Asian Stocks That May Be Undervalued In May 2026

As of early May 2026, Asian markets have shown signs of resilience, with Chinese equities advancing and Japanese indices reaching record highs amid positive sentiment around AI-related demand and easing geopolitical tensions. Amidst this backdrop, investors often seek undervalued stocks that may offer potential opportunities for growth, particularly in sectors demonstrating robust domestic demand or technological innovation.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Yurtec (TSE:1934) | ¥2502.00 | ¥4969.66 | 49.7% |

| TOKYO BASELtd (TSE:3415) | ¥376.00 | ¥751.84 | 50% |

| Shenzhen Dynanonic (SZSE:300769) | CN¥78.96 | CN¥156.07 | 49.4% |

| Pourin Special Welding Technology (SZSE:301468) | CN¥60.65 | CN¥119.34 | 49.2% |

| Plus Alpha ConsultingLtd (TSE:4071) | ¥2347.00 | ¥4675.04 | 49.8% |

| NexTone (TSE:7094) | ¥1527.00 | ¥3030.24 | 49.6% |

| Korea Circuit (KOSE:A007810) | ₩102200.00 | ₩200569.34 | 49% |

| Intco Medical Technology (SZSE:300677) | CN¥50.92 | CN¥100.44 | 49.3% |

| Info-Tech Systems (SGX:ITS) | SGD0.985 | SGD1.92 | 48.7% |

| Dajin Heavy IndustryLtd (SZSE:002487) | CN¥82.98 | CN¥160.59 | 48.3% |

Here's a peek at a few of the choices from the screener.

East Buy Holding (SEHK:1797)

Overview: East Buy Holding Limited is an investment holding company engaged in livestreaming e-commerce for private label product sales in China, with a market cap of HK$28.95 billion.

Operations: The company's revenue primarily comes from its online live commerce business, generating CN¥4.52 billion.

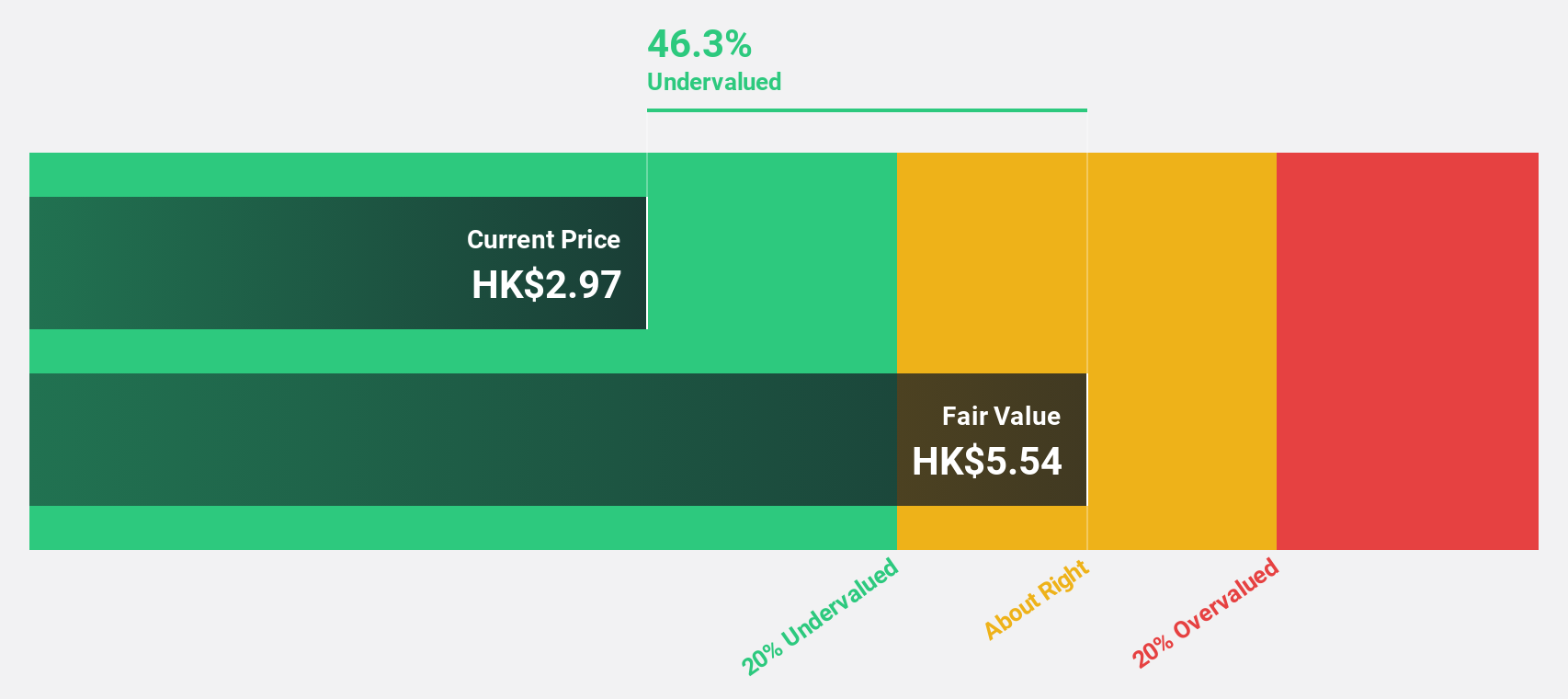

Estimated Discount To Fair Value: 10.1%

East Buy Holding is trading at HK$27.32, below its estimated future cash flow value of HK$30.39, indicating it may be undervalued based on cash flows. The company recently became profitable and is forecast to achieve significant earnings growth of 24.7% annually over the next three years, outpacing the Hong Kong market's average growth rate. However, its Return on Equity is expected to remain low at 9% in three years' time.

