A Look At China National Building Material's Valuation After Q1 2026 Results And Lower Final Dividend Approval

China National Building Material (SEHK:3323) has just reported first quarter 2026 results alongside AGM approvals that include a lower final cash dividend and a fresh mandate to issue additional shares.

See our latest analysis for China National Building Material.

The recent AGM decisions and first quarter 2026 loss reduction have coincided with a sharp short term rebound, with a 20.41% 1 month share price return and a 63.35% 1 year total shareholder return. However, the 5 year total shareholder return remains negative at 19.34%, suggesting momentum has improved but long term holders are still underwater.

If this mix of near term recovery and longer term mixed results has you thinking about other opportunities, it could be a good moment to check out 8 top copper producer stocks

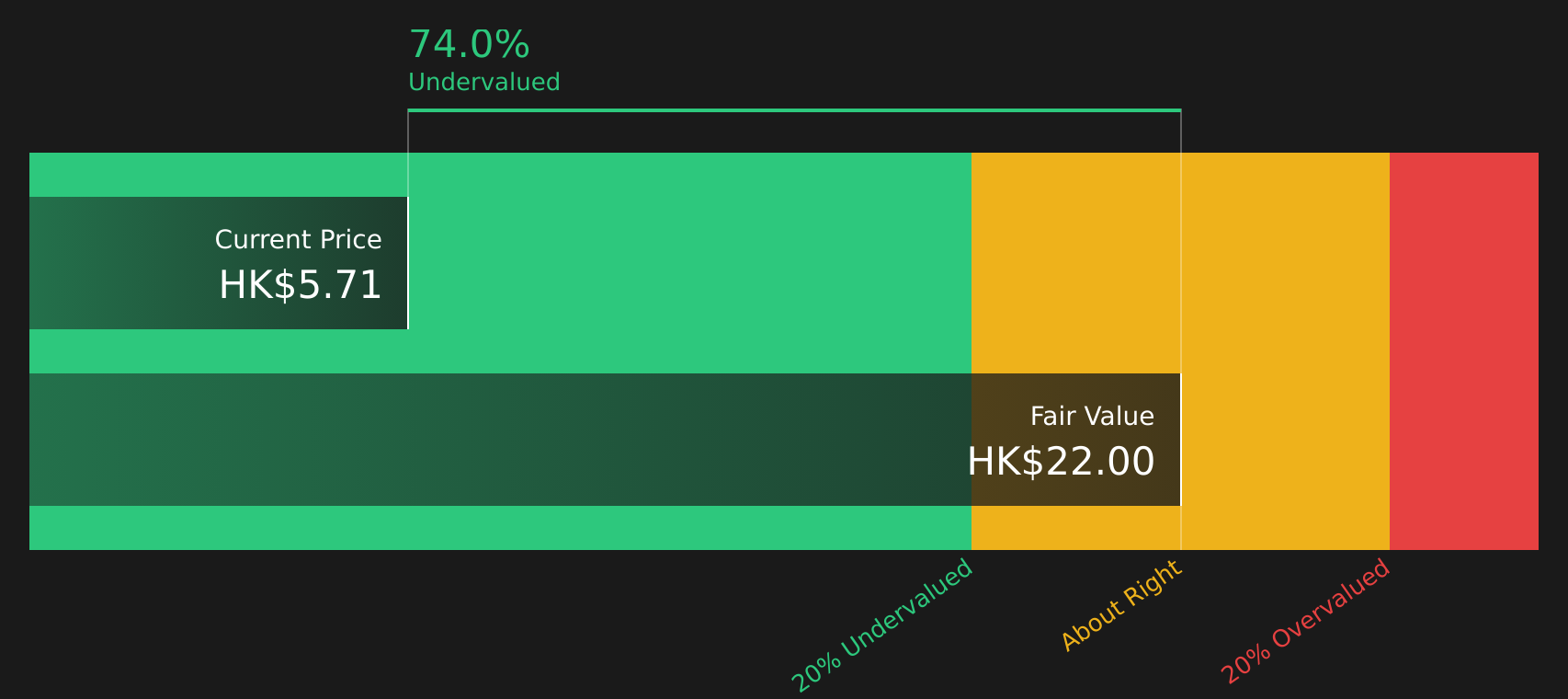

So with the stock trading at HK$5.84, a sizeable intrinsic discount indicated and a strong recent rebound after years of weak total returns, is there still a buying opportunity here, or is the market already pricing in future growth?

Preferred Multiple of 0.2x P/S: Is it justified?

On a P/S of 0.2x at a HK$5.84 share price, China National Building Material screens as inexpensive compared with both its peers and its own implied fair level.

The P/S ratio compares the company’s market value to its revenue, which can be useful when earnings are negative or volatile, as is the case here. With China National Building Material currently loss making yet generating HK$177,847.09m of revenue, investors are effectively paying a relatively low amount for each unit of sales compared with similar Hong Kong basic materials stocks.

Relative to the Hong Kong Basic Materials industry average P/S of 0.7x, the stock’s 0.2x multiple is far lower. This implies the market is pricing in weaker prospects or higher risk than for peers. Against the estimated fair P/S of 0.7x, it also trades well below the level the SWS fair ratio model suggests the market could gravitate toward if sentiment and fundamentals align more closely.

Explore the SWS fair ratio for China National Building Material

Result: Price-to-Sales of 0.2x (UNDERVALUED)

However, investors still face risks, including the recent HK$3,745.26m net loss and heavy reliance on PRC revenue at HK$145,448.51m, which could pressure sentiment.

Find out about the key risks to this China National Building Material narrative.

Another View: What Does The DCF Say?

While the low 0.2x P/S points to value on sales, the SWS DCF model indicates an estimated future cash flow value of HK$21.94 compared to the current HK$5.84 price. That is a very wide gap, so is the discount a genuine opportunity or a sign of higher risk?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out China National Building Material for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 222 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals on value and risk so far. If you want to act while sentiment is shifting, take a closer look at the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that fit your goals and risk comfort. Use screeners to widen your net confidently.

- Spot potential mispriced opportunities early by scanning screener containing 545 high quality undiscovered gems before the crowd catches on.

- Strengthen your income focus by reviewing 486 dividend fortresses that aim to combine higher yields with stability.

- Prioritise resilience by checking 309 resilient stocks with low risk scores that score well on risk while still offering upside potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English