3 Asian Stocks Estimated To Be Up To 31.8% Below Intrinsic Value

As global markets navigate geopolitical tensions and economic uncertainties, Asian equities have shown resilience, with some indices maintaining stability amid fluctuating conditions. In this environment, identifying undervalued stocks can offer opportunities for investors seeking to capitalize on potential market inefficiencies. Recognizing a good stock often involves assessing its intrinsic value relative to its current price, especially in regions like Asia where emerging economic trends may present unique investment prospects.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| SHIFT (TSE:3697) | ¥656.20 | ¥1288.98 | 49.1% |

| Shenzhen Yanmade Technology (SHSE:688312) | CN¥70.07 | CN¥138.86 | 49.5% |

| Rayhoo Motor DiesLtd (SZSE:002997) | CN¥29.98 | CN¥58.21 | 48.5% |

| Premium Group (TSE:7199) | ¥1842.00 | ¥3672.79 | 49.8% |

| Paradise Entertainment (SEHK:1180) | HK$0.70 | HK$1.38 | 49.4% |

| NexTone (TSE:7094) | ¥1467.00 | ¥2898.17 | 49.4% |

| JAC Recruitment (TSE:2124) | ¥862.00 | ¥1694.20 | 49.1% |

| Inner Mongolia Xingye Silver & Tin Mining (SZSE:000426) | CN¥42.38 | CN¥84.03 | 49.6% |

| HD-Hyundai Marine Engine (KOSE:A071970) | ₩105800.00 | ₩211155.63 | 49.9% |

| DIGITAL HEARTS HOLDINGS (TSE:3676) | ¥832.00 | ¥1642.52 | 49.3% |

Let's review some notable picks from our screened stocks.

Innovent Biologics (SEHK:1801)

Overview: Innovent Biologics, Inc. is a biopharmaceutical company focused on the research and development of antibody and protein medicine products in China, the United States, and internationally, with a market cap of approximately HK$156.17 billion.

Operations: The company's revenue is primarily derived from its biotechnology segment, which generated CN¥13.04 billion.

Estimated Discount To Fair Value: 31.8%

Innovent Biologics appears undervalued based on cash flow analysis, trading at HK$90, below its estimated future cash flow value of HK$131.92. Analysts forecast significant earnings growth of 30.8% annually, surpassing the Hong Kong market average. Recent financials show a shift from a net loss to a CNY 813.57 million profit in 2025, alongside substantial revenue growth to CNY 13 billion. The company is advancing innovative treatments like IBI3055 and expanding its collaboration with Eli Lilly for global development.

- Upon reviewing our latest growth report, Innovent Biologics' projected financial performance appears quite optimistic.

- Click to explore a detailed breakdown of our findings in Innovent Biologics' balance sheet health report.

