Undervalued Small Caps With Insider Buying Opportunities In May 2026

The United States market has shown robust performance recently, with a 3.2% increase over the last week and a remarkable 31% rise over the past year, while earnings are expected to grow by 16% annually. In this thriving environment, identifying small-cap stocks that may be undervalued and exhibit insider buying can present unique opportunities for investors seeking potential growth in their portfolios.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| First United | 9.5x | 2.7x | 47.59% | ★★★★★☆ |

| Financial Institutions | 9.0x | 2.9x | 31.46% | ★★★★★☆ |

| Ferroglobe | NA | 0.6x | 45.75% | ★★★★★☆ |

| Ribbon Communications | 15.0x | 0.6x | 32.80% | ★★★★★☆ |

| Metropolitan Bank Holding | 13.0x | 3.7x | 39.45% | ★★★★☆☆ |

| PCB Bancorp | 8.8x | 3.0x | 17.70% | ★★★★☆☆ |

| German American Bancorp | 12.1x | 4.4x | 44.26% | ★★★☆☆☆ |

| Bank of Marin Bancorp | NA | 11.7x | 33.40% | ★★★☆☆☆ |

| New Peoples Bankshares | 9.7x | 2.3x | 23.07% | ★★★☆☆☆ |

| Aldeyra Therapeutics | NA | NA | 45.67% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

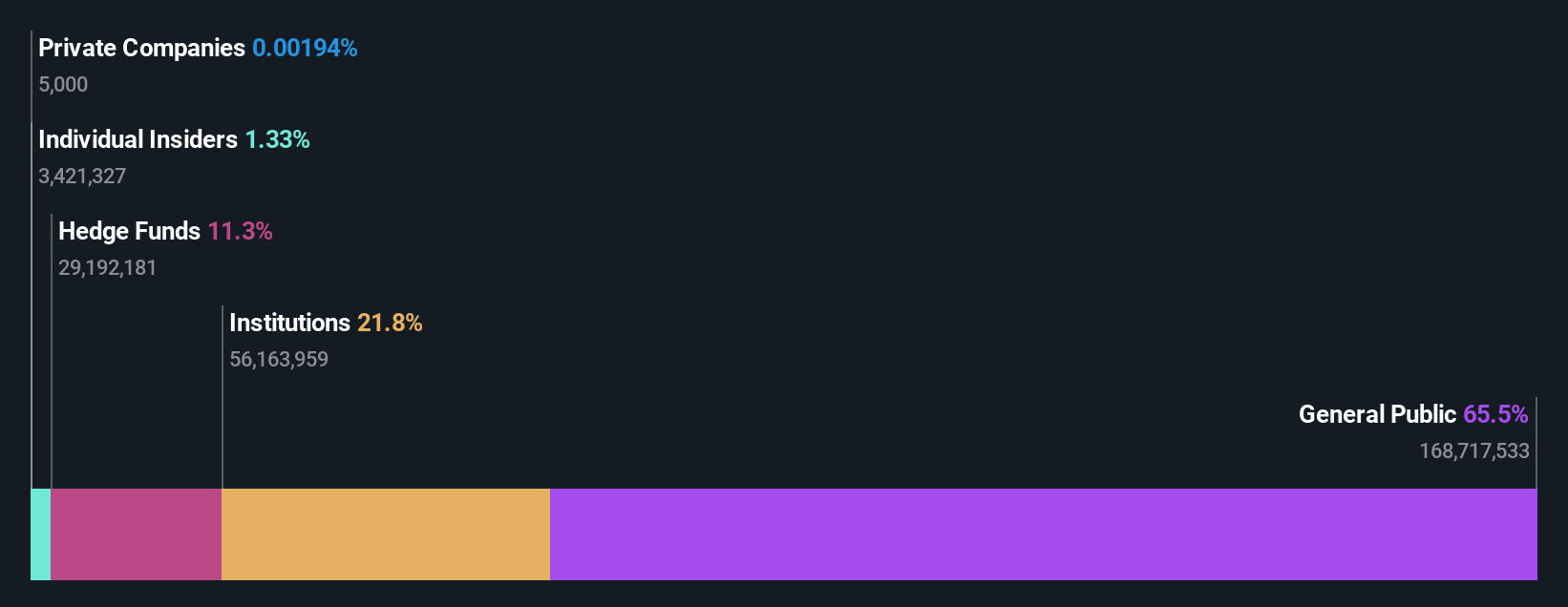

SNDL (SNDL)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: SNDL is a Canadian company engaged in the production and retail of cannabis products, with a market cap of approximately CA$1.45 billion.

