Does VinFast’s Record 2025 EV and E‑Scooter Deliveries Change The Bull Case For VinFast Auto (VFS)?

- In 2025, VinFast Auto more than doubled its electric vehicle deliveries to 196,919 units and lifted e-scooter and e-bike deliveries to 406,498, surpassing its own guidance.

- This surge across both four-wheel and two-wheel segments, combined with a global 2026 EV delivery goal of 300,000 units, highlights how VinFast is scaling an integrated electric ecosystem rather than relying on a single product line.

- Now we’ll examine how this record delivery performance, especially in e-scooters and e-bikes, could influence VinFast Auto’s broader investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

VinFast Auto Investment Narrative Recap

To own VinFast Auto, you need to believe it can convert rapid volume growth across cars, e scooters and e bikes into a sustainable global business, despite ongoing heavy losses and liquidity pressure. The latest delivery beat supports the growth side of that equation, but it does not yet resolve the most immediate concern around high cash burn and the potential need for future funding, which remains the key near term risk for shareholders.

The company’s 2026 guidance for 300,000 EV deliveries and at least 2.5 times growth in two wheelers is the clearest recent announcement linked to this record year. It connects directly to the delivery momentum just reported, while also setting a high execution bar: VinFast now has to prove it can hit these targets without worsening already negative margins and cash flows, which are central to the current investment case.

Yet investors should also weigh how this rapid growth interacts with VinFast’s limited cash runway and the risk of future dilution that may...

Read the full narrative on VinFast Auto (it's free!)

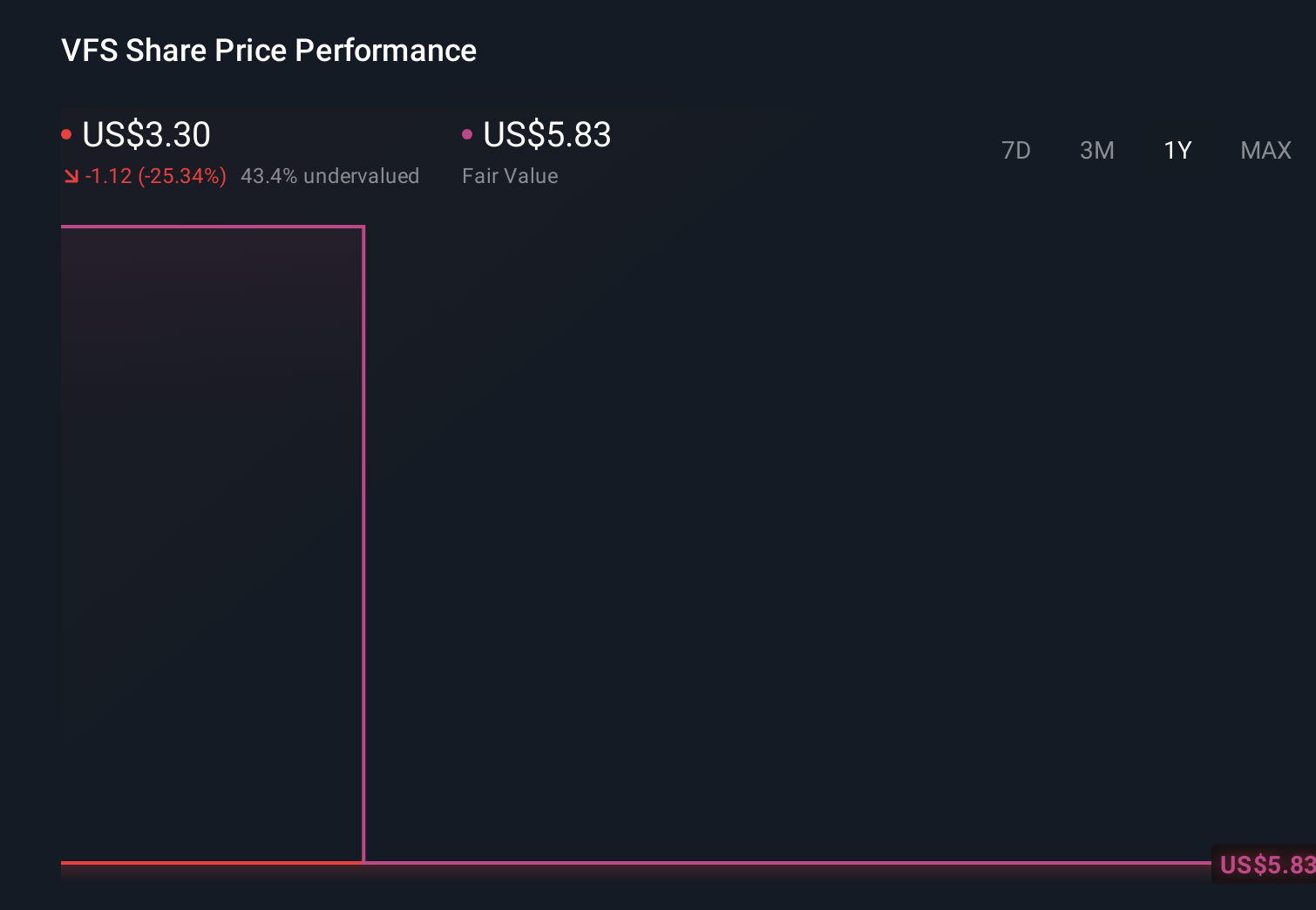

VinFast Auto's narrative projects ₫239,006.9 billion revenue and ₫5,494.0 billion earnings by 2029. This requires 38.3% yearly revenue growth and an earnings increase of about ₫102,536.0 billion from -₫97,041.9 billion today.

Uncover how VinFast Auto's forecasts yield a $6.30 fair value, a 48% upside to its current price.

Exploring Other Perspectives

The highest estimate analysts were already assuming about 41% annual revenue growth and earnings of roughly ₫9,301.1 billion by 2028, so this delivery surge could either support that optimistic view or expose how ambitious it really is, especially if executing on two wheeler expansion proves harder than expected.

Explore 5 other fair value estimates on VinFast Auto - why the stock might be a potential multi-bagger!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your VinFast Auto research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free VinFast Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate VinFast Auto's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 33 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English