Asian Growth Companies With Strong Insider Ownership In April 2026

As global markets respond positively to geopolitical developments and economic data, Asian markets are also experiencing a period of cautious optimism, supported by China's stronger-than-expected GDP growth and easing tensions in the Middle East. In this environment, growth companies with high insider ownership can be particularly appealing as they often exhibit alignment between management and shareholder interests, potentially enhancing their resilience and strategic focus amidst fluctuating market conditions.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Suzhou Dongshan Precision Manufacturing (SZSE:002384) | 33.5% | 78.8% |

| Streamax Technology (SZSE:002970) | 32.3% | 30.3% |

| Shanghai Biren Technology (SEHK:6082) | 11% | 121.5% |

| Seojin SystemLtd (KOSDAQ:A178320) | 23.7% | 109.2% |

| Modetour Network (KOSDAQ:A080160) | 12.3% | 61.6% |

| Meitu (SEHK:1357) | 22.7% | 32% |

| Laopu Gold (SEHK:6181) | 19% | 25.7% |

| Jiangxi Fushine Pharmaceutical (SZSE:300497) | 22.6% | 88.7% |

| Gold Circuit Electronics (TWSE:2368) | 30.5% | 36.8% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 46.1% |

Let's take a closer look at a couple of our picks from the screened companies.

Meitu (SEHK:1357)

Simply Wall St Growth Rating: ★★★★★★

Overview: Meitu, Inc. is an investment holding company focused on developing and providing AI-powered products for photo, video, and design production in Mainland China and internationally, with a market cap of approximately HK$20.77 billion.

Operations: The company generates revenue from its Internet Business segment, amounting to CN¥3.86 billion.

Insider Ownership: 22.7%

Earnings Growth Forecast: 32% p.a.

Meitu, Inc. demonstrates strong growth potential with its earnings projected to increase significantly over the next three years, outpacing the Hong Kong market. The company's revenue is also set to grow substantially, supported by a share repurchase program aimed at enhancing net asset value and earnings per share. Despite a decrease in net income for 2025, Meitu remains undervalued relative to its estimated fair value, suggesting room for potential appreciation as insider ownership aligns management interests with shareholders.

- Take a closer look at Meitu's potential here in our earnings growth report.

- In light of our recent valuation report, it seems possible that Meitu is trading beyond its estimated value.

Shanghai Forest Cabin Cosmetics Group (SEHK:2657)

Simply Wall St Growth Rating: ★★★★★★

Overview: Shanghai Forest Cabin Cosmetics Group Co., Ltd. operates in the cosmetics industry and has a market cap of approximately HK$8.68 billion.

Operations: The company's revenue is primarily derived from its Personal Products segment, which generated CN¥2.45 billion.

Insider Ownership: 35.6%

Earnings Growth Forecast: 31.3% p.a.

Shanghai Forest Cabin Cosmetics Group is experiencing significant growth, with revenue and earnings forecasted to rise substantially faster than the Hong Kong market. The company reported a strong financial performance for 2025, with sales reaching CNY 2.45 billion and net income at CNY 360.37 million. Despite recent board resignations, the company's focus on expanding its product portfolio and customer base continues to drive its competitive edge in the cosmetics industry.

- Unlock comprehensive insights into our analysis of Shanghai Forest Cabin Cosmetics Group stock in this growth report.

- Upon reviewing our latest valuation report, Shanghai Forest Cabin Cosmetics Group's share price might be too pessimistic.

Delijia Transmission Technology (Jiangsu)Ltd (SHSE:603092)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Delijia Transmission Technology (Jiangsu) Ltd, with a market cap of CN¥28.43 billion, operates in the transmission technology sector.

Operations: The company's revenue segments include various operations within the transmission technology sector.