Operations: SNDL's revenue has shown significant growth, reaching CA$951.58 million by September 2025, with a gross profit margin of 27.13%. The cost of goods sold (COGS) was CA$694.36 million in the same period, indicating a substantial portion of revenue is absorbed by production costs. Operating expenses include significant general and administrative costs, which were CA$202.03 million as of September 2025. Despite increasing revenues and gross profit margins over time, the company reported a net income loss of CA$92.28 million for the same quarter, reflecting ongoing financial challenges in achieving profitability.

PE: -46.4x

SNDL, a cannabis-focused company, recently reported first-quarter 2026 sales of CAD 195.91 million with a net loss reduced to CAD 9.91 million from the previous year. Despite the unprofitable status and reliance on external funding, they show insider confidence through share repurchases of over 4 million shares for CAD 8.85 million between November 2025 and March 2026. Leadership changes may impact strategy as they navigate these challenges in pursuit of growth within their industry segment.

- Take a closer look at SNDL's potential here in our valuation report.

Evaluate SNDL's historical performance by accessing our past performance report.

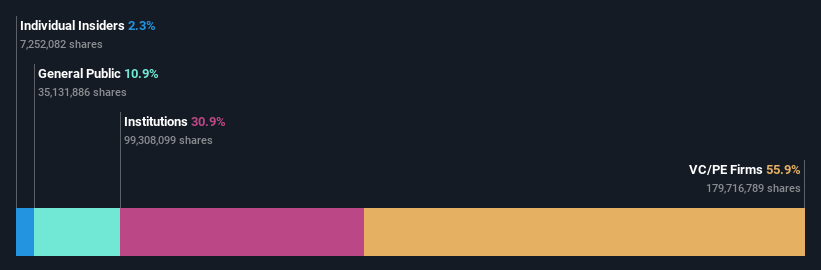

Advantage Solutions (ADV)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Advantage Solutions is a provider of outsourced sales and marketing services to consumer goods companies and retailers, with a market cap of approximately $1.13 billion.

Operations: Advantage Solutions generates revenue primarily through its services, with a notable gross profit margin of 14.02% as of March 2026. The company incurs significant costs, including cost of goods sold (COGS) and operating expenses, which impact its profitability. Over recent periods, the net income has shown negative margins, reflecting challenges in managing non-operating expenses and overall financial performance.

PE: -2.3x

Advantage Solutions, a player in the U.S. market with fluctuating share prices over the past three months, faces challenges with profitability and relies on higher-risk external borrowing for funding. Despite these hurdles, insider confidence is evident as David Peacock purchased 8,000 shares in April 2026 for US$128,780. The company recently underwent a reverse stock split and anticipates flat to low single-digit revenue growth in 2026. Leadership changes aim to drive growth and innovation amidst industry shifts.

- Click to explore a detailed breakdown of our findings in Advantage Solutions' valuation report.

Understand Advantage Solutions' track record by examining our Past report.

Tecnoglass (TGLS)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Tecnoglass is a company that specializes in the manufacturing and distribution of architectural glass and windows, with a market capitalization of approximately $2.25 billion.

Operations: The primary revenue stream comes from the Architectural Glass and Windows segment, generating $983.61 million. The gross profit margin has shown an upward trend, reaching 50.59% in Q1 2023 before slightly decreasing to 42.84% by the end of 2025. Operating expenses have consistently increased over time, with notable components including sales and marketing expenses and general & administrative costs.

PE: 12.4x

Tecnoglass, operating in the glass and window industry, is a small cap stock showing potential for value appreciation. Despite relying on external borrowing for funding, insider confidence is evident with recent share purchases. The company projects revenue growth between US$1.06 billion and US$1.13 billion in 2026, an 11% increase at midpoint. Recent buybacks of over 3 million shares suggest management's belief in its value proposition. With earnings set to grow annually by nearly 4%, Tecnoglass presents intriguing prospects amidst market dynamics.

- Delve into the full analysis valuation report here for a deeper understanding of Tecnoglass.

Gain insights into Tecnoglass' past trends and performance with our Past report.

Seize The Opportunity

- Delve into our full catalog of 64 Undervalued US Small Caps With Insider Buying here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English