- The growth report we've compiled suggests that East Buy Holding's future prospects could be on the up.

- Delve into the full analysis health report here for a deeper understanding of East Buy Holding.

Tongguan Gold Group (SEHK:340)

Overview: Tongguan Gold Group Limited is an investment holding company involved in the exploration, mining, processing, smelting, and sale of gold and related products in China with a market cap of HK$16.47 billion.

Operations: The company generates revenue primarily from its gold mining operations, amounting to HK$2.40 billion.

Estimated Discount To Fair Value: 16.2%

Tongguan Gold Group is trading at HK$3.1, below its estimated cash flow value of HK$3.7, which may suggest undervaluation. The company reported significant earnings growth with net income reaching HK$830.43 million from HK$211.14 million a year ago and forecasts indicate continued strong earnings and revenue growth over the next three years, outpacing the Hong Kong market average. However, shareholders experienced dilution in the past year.

- Our earnings growth report unveils the potential for significant increases in Tongguan Gold Group's future results.

- Take a closer look at Tongguan Gold Group's balance sheet health here in our report.

Fibocom Wireless (SZSE:300638)

Overview: Fibocom Wireless Inc., along with its subsidiaries, offers wireless communication modules and artificial intelligence solutions both in China and internationally, with a market cap of CN¥19.28 billion.

Operations: Fibocom Wireless Inc. generates revenue through its wireless communication modules and artificial intelligence solutions, serving both domestic and international markets.

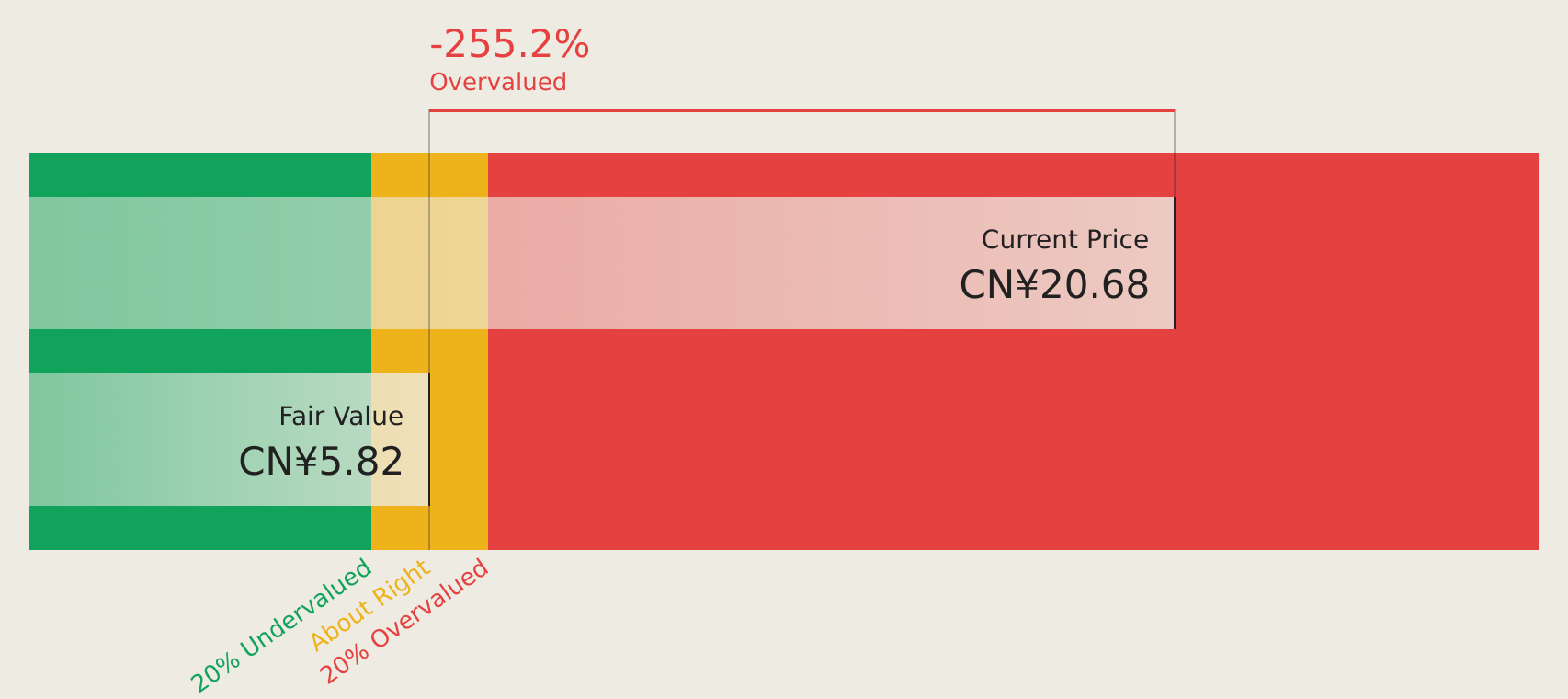

Estimated Discount To Fair Value: 42%

Fibocom Wireless is trading at CN¥23.51, significantly below its estimated cash flow value of CN¥40.52, highlighting potential undervaluation. Despite a challenging year with decreased revenue and net income, the company anticipates robust earnings growth of 38.9% annually over the next three years, surpassing market averages in China. Analysts expect a 23.4% stock price increase, although recent shareholder dilution and declining profit margins present challenges to consider.

- Upon reviewing our latest growth report, Fibocom Wireless' projected financial performance appears quite optimistic.

- Get an in-depth perspective on Fibocom Wireless' balance sheet by reading our health report here.

Summing It All Up

- Investigate our full lineup of 197 Undervalued Asian Stocks Based On Cash Flows right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English