How Warrior Met Coal’s Profit Rebound and Blue Creek Completion Will Impact Warrior Met Coal (HCC) Investors

- Warrior Met Coal reported first-quarter 2026 results showing sales of US$448.47 million and revenue of US$458.59 million, with net income improving to US$72.34 million from a net loss a year earlier.

- The company also reaffirmed its full-year 2026 production and sales guidance and confirmed completion of the major Blue Creek mine buildout, underscoring management’s confidence in its operating plan.

- With Warrior Met Coal reaffirming 2026 volume guidance after swinging back to profitability, we’ll examine how this reshapes its investment narrative.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Warrior Met Coal Investment Narrative Recap

To own Warrior Met Coal, you need to believe that demand for its metallurgical coal, particularly from export markets, will support the company’s expanded production base while it manages pricing and regulatory pressures. The key short term catalyst is how effectively the newly completed Blue Creek mine and existing operations can convert reaffirmed 2026 volumes into sustained profitability. The latest earnings beat and return to profit are encouraging, but they do not remove the structural risks around pricing and decarbonization.

The most relevant update to this earnings release is Warrior Met Coal’s decision to reaffirm its 2026 production and sales guidance of 12.0 to 13.0 million short tons of coal production and 12.5 to 13.5 million short tons of coal sales. Holding guidance steady after a strong first quarter and confirmation that Blue Creek’s major buildout is complete ties directly into the main catalyst: proving that higher capacity can be sold at acceptable margins without overexposing the business to weaker coal prices or regional demand shifts.

Yet, even with improving results, investors should be aware that growing exposure to export markets and evolving climate regulation could still...

Read the full narrative on Warrior Met Coal (it's free!)

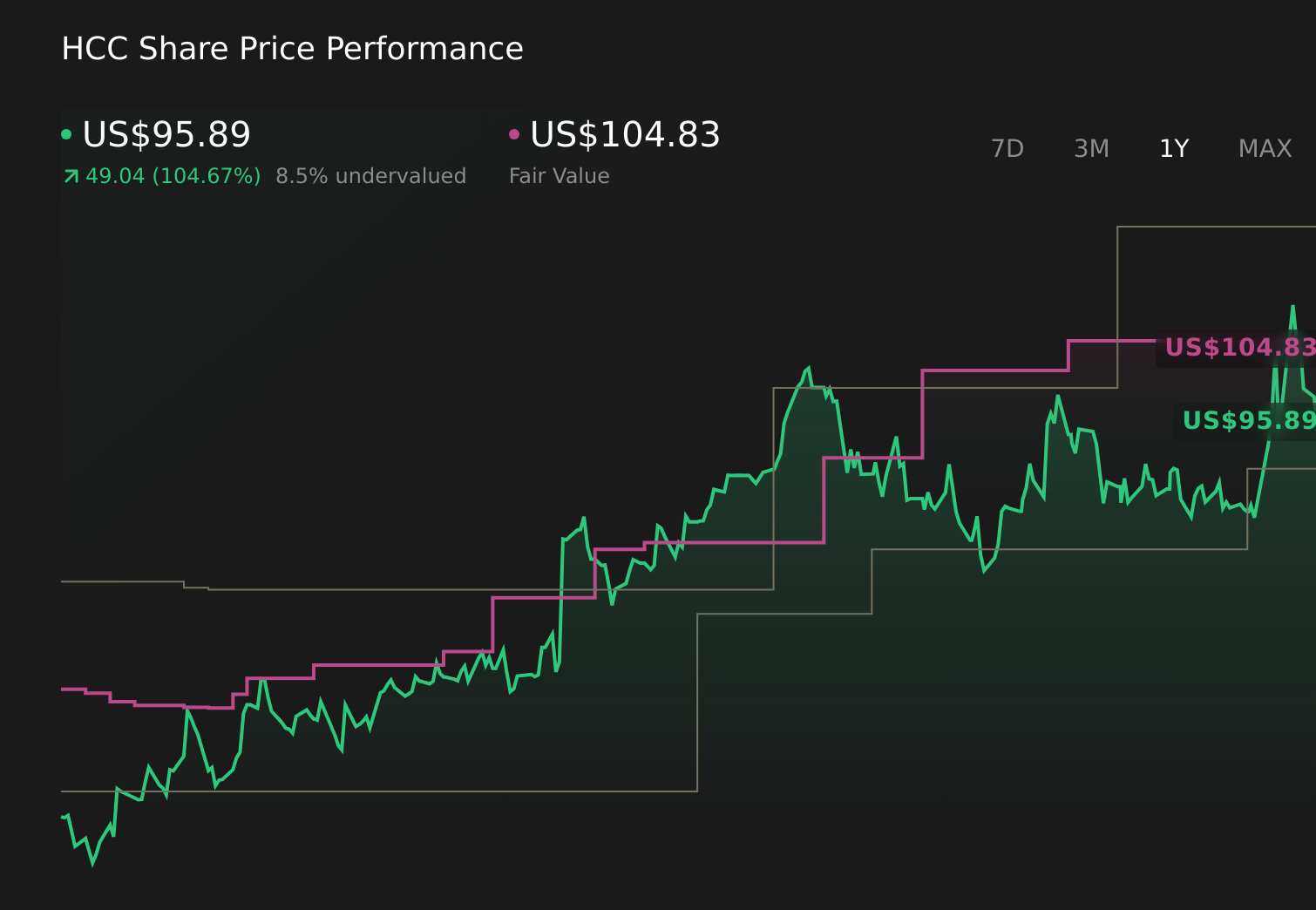

Warrior Met Coal's narrative projects $2.3 billion revenue and $472.1 million earnings by 2029.

Uncover how Warrior Met Coal's forecasts yield a $105.67 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Before this Q1 result, the most optimistic analysts were already modeling around US$2.7 billion in future revenue and roughly US$820.8 million in earnings, which is far more upbeat than consensus. If you lean toward that bullish view, Blue Creek’s completion and reaffirmed 2026 volumes may look like early confirmation, but the same news can also sharpen concerns about long term decarbonization and pricing pressure, so it is worth comparing how different forecasts might shift as new data comes in.

Explore 4 other fair value estimates on Warrior Met Coal - why the stock might be worth as much as 61% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Warrior Met Coal research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Warrior Met Coal research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Warrior Met Coal's overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 26 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English