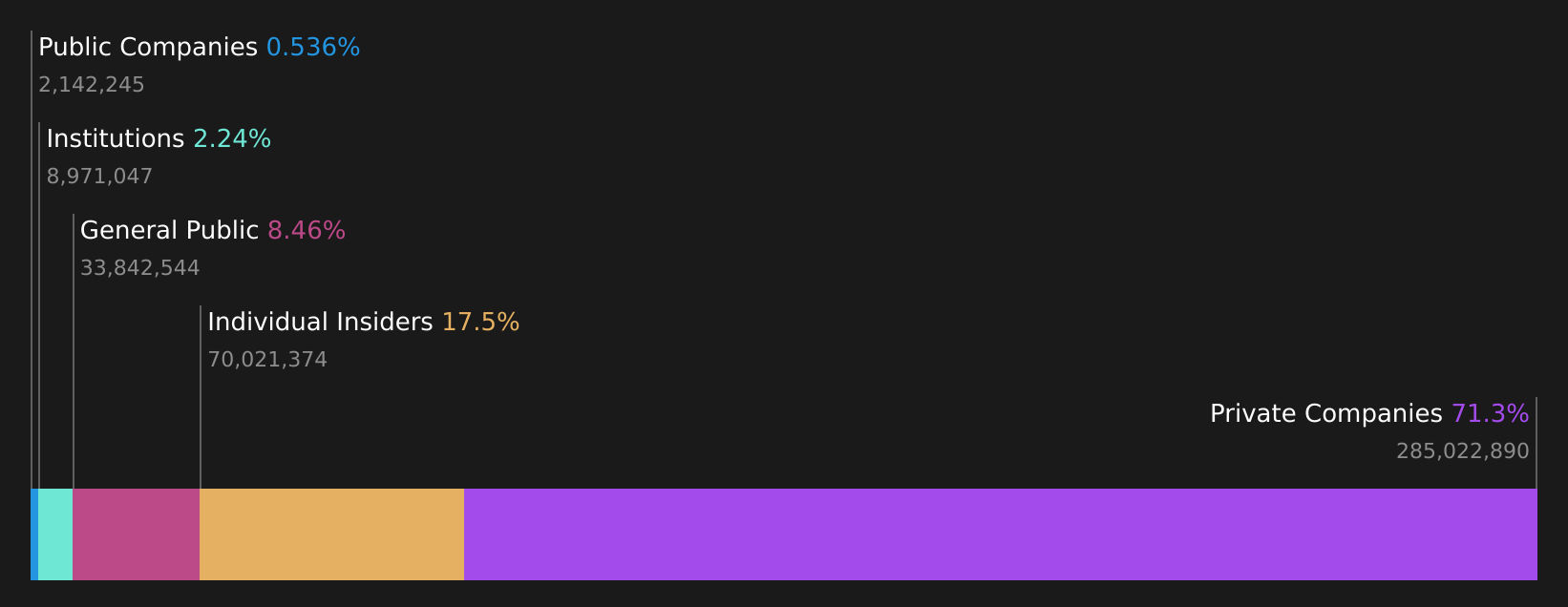

Insider Ownership: 17.5%

Earnings Growth Forecast: 23.3% p.a.

Delijia Transmission Technology (Jiangsu) Ltd. shows robust growth with its revenue rising to CNY 5.42 billion and net income reaching CNY 827.37 million in 2025, reflecting a significant earnings increase of 55%. The company's forecasted annual profit growth of over 23% aligns with its high insider ownership, suggesting confidence in long-term prospects. While its price-to-earnings ratio is lower than the market average, revenue growth outpaces market expectations at over 21% annually.

- Get an in-depth perspective on Delijia Transmission Technology (Jiangsu)Ltd's performance by reading our analyst estimates report here.

- Our comprehensive valuation report raises the possibility that Delijia Transmission Technology (Jiangsu)Ltd is priced higher than what may be justified by its financials.

Seize The Opportunity

- Access the full spectrum of 523 Fast Growing Asian Companies With High Insider Ownership by clicking on this link.

- Curious About Other Options? The end of cancer? These 31 emerging AI stocks are developing tech that will allow early idenification of life changing disesaes like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English