A Look At Tripadvisor (TRIP) Valuation After Softer First Quarter Earnings Results

Earnings set the tone for Tripadvisor (TRIP)

Tripadvisor (TRIP) just opened its year with a first quarter update that showed softer sales and a wider loss, a combination many investors watch closely when reassessing the stock.

The company reported first quarter revenue of US$382.4 million compared with US$398.2 million a year earlier. Net loss widened to US$32.4 million from US$11 million, with basic and diluted loss per share from continuing operations at US$0.28 versus US$0.08 previously.

See our latest analysis for Tripadvisor.

The first quarter figures arrived after a tough stretch for Tripadvisor shareholders, with the share price down 16% over the past month and the year to date share price return down 34.9%, while the 1 year total shareholder return has fallen 36.21%. This points to fading momentum as investors reassess the risk profile following weaker earnings.

If this earnings reaction has you reviewing your watchlist, it can be useful to broaden the search and check out 18 top founder-led companies

With Tripadvisor now trading at US$9.53 and showing a 66.14% intrinsic discount alongside a 40.40% gap to the average analyst price target, the key question is whether this signals undervaluation or if the market is already pricing in future growth.

Most Popular Narrative: 33.7% Undervalued

Tripadvisor's most followed narrative pegs fair value at US$14.38, well above the latest close at US$9.53, which sets up a clear valuation gap for investors to interrogate.

Tripadvisor's focus on scaling its experiences marketplace (Viator and TheFork) takes advantage of global consumer shifts toward experiential travel, as rising international leisure travel from the expanding middle class and a preference for unique experiences are both enlarging the company's addressable market and supporting sustainable, above-industry growth rates, positively impacting long-term revenue and gross profit.

The thesis rests on Experiences doing the heavy lifting, earnings expanding faster than revenue, and a future profit multiple that sits below many peers. It is worth examining which assumptions need to hold for that to work.

To reach a fair value of US$14.38, the narrative leans on a detailed earnings path, margin improvement and reinvestment returns, all discounted back at a 10.84% rate to reflect required returns on capital.

Those inputs are layered on top of analyst expectations for revenue growth, profit margin expansion and future earnings per share, with the narrative effectively arguing that the market is not fully reflecting the potential cash generation implied by that scenario.

Result: Fair Value of US$14.38 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on Tripadvisor offsetting pressure on organic traffic and core revenue, as well as managing competition in hotels and experiences that could compress margins.

Find out about the key risks to this Tripadvisor narrative.

Another Angle on Tripadvisor's Valuation

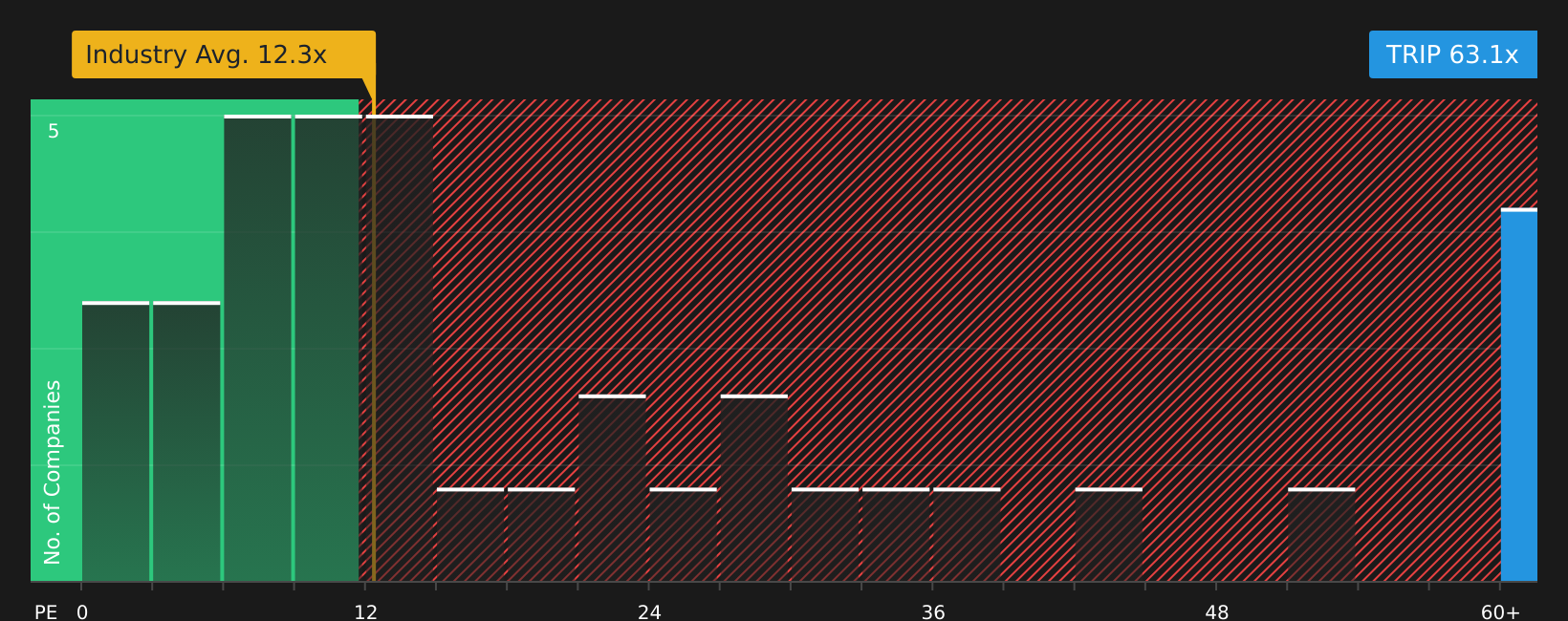

The narrative and fair value estimate of US$14.38 lean on future earnings and cash flows, but the current P/E of 59.6x tells a very different story. It sits far above the US Interactive Media and Services average at 12.6x and the 16.5x peer average, as well as the 26.7x fair ratio the market could move toward, raising the question of whether the real risk here is overpaying for that growth.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

These mixed signals on Tripadvisor can look confusing, so it is worth checking the underlying data now and weighing both sides of the story by reviewing the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Tripadvisor is on your radar, do not stop there. Widen your opportunity set now so you are not relying on a single stock story.

- Spot potential value opportunities early by scanning 51 high quality undervalued stocks that combine quality fundamentals with attractive pricing signals.

- Prioritise resilience and sleep better at night by checking 65 resilient stocks with low risk scores that score well on financial strength and risk metrics.

- Get ahead of the crowd by searching the screener containing 21 high quality undiscovered gems that few investors are watching but already show solid business quality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English