the People’s Republic of China, Europe, the Middle East and Africa, Japan, and internationally; it has a market cap of approximately HK$18.10 billion.

Operations: The company's revenue is derived from several segments, including Orthopedics Devices ($235.16 million), Cardiovascular Devices ($182.18 million), Surgical Robot Devices ($77.58 million), Structural Heart Disease ($51.31 million), Cardiac Rhythm Management (CRM) Business ($229.72 million), and Endovascular and Peripheral Vascular Devices Business ($189.48 million).

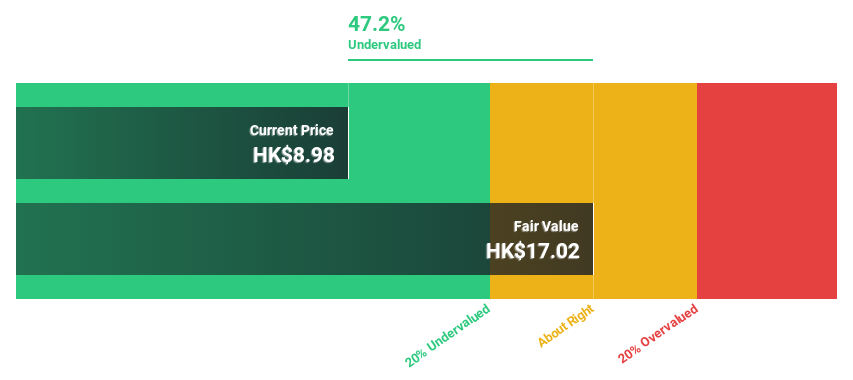

Estimated Discount To Fair Value: 48.3%

MicroPort Scientific, trading at HK$9.44, is highly undervalued with a cash flow-based estimate of HK$18.25. Despite a low forecasted return on equity and slower revenue growth than 20% annually, the company shows promising earnings growth potential at 92.06% per year and is expected to become profitable in three years. The recent international distribution agreements could enhance overseas market presence while strategic executive changes aim to boost global operations efficiency and resource synergies.

- Our expertly prepared growth report on MicroPort Scientific implies its future financial outlook may be stronger than recent results.

- Delve into the full analysis health report here for a deeper understanding of MicroPort Scientific.

Make It Happen

- Delve into our full catalog of 203 Undervalued Asian Stocks Based On Cash Flows here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English