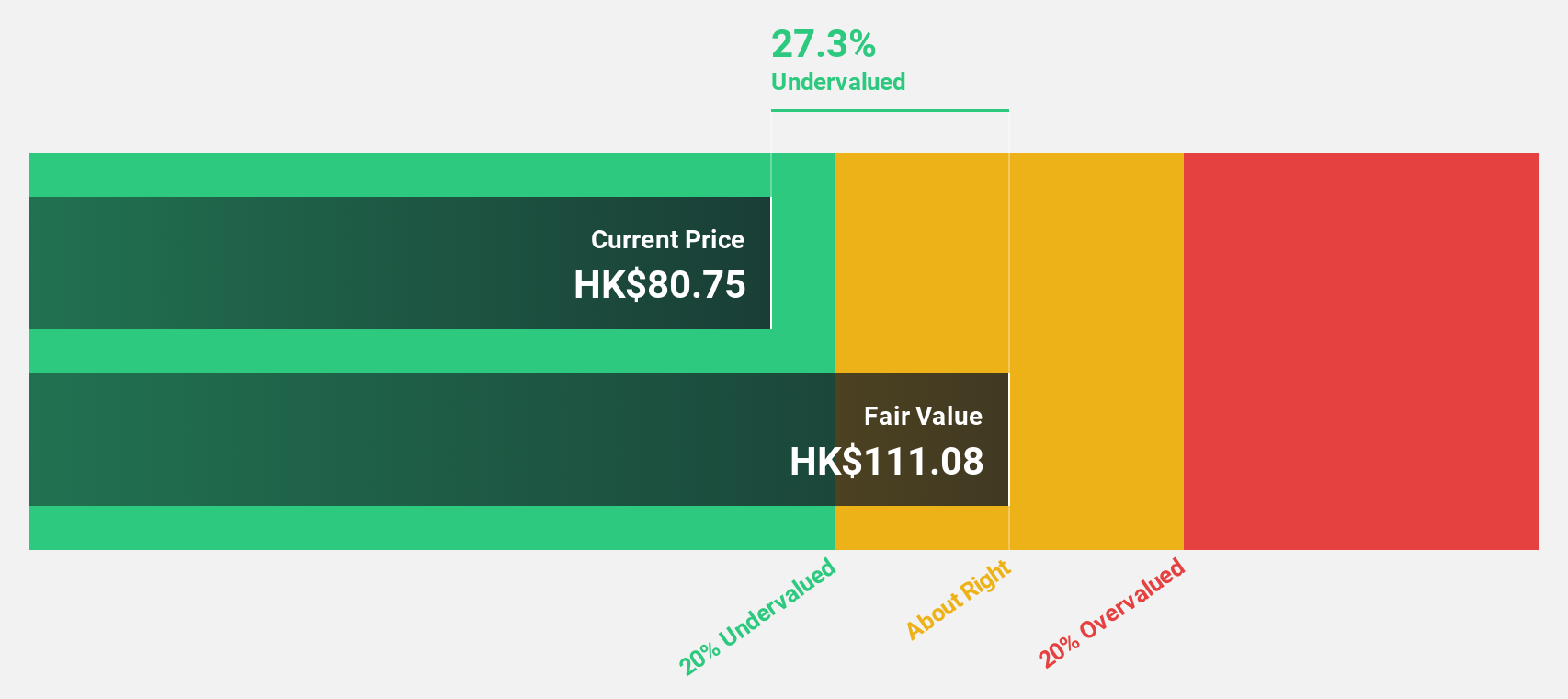

Akeso (SEHK:9926)

Overview: Akeso, Inc. is a biopharmaceutical company involved in the research, development, manufacture, and commercialization of antibody drugs globally, with a market cap of approximately HK$125.09 billion.

Operations: The company generates CN¥3.06 billion from its activities in the research, development, production, and sale of biopharmaceutical products.

Estimated Discount To Fair Value: 25.2%

Akeso is trading at HK$135.8, significantly below its estimated future cash flow value of HK$181.63, suggesting it may be undervalued based on cash flows. The company's earnings are projected to grow 46.81% annually, with revenue expected to expand by 29.1% per year, outpacing the Hong Kong market average. Recent advancements in its bispecific antibodies like ivonescimab and cadonilimab highlight Akeso's strong position in innovative oncology treatments despite current net losses increasing to CNY 1.11 billion in 2025 from the previous year.

- Our growth report here indicates Akeso may be poised for an improving outlook.

- Click here to discover the nuances of Akeso with our detailed financial health report.

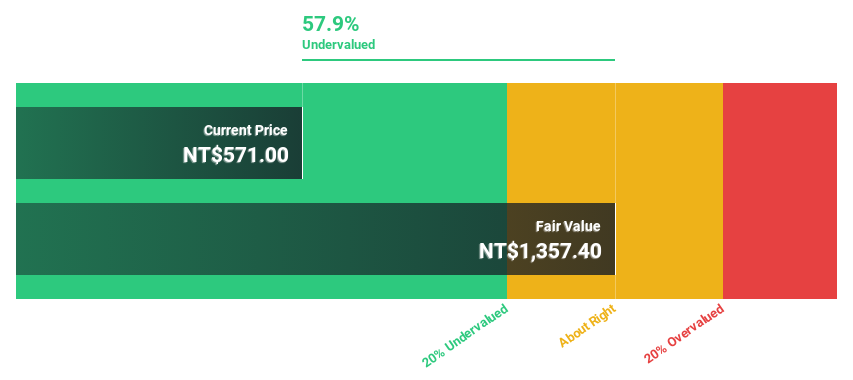

Elite Material (TWSE:2383)

Overview: Elite Material Co., Ltd. manufactures and sells copper clad laminates, electronic-industrial specialty chemicals, raw materials, and electronic components in Taiwan, China, and internationally with a market cap of NT$1.63 trillion.

Operations: The company's revenue is derived from the manufacturing and sales of copper clad laminates, electronic-industrial specialty chemicals and raw materials, as well as electronic components across Taiwan, China, and international markets.

Estimated Discount To Fair Value: 15.2%

Elite Material's recent earnings report shows strong financial performance with first-quarter sales of TWD 33.07 billion and net income of TWD 5.34 billion, reflecting significant growth from the previous year. Despite high share price volatility, the stock trades at NT$4,545, below its future cash flow value of NT$5,361.89. Forecasts indicate robust annual earnings growth of 47.44% and revenue expansion at 42%, outpacing Taiwan's market averages, underscoring potential undervaluation based on cash flows.

- The growth report we've compiled suggests that Elite Material's future prospects could be on the up.

- Unlock comprehensive insights into our analysis of Elite Material stock in this financial health report.

Make It Happen

- Investigate our full lineup of 211 Undervalued Asian Stocks Based On Cash Flows right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English