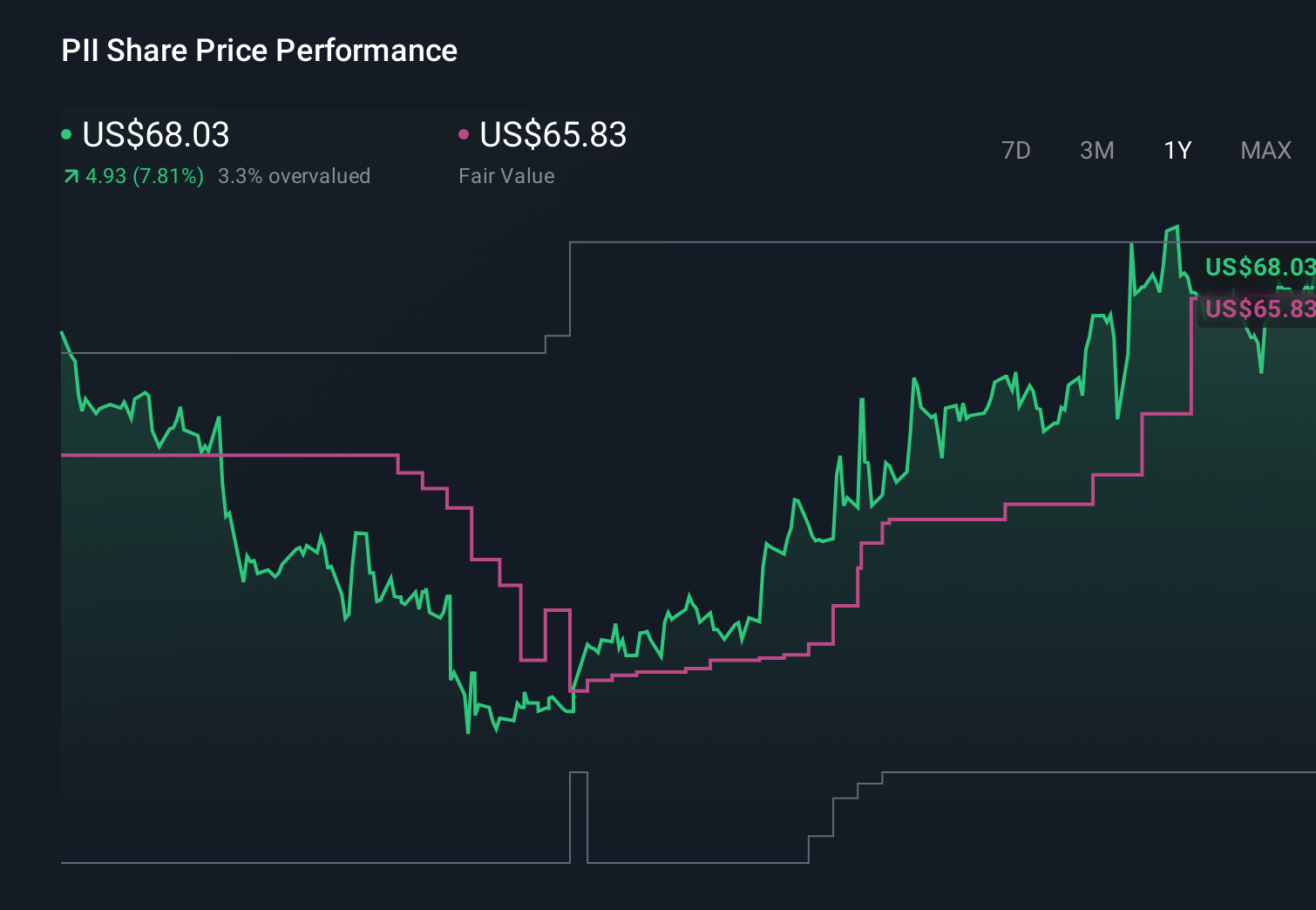

Polaris (PII) Is Up 10.6% After Margin Gains Offset Tariffs In Q1 2026 - Has The Bull Case Changed?

- Polaris Inc. reported past first-quarter 2026 results with sales rising to US$1,658.7 million from US$1,535.8 million, while narrowing its net loss to US$47.4 million from US$66.8 million and reducing loss per share from US$1.17 to US$0.83.

- The quarter also showed an 8% revenue increase, gross margin expansion despite tariff pressures, and double-digit growth in key utility and commercial powersports lines, highlighting underlying operational improvements.

- We’ll now examine how Polaris’s stronger-than-expected margins despite tariff headwinds may influence its pre-existing investment narrative and risk profile.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Polaris Investment Narrative Recap

To own Polaris, you need to believe its core powersports franchises and product pipeline can justify riding out current losses, tariff costs, and a choppy consumer backdrop. The latest quarter’s stronger gross margins and utility-focused growth support the view that tariff mitigation and operational efficiency are the key near term catalysts, while the biggest ongoing risk remains policy and demand uncertainty that could still pressure volumes and keep the business under-earning.

Against that backdrop, the recent 2% dividend increase to US$0.68 per share stands out. It signals continued capital returns even as Polaris absorbs tariff headwinds and reports net losses, which some shareholders may view as reinforcing confidence in cash generation. Whether that dividend track record can sit comfortably alongside the current earnings pressure and high tariff costs will be an important test of the bullish margin improvement story.

But behind the margin progress, the unresolved tariff exposure and its potential drag on future earnings is something investors should be aware of as...

Read the full narrative on Polaris (it's free!)

Polaris' narrative projects $7.8 billion revenue and $438.0 million earnings by 2029. This requires 2.2% yearly revenue growth and an $884.1 million earnings increase from -$446.1 million today.

Uncover how Polaris' forecasts yield a $66.00 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Polaris could lift revenue to about US$8.0 billion and earnings to roughly US$376 million, yet this quarter’s margin resilience and ongoing tariff and electrification risks show just how far apart views can be, and why it helps to compare these upbeat expectations with more cautious scenarios before deciding which version of the story you find more convincing.

Explore 3 other fair value estimates on Polaris - why the stock might be worth just $66.00!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Polaris research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 37 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English