A Look At Helix Energy Solutions (HLX) Valuation After Recent Share Price Pullback And Strong Year To Date Gains

Recent share performance and business snapshot

Helix Energy Solutions Group (HLX) has drawn fresh investor attention after a period of mixed trading, with the stock down 1.7% over the past day and 5.8% over the past week.

Despite that pullback, the shares are up slightly over the past month and have gained 14.2% in the past 3 months, with a year to date return of 50.9% and a 1 year total return of 41%.

The company reports annual revenue of US$1.30b and net income of US$14.33m, with recent annual revenue and net income growth rates of 2.9% and 22.4% respectively.

Helix Energy Solutions Group operates across four segments: Well Intervention, Robotics, Shallow Water Abandonment, and Production Facilities, providing a range of offshore services from well work and subsea robotics to decommissioning and processing.

At a last close of US$9.66 and a market value of about US$1.42b, the stock currently carries a value score of 2, with an indicated intrinsic discount of 34.8% based on available estimates.

See our latest analysis for Helix Energy Solutions Group.

Recent trading has cooled slightly, with the share price down 1.7% over the past day and 5.8% over the past week. However, the 90 day share price return of 14.2% and year to date gain of 50.9% indicate momentum that contrasts with a 1 year total shareholder return of 41%.

If you are weighing Helix against other opportunities in the energy and infrastructure space, it can help to see what else is moving, starting with 36 power grid technology and infrastructure stocks

With Helix trading at US$9.66 against a US$12.50 analyst target and an indicated intrinsic discount of 34.8%, the key question is simple: is this a genuine value gap, or is the market already pricing in future growth?

Most Popular Narrative: 1% Undervalued

Helix's most followed narrative puts fair value at $9.75, just above the last close at $9.66. The focus is on whether that small gap is justified by the long term story rather than a quick rerating.

The pronounced long-term uptick in global demand for well abandonment, decommissioning, and offshore maintenance (as more aging fields require regulatory-compliant retirement) will expand Helix's core addressable market, supporting durable revenue growth, backlog expansion, and reduced earnings volatility.

Want to see what is built into that fair value number? The narrative leans heavily on steady revenue progress, fatter margins, and a richer earnings multiple coming together over time.

Result: Fair Value of $9.75 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, investors still need to watch for project deferrals and spot market volatility, which could pressure utilization, margins and the cash available for future buybacks.

Find out about the key risks to this Helix Energy Solutions Group narrative.

Another Angle on Valuation

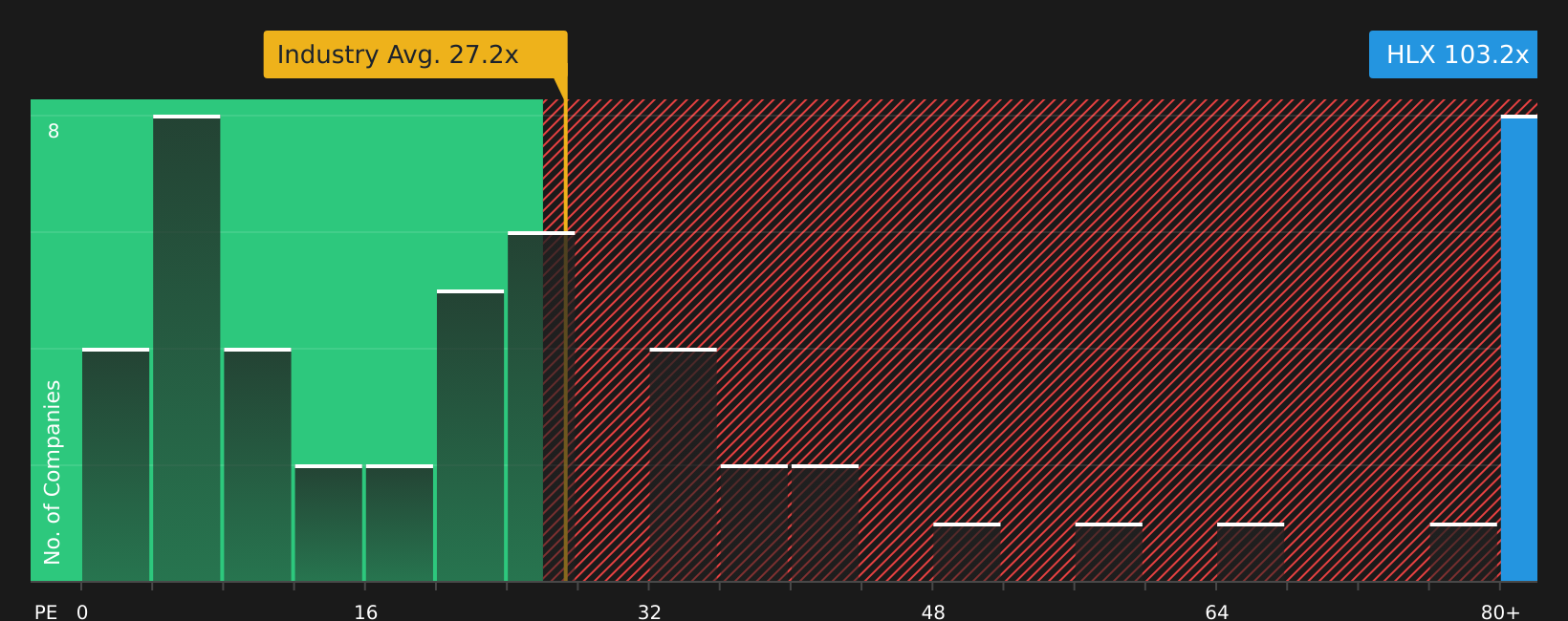

Here is the wrinkle. While the narrative and analyst targets frame Helix as modestly undervalued, the current P/E of 99.3x is far above the fair ratio of 19.9x, the US Energy Services industry average of 34.9x, and the peer average of 72.4x. That kind of gap can signal valuation risk if earnings do not catch up, so how comfortable are you with that stretch?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Unsure how to balance the cautious tone around valuation with the more optimistic long term story and recent momentum figures? Take a closer look at the underlying numbers, compare them with your own expectations, and then weigh up the trade off between potential upside and the risks highlighted in our 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Helix has sharpened your thinking, do not stop there. Use the screener to quickly spot other stocks that might fit your return and risk goals.

- Target potential upside by scanning for companies trading below intrinsic estimates with the 49 high quality undervalued stocks.

- Strengthen your portfolio core by focusing on companies with healthy finances through the solid balance sheet and fundamentals stocks screener (44 results).

- Get ahead of the crowd by searching for lesser known opportunities using the screener containing 21 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English