Assessing Standex International (SXI) Valuation After Third Quarter Earnings Miss And Estimate Cuts

Third quarter miss puts Standex International (SXI) under closer scrutiny

Standex International (SXI) is back on investors' radar after reports that fiscal third quarter earnings and revenue missed expectations, with analysts cutting estimates amid mixed demand and wider macroeconomic headwinds.

See our latest analysis for Standex International.

The recent fiscal third quarter miss and softer earnings sentiment have taken some heat out of the stock in the short term, with a 30 day share price return of down 9.78%. This comes even though the 1 year total shareholder return of 61.63% and 5 year total shareholder return of 165.84% point to a much stronger longer term story, while investors also weigh the impact of leadership changes and a largely completed buyback.

If you are reassessing your industrial holdings after this quarter, it can help to broaden the search and check out 18 top founder-led companies

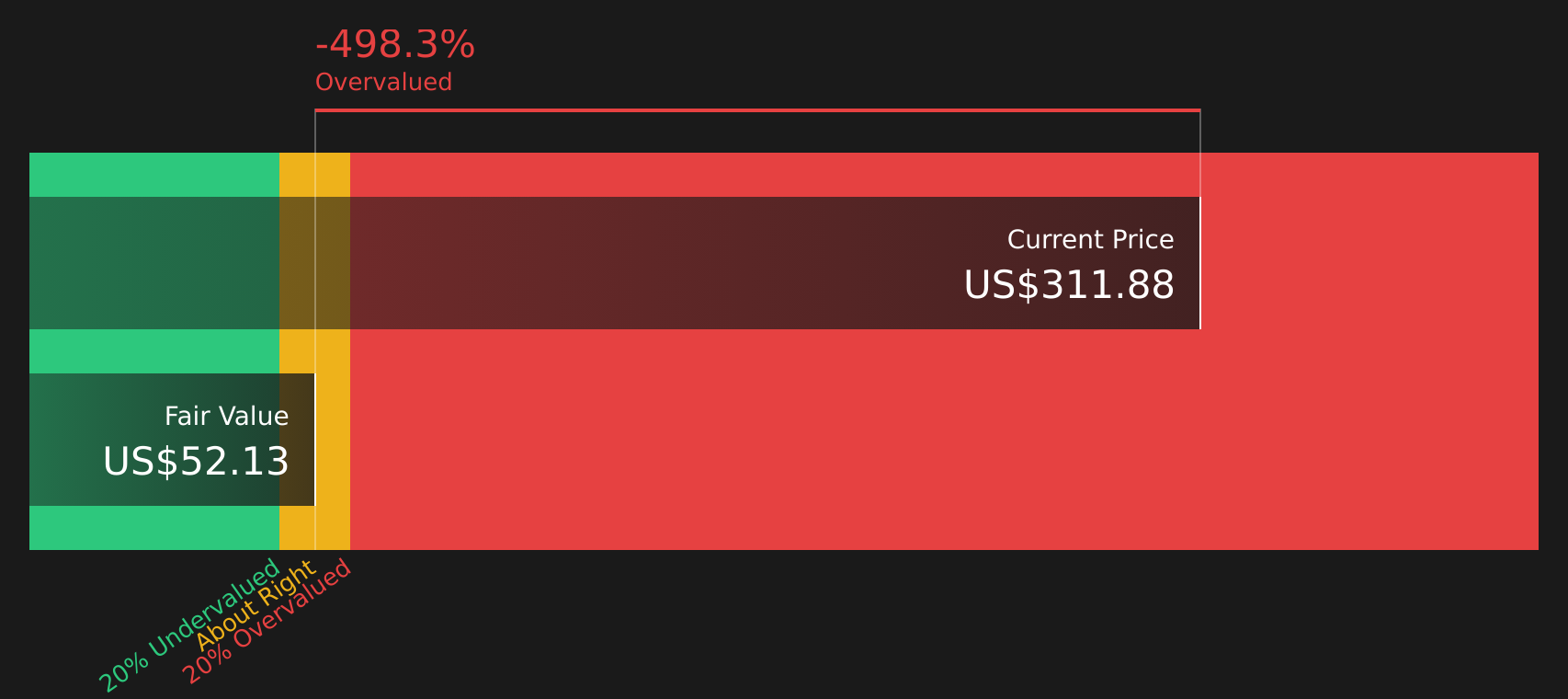

So with Standex posting a softer quarter, yet trading at a roughly 30% intrinsic discount estimate and about 16% below the current analyst price target, is there real value here, or is the market already pricing in future growth?

Most Popular Narrative: 13.6% Undervalued

At a last close of $251.18 versus a narrative fair value of $290.80, the most followed view sees Standex as undervalued, hinging on specific growth and margin assumptions that investors are now questioning after the softer quarter.

The accelerating global shift towards automation, electrification, and grid modernization is driving persistent demand for Standex's high-value electrical, sensor, and precision engineering solutions, creating a runway for double-digit sales increases in fast growth end markets and supporting sustained above-GDP revenue growth.

Ongoing digital transformation in industrial sectors and the proliferation of IoT applications are expanding the need for custom sensors and embedded technologies; Standex's ramped-up R&D and layered new product launches are expected to compound organic growth and provide higher-margin revenue streams, underpinning multi-year operating and net margin expansion.

Want to see what sits behind that optimism? The narrative leans on a tight mix of revenue growth, richer margins, and a punchy future earnings multiple. Curious which assumptions really move the $290.80 fair value and how sensitive they are if things do not go to plan? The full breakdown shows exactly how cash flows and valuation fit together.

Result: Fair Value of $290.80 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can change quickly if acquisition-driven growth masks weaker organic demand, or if trade and tariff pressures start to squeeze margins harder.

Find out about the key risks to this Standex International narrative.

Another Angle: Earnings Multiple Sends A Different Signal

The SWS DCF model points to a fair value of $357.37 for Standex, which suggests the stock is undervalued even after the recent pullback. That sits uneasily alongside a current P/E of 30.7x, which is higher than both the Machinery industry at 25.9x and the 25.5x fair ratio the market could move toward. If earnings or sentiment cool, could that valuation gap turn from opportunity into pressure?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Mixed messages on value and risk so far? Take a closer look at the numbers, pressure test the assumptions, and weigh up the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that could fit your goals even better, so keep your watchlist working hard for you.

- Spot potential bargains early by checking out 52 high quality undervalued stocks that combine quality with a price that may appeal to value focused investors.

- Build a steadier core to your portfolio by scanning 65 resilient stocks with low risk scores that score well on resilience and business risk.

- Get ahead of the crowd by tracking screener containing 21 high quality undiscovered gems that pair solid fundamentals with relatively low market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English